The S&P/ASX 200 Communication Services Index settled the dayâs trading in green on 4 October 2019, edging up 0.41% to the current value of 1,231.6 while the S&P/ASX 200 Index also moved up 0.37% to 6,517.1. Letâs take a detailed look at the following communications services sector company from Australia that have recently disclosed their financial results for FY19.

Nine Entertainment Co. Holdings Limited

Nine Entertainment Co. Holdings Limited (ASX: NEC) is engaged in TV, broadcasting and program production business and operates across digital, internet, subscription video and other media sectors.

Change in substantial holding for MRN: Macquarie Media Limited holds 87.05% voting power on acquisition of more shares up to 149,027,918 for a consideration of AUD1.46 per Share in Nine Entertainment Co. Holdings Limited on 23 September 2019.

Substantial Holder: Vanguard Group became a substantial shareholder by acquiring 85,323,332 ordinary shares, translating into a voting power of 5.003% in Nine Entertainment Co. Holdings Limited on 20 August 2019.

Dividend: The company announced on 22 August 2019, a dividend of AUD0.05 which is payable on 17 October 2019.

FY19 Financial Performance (as at 30 June 2019): During the year, the group revenue reported 40% to increase in the revenue to AUD1.8 billion while EBITDA, EBIT and NPAT went up by 36%, 25% and 19% respectively. The basic earnings per share reduced by 28% 13.1 cents in FY19 from 18 cents in FY18.

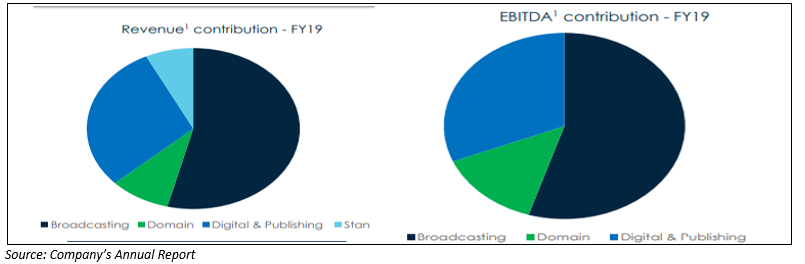

Division wise results-

- Broadcasting: Although broadcasting contributes 54% to the revenue, there was a 5% fall in revenue from prior year. EBITDA came down to AUD 240.6 million in FY19 from AUD270.8 million in FY18 marking a change of 11%.

- Digital and Publishing: There was a 3% rise in revenue from AUD 619.6 million to AUD 637.3 million in FY19 contributing 30% of revenue. EBITDA for digital and publishing comprised 31% of the total and rose by 56% from the prior year to AUD 130.1 million in FY19.

- Domain: Revenue for domain took a dive from AUD 357.3 million to AUD 335.6 million in FY19 representing a negative change of 6%. During the FY19, EBITDA also went down by 15% to AUD 98 million in FY19 from AUD 117.5 million in FY18.

- Stan: Active subscribers of Stan were more than 1.7 million resulting in the growth in revenue and EBITDA by 62% and 56% to AUD 157.1 million and AUD 21.3 million respectively.

Growth Profile: While Broadcasting and metro media focused on efficient delivery of premium content 9now became the leading player in fast growing segment with new revenue streams from existing content spend. Stan subscribers grew up to 1.7 million in 4 years and Domain leveraged Nineâs reach to grow yield and geographic share. During the year, there was a strong cash conversion of 89% forecasting fully franked dividend of 10 cents.

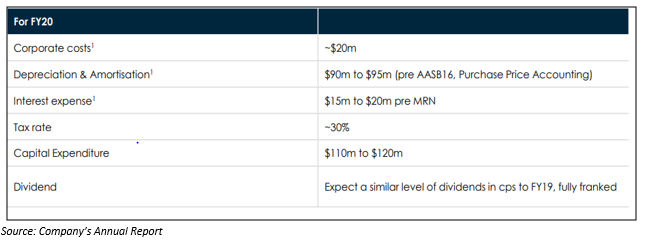

Outlook Group EBITDA growth of around 10% is expected to be reported by the company in the coming year. Strong subscriber growth is set to continue given Stanâs scale and revenue is expected to rise for broadcasting in FY20.

Stock Performance: The stock closed the dayâs trading at AUD 1.977 on 4 October 2019 delivering a YTD return of 41.11% and six motnhs return of 9.48% (as per ASX).

Southern Cross Media Group Limited

Australia-based Southern Cross Media Group Limited (ASX:SXL) creates and broadcasts content on free as well as air commercial radio, TV and online platforms across the nation.

Dividend: Southern Cross Media Group Limited announced the distribution of final ordinary dividend of 4 cents per share payable on 8 October 2019.

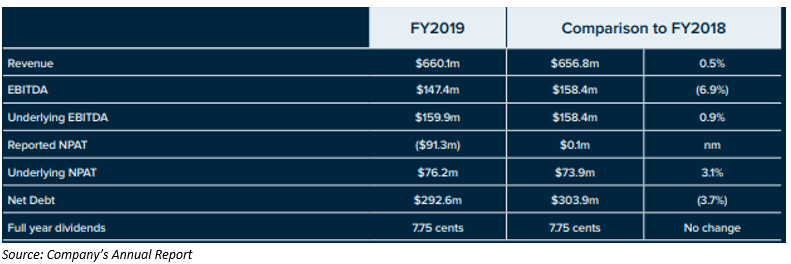

FY19 Financial Performance (as at 30 June 2019): Group revenue of AUD 660.1 million was 0.5% up on the prior year. Group EBITDA of AUD 147.4 million was down 6.9% on the prior year, falling by AUD 12.5 million due to significant items and restructuring costs. Underlying net profit after tax was AUD 76.2 million, which was 3.1% higher than the prior year. Net debt reduced during the year from AUD 303.9 million to AUD 292.6 million. SCA is comfortably within its debt covenants and has a robust balance sheet allowing flexibility and opportunities for future growth. SCAâs television operations contributed revenue of AUD 206.6 million in FY2019, down 3.2% compared to FY2018. Excluding significant items and restructuring charges, underlying EBITDA increased by 1.2% to AUD 33.7 million and the underlying EBITDA margin increased from 15.6% to 16.3%.

Operational Review: Audiences of Hit and Triple M expanded and SCAâs digital stack extends commercial impact. SCAâs Audio business grew successfully in FY2019. Revenue increased by 2.3% to AUD 453.4 million and underlying EBITDA grew by 3.4% to AUD 152.7 million. This result was spurred by national audio revenue growth of 9.3% to AUD 254.4 million, offset by weaker local revenue. The Triple M networkâs metro audience remained stable with an 8.2% share and a 32,000 or 1% increase in listeners to 2.35 million.

The Hit network strengthened in its core demographic of Women 25-54 over FY2019 in metro markets, with a 7.4% increase in listeners to 1.103 million. The company reached over the 10 million Australians every week across television, radio and digital networks. There are about 86 FM and digital radio stations reaching 7.5 million people. There were 3.9 million Triple M network listeners and 4.4 regional network viewers of television.

Outlook: Audio division contributes the majority of the earnings and hence its planned to further grow the division by focusing on improving the content offering, on expanding the breadth of its offering through use of its digital radio spectrum and through the development of personalised and on-demand content. In Television, SCA will achieve improved efficiency following the decision to outsource both playout and transmission services.

Stock Performance: The stock closed the trading session at AUD 1.150 on 4 October 2019 with an annual dividend yield of 6.77%. The performance of the stock has increased by 16.24% YTD.

Ooh! Media Limited

Ooh! Media Limited (ASX:OML) is the media company across Australia and New Zealand creating deep engagement between people and brands through out of home advertising solutions. The offering includes large format classic and digital roadside screens, the ones located in shopping centres, airport terminals and lounges, cafes, pubs, universities, office building and gyms.

Interim Dividend-Cleansing statement: Ooh Media issued 1,613,371 fully paid ordinary shares under the Ooh! media Dividend Reinvestment Plan and 1,143,700 Shares issued pursuant to the Firm Commitment Agreement for a consideration of AUD 3.042 per Share on 30 September 2019.

Change in substantial Holding: HMI Capital LLC and Its associates, HMI Capital Partners, LP., Merckx Capital Partners, LP and HMI Capital Offshore Partners, LP increased its voting power to 15.12% from 13.98% in the company.

Leadership Changes: The company announced to have appointed Ms Philippa Kelly to the position of independent Non-Executive Director, commencing 18 September 2019.

Dividend: Ooh! Media Limited announced the payment of dividend of 3.5 cents which is payable on 30 September 2019.

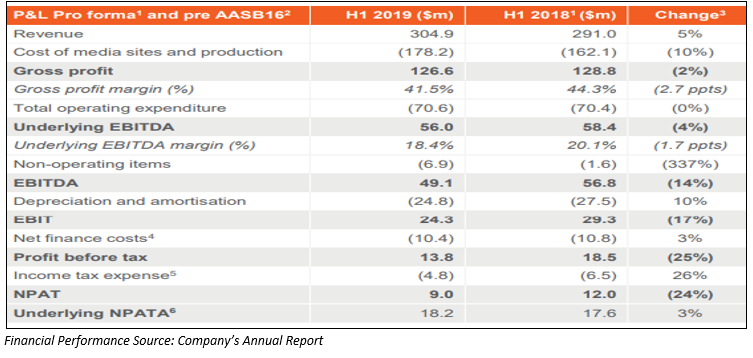

FY19 Financial Performance (as at 30 June 2019): Pro forma revenue rose by 5% up to $304.9 million and Commute business delivered a strong contribution with 13% revenue growth. The companyâs underlying EBITDA reduced 4% to $ 56 million and NPAT fell 24% at $ 9 million due to softer EBIT. Underlying Opex growth tracking was at 4% which is below the previous guidance range of 5-7%. Going forth in FY20, Ooh! Media expects to achieve a leverage ratio below or near to 2.0 times.

The capital expenditure for FY19 amounted to $ 28.3 million.

Operational highlights: The company has successfully integrated Commuteâs highly complementary segments of street furniture and rail into the Companyâs sales propositions. Pre-synergy operational expenditure growth was 4% which is below the prior guidance for growth of between 5% and 7%.

Stock Performance: The OML stock closed the dayâs trading at AUD 2.790, down 1.76% on 4 October 2019 with an annual dividend yield of 3.87%. The market cap of the stock is AUD 688.38 million with the PE Ratio of 27.840.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.