Today, S&P/ASX 200 Information Technology (Sector) is down by around 3.24%, mainly due to the fall of major tech players like EML Payments and Wisetech Global Limited. Despite reporting strong results for the first half of FY20, both of the above-mentioned companies witnessed a significant fall in their share prices during today’s trade. The tightening of guidance range by both of these companies could be the reason behind the negative investors’ sentiment. Let’s take a closer look at the results of these tech companies.

EML Payments Limited (ASX: EML)

Payment solutions provider- EML Payments Limited has reported record results in the first half of FY20. The company witnessed a 60% in GDV (Gross Debit Volume), 25% uplift in revenue and 42% uplift in EBITDA in H1 FY20, as compared to pcp.

During the period, the company’s Gift & Incentive (G&I) segment performed well, with GDV growth of 26% to $0.84 billion. Further, the company witnessed a range of trading conditions with a weaker environment in the UK and Germany offset by strong growth in Poland, Ireland and Dubai in particular. Volumes from the company’s North American malls were broadly stable despite fewer weekend days in the run up to Christmas. The company expect to see continued GDV growth in the second half of FY20 relative to the pcp.

Earlier the company had flagged an increase in gross profit margins due to continued expansion of its self-issuance capabilities in Europe and Australia which delivered a meaningful improvement in the first six months. Notably, the company’s EBITDA growth has exceeded 30% in each of the last three years. The company believes that it is well placed for future continued growth, driven by:

- Continued GDV growth from new and existing programs in each segment;

- The contribution to Group financials from the acquisition of PFS, which is in progress with change of control requests in progress with the Central Bank of Ireland and the Financial Conduct Authority (United Kingdom);

- The contribution to Group financials from the transition of an additional 113,000 salary packaging benefit accounts (by April 2021) through the companby’s agreement with Smartgroup and NSW Health announced in May 2019 and January 2020 respectively;

- Continued improvement in gross margins from self-issuance in Australia; and

- Continued leverage on the company’s growing scale continues to improve the company’s overheads as a % of revenue which reduced to 43% in H1FY20.

It is important to note that the company has tightened FY20 guidance range for Revenue to $120 - $129 million and EBITDA to $39.5 – 42.5 million. Despite reporting strong results, the company today has witnessed a decline of 14.5% in its share price (as at 3:38PM).

Wisetech Global Limited (ASX: WTC)

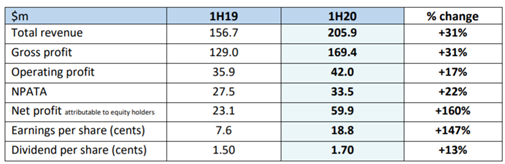

Global cloud-based software solutions provider, Wisetech Global Limited has delivered high quality growth in the first half of 20 with revenues up 31% to $205.9 million and EBITDA up 29% to $62.5 million. The half year results are reflecting the strength of the company’s CargoWise business and strategic actions, along with increased adoption by the world’s largest logistics organisations.

Snippet of Half year Results (Source: Company’s Report)

Over the half year period, the company has continued to expand its technology platform and grow its global footprint.

While providing the outlook for FY20, the company informed that the unexpected outbreak of coronavirus (COVID-19) and the effective shutdown of China, a critical driver of the global manufacturing supply chain and a ~16% contributor to global GDP, is creating negative flow-on effects to manufacturing, which is causing the supply chains and economic trade across the world to slow down.

In considering adjustment to its guidance for FY20, the company has prudently taken into account the potential impact of COVID-19 on manufacturing and export trade and is expecting its FY20 revenue to be around $420 million - $450 million and EBITDA to be around $114 million - $132 million.

The company’s stock has witnessed a decline of 25.7% during today’s trading session (as at 3:38 PM).

Nearmap Ltd (ASX: NEA)

Nearmap Ltd, a global leader in the location intelligence market derived from aerial imagery content, has released its 1H FY20 result today.

For the half year period, the company reported revenue of $46.34 million, up 31% on corresponding prior half year revenue of $35.48 million. Over the period, the company’s total subscription revenue increased by 31%, up to $46.16 million, reflecting continuing strong growth in both Australia & New Zealand, and North America. The company reported EBIT loss of $18.9 million which reflects the scaling of business operations but also includes the impact of accelerated amortisation per the previously announced change to capture cost amortisation period.

During the period, the company invested in the technology to provide the most current, clearest and widest footprint of location intelligence. The company’s camera systems more efficient than any other, its processing capabilities which can seamlessly process the highest resolution imagery in days, not weeks or months, and its tools and content types are what enable Nearmap to be an indispensable asset to its customers.

Last month, the company revised its guidance for its ACV portfolio to end FY20 between $102m- $110m, and to continue to deliver 20-40% ACV growth in the medium to long term.

In the second half of FY20, the company is on track to commercially release its AI content within MapBrowser, making this content generally available to all its customers. The company is of the view that it will delivering year-on-year ACV growth of 20-40% in the medium to long term. The company also expects 20-40% ACV growth in the medium to long term with large deals being the swing factor.

Following the release of the results, NEA’s stock price witnessed a decline of 4.24% during the day’s trade.