Trade war and geopolitical tension has made a challenging year for the commodities in 2019. However, commodities like lithium and cobalt have been down for some other reasons. Before the beginning of the Electric Vehicle era, lithium was primarily used in medicines for curing depression.

Due to increase in supply, which has overtaken the demand from EVs, the lithium carbonate prices have fallen by more than 20 per cent this year to around $10,000/mt, as measured by S&P Global Platts. When lithium prices reached over $25,000/mt in 2017 it was called âwhite goldâ, but now it is been branded as âwhite dustâ, as some companies burned after overinvesting in its large scale-production and processing.

The demand supply ratio is not good for lithium as supply of the commodity is more and demand from EVs is less as it was anticipated, and this has happened to almost all battery materials. The pickup rate from EV is not expected to start increasing until the early to mid-2020.

One of the top investment banks has forecasted that the prices of lithium may further fall by 30% by the end of 2025 as suppliers are very eager to bring on new refining and production capacity. One of the Australian companies, Galaxy Resources has also taken a hit from the slump. Galaxy Resources is scaling back its production from the mines by 40% in the next year.

The biggest lithium players in the world are suffering from the decrease in prices. Worldâs top companies like Tianqi, that owns half the Australiaâs best lithium, reported a loss in September quarter 2019.

Spodumene or brine are the main source of lithium and Australia is the home of majority of spodumene mines. The prices of spodumene are down by 38% to $543 per tonne in the same period.

Let us look at Australiaâs Top Lithium Producing Companies:

Galaxy Resources Limited (ASX: GXY)

Galaxy Resources Limited is engaged in the production of lithium concentrate and exploration for minerals in Australia, Canada and Argentina.

Quarterly Highlights for September Quarter 2019:

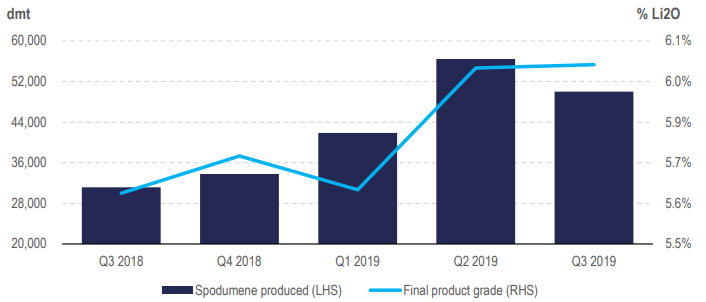

- Mt Cattlin achieved production volume of 50,014 dry metric tonnes (dmt) of lithium concentrate, which is the midpoint of production guidance of 45,000 â 55,000 dmt;

- The unit cash cost of production came at US$387 / dmt from Mt Cattlin, which made it as one of the lowest cost lithium concentrate operations globally;

- There was a small quarter-on-quarter (q-o-q) increase in unit operating cost, mainly as a result of lower production volume and a lower grade of ore processed on Q3 2019;

- The total shipment came at 58,278 dmt of lithium concentrate, which was slightly under guidance of 60,000 to 70,000 dmt;

- The company has a cash of US$169 million and has a debt of US$32 million as on 30th September 2019.

Production Volume and Grade of Final Product (Source: Company Reports)

Guidance for the Next Quarter:

- In the next quarter, the company is targeting a production of 35,000 to 45,000 dmt of lithium concentrate;

- This will imply full year production guidance of 183,000 â 193,000 dmt, within the previous guidance range of 180,000 â 210,000 dmt;

- The company is targeting shipment volume of 30,000 to 40,000 dmt for Q4.

Outlook:

In response to the market conditions currently being experienced in the lithium sector, the company is reviewing the operations from the Mt Cattlin to determine the optimal scale of operations. To ensure that Mt Cattlin continues to maintain healthy balance sheet and produce a positive operating cash margin, the company is going to prioritise value over volume. The review is near its completion, and the company is planning to cutback 40% of its production from Mt Cattlin;

- Cost reduction initiatives will continue to be a major focus area at Mt Cattlin;

- Galaxy has undertaken a review of all key contracts and identified several potential sources of cost reduction, some of which have already been realised;

- This reduced scale of operation, combined with the cost initiatives currently underway, will allow Galaxy to maintain a low unit operating cost and a forecasted positive operating cash margin.

Comments of the company on Lithium Market:

The performance in the lithium-ion battery supply chain sector and electric vehicle was soft during Q3 2019. Combination of factors like US/China trade war and weaker than expected growth in China has negatively impacted the short-term sentiment and overall economic outlook.

- A soft quarter in Chinese New Energy Vehicle (âNEVâ) manufacturing production, as well as subdued deliveries in the USA were core contributors to the weakness in lithium demand during Q3 2019;

- The key supply side pressures remain significant stockpiles of lithium products and an oversupply of lithium materials;

- Pressure associated with low-prices and increased competition is forcing a supply side rationalisation;

- In the spodumene market, the magnitude of supply volumes, and a low utilisation of conversion capacity has driven market prices to fall below the operating cost of marginal producers.

Stock Performance

The stock of GXY closed the dayâs trading at $0.955 per share on 1st November 2019, up by 2.139% from its previous closing price, with the market capitalisation of $382.86 million. The total outstanding shares of the company stood at 409.48 million, and its 52-week low and high is $0.815 and $2.850, respectively. The company has given a total negative return of 26.95% and 36.61% in the time period of three months and six months, respectively.

Pilbara Minerals Limited (ASX: PLS)

Pilbara Minerals Limited is engaged in the business of exploration, development and operation of the Pilgangoora Lithium-Tantalum Project.

The companyâs objectives are:

- to sell premium products from the conduct of safe mining and processing activities at the 100% owned Pilgangoora Project located in the Pilbara region of Western Australia;

- to increase the existing Joint Ore Reserves Committee (JORC) resource and reserve at the Pilgangoora Project, and to undertake further exploration at its other North Pilbara exploration projects;

- to create opportunities through the establishment of deeper links with the lithium raw materials supply chain, including participation in downstream chemical processing opportunities to leverage the size and quality of the Pilgangoora Project.

Quarterly Highlights for September Quarter 2019:

The company has secured a strategic investment from CATL, Chinaâs largest EV battery manufacturer, as a part of equity raising of $111.5 million to support its long-term growth.

Key Highlights:

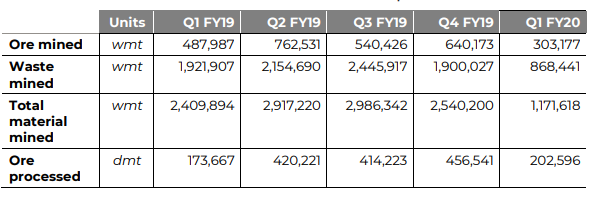

- Production was weakened at the Pilgangoora Project due to customer requirements and current market conditions;

- The company produced 21,322 dmt of spodumene concentrate 6.06% Li2O;

- The company shipped 20,044 dmt of spodumene concentrate, including parcels of both SC6 (6% Li2O) and SC5.5 (5.5% Li2O);

- First shipment to Chinaâs Great Wall Motor Company completed in August, pursuant to the new offtake agreement for 20,000 dmt per annum over a period of approximately six years.

Total Ore Mined and Processed (Source: Company Reports)

Comments of the Company on The Lithium Market:

This quarter was weak in respect of demand of lithium raw material, which impacted prices received across the entire lithium raw materials and chemicals product suite and spodumene exports from Western Australia. The company has already moderated its production, reduced costs and used available ore and final product stocks to support customer sales. Due to weak demand from China, entire lithium industry is being impacted. This is because of changes to the subsidy regime to support Chinese electric vehicle (EV) production.

- The EV production is still growing in China, the relative pace of growth has tempered over approximately the last 12 months;

- This has resulted in lower demand for lithium chemicals thereby impacting price;

- The slower uptake of the Chinese subsidy regime has resulted in persistent weak market conditions for lithium chemicals;

- The company has also changed its guidance for December quarter 2019, which has been revised to 35,000 dmt from 70,000 dmt for spodumene concentrate.

The company is continuing to assess the customer base in this product segment to determine the future production requirements of secondary concentrate as opposed to primary concentrate.

Stock Performance

The stock of PLS closed the dayâs trading at $0.335 per share on 1st November 2019, up by 3.077% from its previous closing price, with the market capitalisation of $722.7 Mn. The total outstanding shares of the company stood at 2.22 billion, and its 52-week low and high is $0.270 and $0.885, respectively. The company has given a total return of -30.85% and -46.28% in the time period of three months and six months, respectively.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.