In this article, we would discuss two stocks from the Industrials Sector. These companies are component of the S&P/ASX 200 Index and the S&P/ASX 200 Industrials (Sector) Index. On 13 August 2019, the Australian Benchmark Index S&P/ASX 200 last traded at 6,568.5, down by 21.8 points or 0.3% compared to its last close. Concurrently, the S&P/ASX 200 Industrials (Sector) Index, by the closure of the trading session was at 6,864.2, up by 4.2 points or 0.06% from the previous close.

Aurizon Holdings Limited (ASX: AZJ)

On 12 August 2019, the company released full year results for the period ended 30 June 2019. Accordingly, the revenues were down by 7% to $2,908 million in FY2019 compared with $3,113 million in FY2018. The statutory Earnings Before Interest and Tax was down to $829 million compared with $966 million in the prior corresponding period.

Meanwhile, the statutory NPAT was down by 15% to $473 million in FY2019 against $560 million in FY2018. Subsequently, the statutory EPS stood at 23.8 cents in FY2019, down by 14% from 27.8 cents in FY2018.

The companyâs non-network businesses contributed $450 million to the group EBIT excluding redundancy costs. It also included $20 million in recoveries of doubtful debt, and the figures from the segment were above the market guidance of $390 - $430 million in August 2018. Reportedly, the network segment accounted for $400 million to the group EBIT, and 12% reduction was due to one-off regulatory true-up of $60 million.

Further, it was reported that the subdued revenues of the company depicted the impact of UT5 final decision, FY18 true-up in Network business, lower revenue in Bulk due to the cessation of the Cliffs contract.

Besides, the company declared a final dividend of 12.4 cents per share, which would be 70% franked. Besides, the record date for the dividend is 26 August 2019, Ex-date is 27 August 2019, and it is scheduled to be paid on 23 September 2019. Admittedly, the latest dividend takes the total dividend for the full-year to 23.8 cents.

Strategic Review

Strategic Review (Source: Full Year Results Presentation)

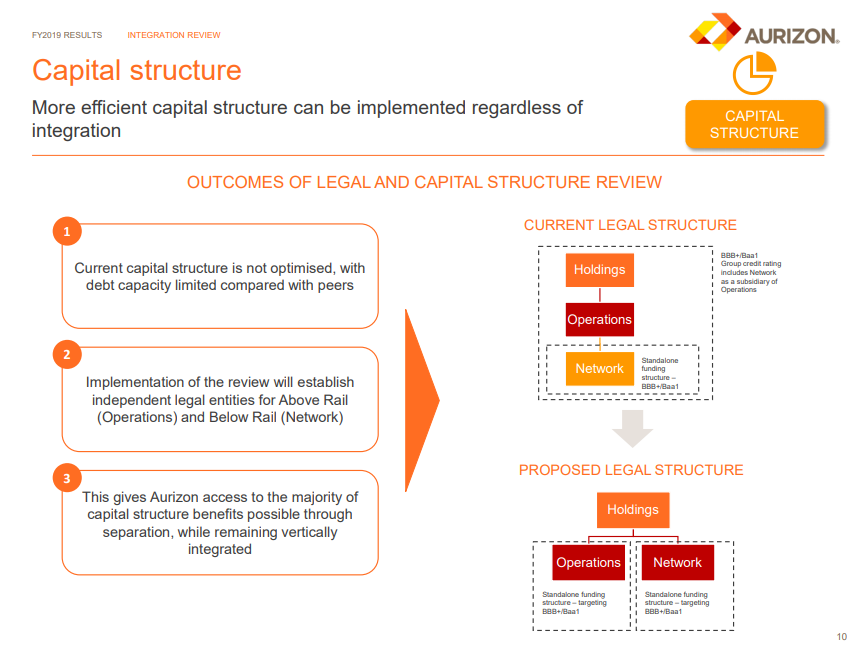

The company also completed two strategic reviews during the year. Reportedly, the company reviewed its vertically integrated structure to determine the optimal structure behind the created shareholder value. In 2010, the company had completed such review during the IPO, and the recent review depicted that the benefits from integration outweigh the benefits of the separation.

Meanwhile, the second review was to test the optimality of the capital structure of the company. Subsequently, the proposed legal structure intends to maintain the rail business under the holding company. The new structure would allow standalone funding structure for the Rail Business â Operation & Rail Business â Network, which would mean independent gearing levels according to the risk profiles.

Further, it provides an additional funding capacity of ~$1.2 billion, the Operations & Network would target credit rating of BBB+/Baa1, and implementation of the proposed structure is likely to be completed in the upcoming months.

Balance Sheet

Reportedly, the current assets were down by $66.6 million due to a reduction in cash, reduction in trade & other receivables due to Cliffs termination payment, and ~$20 million recovery in doubtful debts helped to offset losses.

Besides, the total borrowings of the company was down by $132.1 million due to the repayment of bank debt facilities for $253.4 million, which was offset by the unfavourable revaluation of medium-term notes.

Outlook

As per the release, the company expects Underlying EBIT for the year FY2020 to be in between $880 - $930 million. Further, the company assumes increase in EBIT across all business units backed by volume growth, benefits arising from operational efficiencies. Additionally, the UT5 customer agreement in the Network business would also impact the expected Underlying EBIT for FY2020.

Share Buy Back

As per the release, the company has announced on market share buy-back program for AU$300 million during FY2020. Besides, it would allow the company to undertake efficient capital management, and UBS AG Australia would be acting on behalf of the company to undertake the buy-back program.

Further, the company would undertake the buy-back program for 12 months starting 27 August 2019 to 26 August 2020, and it would conduct buy-back at times, which are considered beneficial for its efficient capital management.

On 13 August 2019, by the end of the trading session, AZJâs stock was at A$6.05, up by 3.242% from the previous close.

NRW Holdings Limited (ASX: NWH)

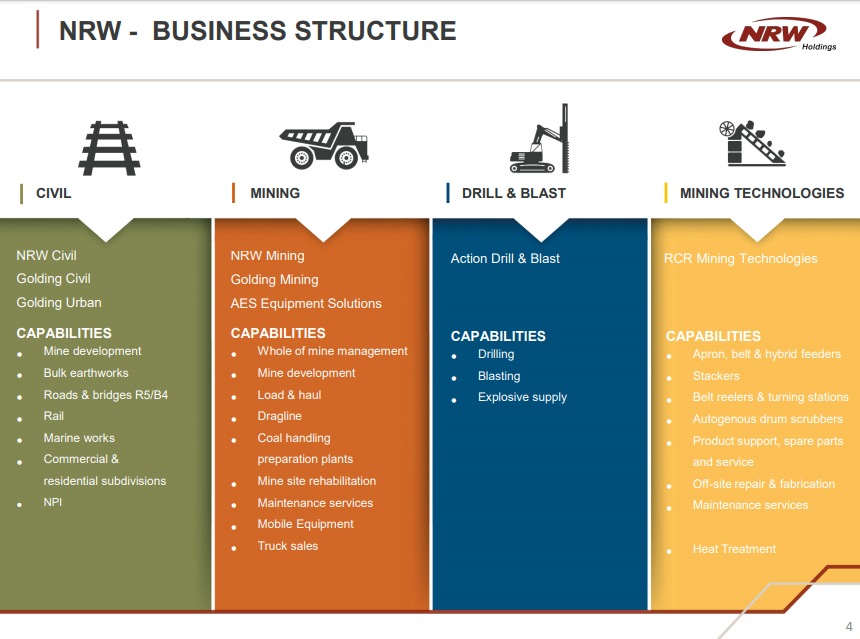

Based in Perth, NRW Holdings is a company engaged in providing diversified services to the Mining, Civil & Construction industry. The company also caters to some of the largest companies in Mining & Construction companies.

Business Structure (Source: NRW - Euroz Investor Presentation, March 2019)

The company had released its full-year results for the previous year on 23 August 2018. Therefore, the investors must be waiting for the company to release the full-year results for the FY2019 period.

On 3 July 2019, the company reported on an agreement with Stanmore Coal (ASX: SMR). Accordingly, the agreement was signed by the companyâs subsidiary â Golding Contractors Pty Ltd, which would mean an addition of third truck & excavator fleet to improve the overburden removal capacity.

Reportedly, approximately $450 million was added to the existing 5-year contract, and at the current mine production levels, the total contract sum is estimated to be approximately of $950 million. Besides, the mine has been increasing the production level during the fiscal year 2019, and it seeks to maintain the current coal production volumes of approximately 3 Million ROM tonnes per annum through the new contract mine plans.

Also, in June 2019, the company reported on the Voluntary Administrators (Administrators) being appointed to Gascoyne Resources Limited (ASX: GCY). Accordingly, Gascoyne Resources, a client of NRW Holdings, procured contract mining service from the company. The company noted that the Voluntary Administrators continued to operate the Gascoyne Resources, while recapitalisation options were being explored.

Reportedly, the company has been supporting the Voluntary Administrators, and payments would be made to all the works undertaken while the Administrators carry a review of recapitalisation options. Meanwhile, the company was expecting an EBITDA for FY2019 in the range of $140 million to $145 million before the appointment of Administrators.

The company also provided an update to the FY20 Outlook. Accordingly, the company had secured work worth $1.1 billion for FY20, which excluded Gascoyne contract. In addition, the company is expecting to deliver full-year revenues of ~$1.5 billion in FY20, and the RCRMT and Urban businesses are anticipated to generate revenues of approximately $200 million.

On 13 August 2019, NWHâs stock last traded at A$2.02, down by 0.976 percent from the previous close. The stock has delivered a return of +28.12% over the year-to-date period. Besides, it was down by 17.34% over the past three months period. The market capitalisation of the company is ~A770.58 million, with ~375.89 million shares outstanding.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.