Health minister Greg Hunt has recently declared an increase of 2.92 per cent in industry weighted average of private health insurance premium in 2020, rejecting health fundsâ call for a rise of 3.5 per cent. It is the smallest such increase in last two decades, which represents a significant decline from the governmentâs previous increases over the last seven years ranging from 3.25 per cent to 6.2 per cent.

Over the years, insurance sector growth and development has been directly related with the health and population of the nation. Due to the increase in awareness, citizens of most of the developing countries are inclining towards insurance policies.

Letâs have a look at two insurance companies along with their business updates.

NIB holdings limited (ASX : NHF)

NIB holdings limited is engaged in provision of health insurance whereby the company underwrites and distributes private health insurance across the geographies like Australian and New Zealand. The business caters to the residents as well as international students and visitors to Australia.

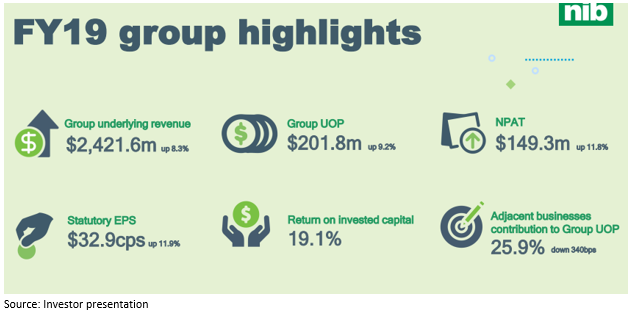

The company recently updated that it will increase the health insurance premium from April 2020 by an average of 2.9%, in line with the recent changes to private health insurance premiums. As reported, the company provided lower premium as compared to the previous corresponding year for the sixth consecutive year. The company made a record claim of $1.7 billion on behalf of Australians during FY19.

Business Highlights

- The business reported actual arhi claims inflation of 2.9% per person, aided by product mix erosion or downgrading.

- Net margin of the company was reported at 6.3% during FY19 along with actuarial development as compared to 6.5% in FY18.

- During FY19, NHF reported total revenue at $2.4 billion, up 8.3% on y-o-y basis. The companyâs NPAT came in at $149.3 million, up by 11.8% from the previous financial year.

- The Australian businessâs membership grew 2.1% on y-o-y basis as compared to the industryâs growth of 0.7% during the same time frame. Premium revenue from Australia segment came in at $2,013.2 million, witnessing a year-on year growth of 7.6%.

- The business reported 7.2% membership growth across the New Zealand segment, while the revenue came at $215.5 million, up 8.8% on y-o-y basis.

- The international business derived premium revenue of $110.1 million, up 18% on y-o-y basis. NHF reported membership growth of 19.5% during the financial year of 2019.

- The travel segment reported gross written premium at $152.7 million, up 7.5% on y-o-y basis. During the period, the company reported QBE Travel acquisition.

- The company established new operations across Tiajin and Shanghai (located in China). NHF reported a team of ~25 people working as part of joint venture in China. While, the China segment is waiting for the regulatory approval for health insurance product. The company secured health service annual revenue ~$1 million from the JV in China.

Outlook: As per the latest guidance, the company is expecting claims inflation per person expense likely to increase in FY20. The company estimated that effect of health waiver plays a pivotal role for the inflation while the it expects the impact should be moderate in FY20.

The company reaffirmed its FY20 underlying operating profit guidance of at least $200 million (statutory operating profit of at least $180 million).

Stock Update: The stock of NHF traded at $6.560, down 2.82% with a market capitalization of $3.08 billion on 10 December 2019 (2:38 PM AEST). The 52-week trading range of the stock stands at $4.640 to $8.2. The stock has generated an annualized dividend yield of 3.41% while the price to earnings ratio of the stock stood at 20.52x on trailing twelve months (TTM) basis.

Medibank Private Limited (ASX: MPL)

Medibank Private Limited is a private health insurance player, which focuses on distributing and underwriting private health insurance policies under its two brands, ahm and Medibank. It has recently received the approval to increase health insurance premiums by an average of 3.7%- lowest premium rise in almost two decades.

FY19 Financial Highlights for the period ended 30 June 2019:

- The company reported revenue of $6,655.8 million as compared to $ 6,468.8 million in previous financial year.

- Net profit of the company came in at $437.7 million as compared to $424.2 million in FY18.

- The business reported total current assets at $3,130.5 million including Cash and cash equivalents at $656.5 million, Trade and other receivables of $283.9 million and Financial assets at fair value at $2,130.7 million as on 30 June 2019.

- The company recorded 3.77 million of customers, paying $5.4 billion benefits to its customers.

- The management fees was noted at $2.9 million or 0.5% in FY19 and lower management expenses to premium revenue at 8.7% in FY19 (8.8% in FY18).

- Savings of $20.4 million were recorded through productivity program during the year aided by by savings in procurement, consulting spends, technology and automation.

- Net claims paid on behalf of customers, during the period increased by $135.4 million, or 2.6%, to $5.4 billion, representing 82.9% of Health Insurance premium revenue and a claims cost per policy unit increase of 2.3%.

Guidance: As per the FY20 guidance, the company will focus on personalize and integrate health along with customerâs experience. The company will focus on enhancing corporate, non-resident and diversified portfolios in coming years, while further eyeing to expand its strategy to commercialize the payor service including payment integrating program.

Stock Update: The stock of MPL traded at $3.230, down 0.62% with a market capitalization of $8.95 billion on 10 December 2019 (2:38 PM AEST). The stock is quoting at the upper band of its 52-week trading range of $2.274 to $3.654. The stock has delivered negative returns of 7.14% and 3.45% in the last three-months and six-months, respectively. The stock is trading at a P/E multiple of 19.46x on TTM basis. The stock has generated an annualized dividend yield of 4.03%.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice