Late last month, Royal Dutch Shell CEO, Ben van Beurden, told CNBC “The coronavirus, I’m sure, will keep a lot of people on edge, and rightly so,” and they would be regularly monitoring and reviewing the market situation and activities.

Due to weak LNG demand from Asia, LNG traders are either diverting their shipment routes or looking for new buyers, with the Asian Japan Korea Marker (Platts) 2-month LNG futures trading at record lows at US$2.99 per million British Thermal units on 6 February 2020.

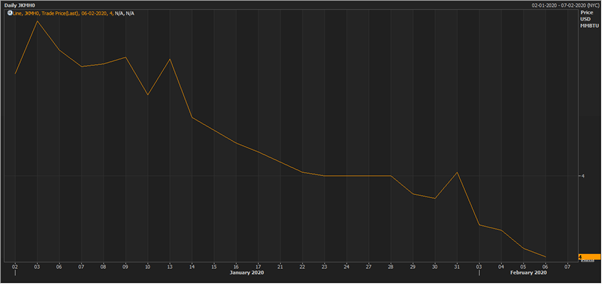

The Japan Korea LNG Marker (Platts) Futures (JKMH0) (Source: EODHD/Others Eikon)

The Japan Korea Market is the Asian indicator of the LNG trade prices for the most part of the continent.

The JKMTM fell by almost 30% since the start of the year from around US$5 per million British Thermal units to US$3.55 per million British Thermal units on 6 February 2020.

The Japan Korea LNG Marker (Platts) 2-Month Futures (JKMc2) Source: (EODHD/Others Eikon)

The JKMTM 2-month futures have fallen from $4.56 per million British Thermal units to $2.99 per million British Thermal units on 6 February 2020, a 34.5% decline in less than 3 fortnights.

If the Chinese LNG buyers force majeure their offtake agreements, the 1-month and 2-month futures of JKMTM LNG marker might fall even lower.

Some of the industry experts anticipate that the Japan Korea Marker (JKM) 1-month future prices might fall under US$3 per million British Thermal units during the upcoming summer season. The situation has arisen when the US, Australia, Qatar and Russian markets have attained stable gas production.

Goldman Sachs has already lowered growth forecast for LNG imports for the first quarter due to the combination of reduced industrial activity and business conditions plagued by coronavirus in China and the reduced demand mainly due to weak demand from both Japan (world’s largest LNG importer) and China owing to the warmer than normal winter season.

In fact, media reports state that CNOOC, the largest buyer from China, had offered to resell LNG amid high stocks and reduced demand.

China Cancels LNG Contracts

China, the second largest importer of LNG in the world, reported the first cases of suspension of supply contracts. The domestic LNG demand in China has weakened following the coronavirus outbreak, which is supposedly affecting the industry demand as well as slowing the domestic and corporate demand due to warmer than expected/normal winter temperatures. The situation is proving to be double whammy for LNG prices in China.

Though there has been no official public announcement by China National Offshore Oil Corporation (CNOOC), as per the street news and some media reports, on 6 February 2020, CNOOC announced force majeure on some of its LNG shipments to multiple suppliers with close to immediate deliveries scheduled earlier.

The CNOOC suppliers include Woodside Petroleum’s North West Shelf LNG-a $34 billion operations operating since 1989, Shell’s Queensland Curtis LNG operations- CNOOC holds a 50% stake in the Train 1 operations and Total SA.

French Supplier on Force Majeure

Total SA came out to the public, rejecting the force majeure notice by a Chinese LNG buyer from China. Total SA emerges as the first global energy firm to publicly speak about the Chinese buyers looking for a way out of the supply deals.

The coronavirus concerns have adversely affected the spot crude oil & LNG sales in the world’s largest energy market, putting additional stress on the global market and depreciating the prices.

During the full-year presentation of Total, Philipe Sauquet, who leads the company’s gas, renewables and power segment, said

The tussle between the LNG suppliers and the Chinese buyers might drag down the LNG market further.

US LNG stocks tumbled, as gas producers earlier counted on China to absorb the record LNG production following the shale boom. As per Reuters, the average daily export increased by 68% y-o-y to 5 billion cubic feet per day in 2019. The exports in 2018 had increased by 53% from 2017. If the slump in LNG demand continues for a longer term, the soaring exports from the US shale boom might come to a halt and may end in production cuts.

The warmer than normal winter had already hit the market hard and recovery of the demand is difficult to expect in summers due to absence of the seasonal demand for heating purposes.

Shares of Cheniere Energy Inc, the largest US LNG exporter, tanked to the year bottom price of US$55.93 a share before recovering to close at US$57.65 a share on 6 February 2020.

As per media reports, Cheniere earlier this week had expressed its intensions of cutting down the LNG production this summer if the customers refuse cargoes.

Woodside Petroleum Ltd (ASX:WPL), the largest Australian natural gas producer, controls almost 6% of the global LNG supply. The major, unlike other companies, has some of the world's largest fixed-price supply contracts already in place for which the supply contract prices might actually be higher than the current spot prices due to the current LNG prices and therefore acting as relief against the low prices.

One of the cheapest LNG contracts was between North West Shelf operator Woodside Petroleum in 2002 for 25 years at a fixed-price contract, which is now expected to be higher than the current spot prices, quite uncommon for such long-term deals.

Recently, Woodside signed another long-term sale agreement with Uniper Global Commodities SE (Uniper) for the supply of LNG for 13 years starting in 2021. The deal is contingent on the final investment decision on the Scarborough development.

But still, Woodside would have to take the hit from gas supplies, which are not part of the fixed price deals. Woodside traded at $33.85 a share with a market capitalisation of $32.38 billion on 7 February 2020.

The industry experts already anticipate increased scheduling of LNG terminal maintenance, this spring, as the oversupply situation in the global market eases down.

Whether or not the upcoming months will revive the LNG market? Will there be more force majeure of the offtake agreement? Only the time can tell.

For the time being, we can expect production cuts and lower imports to China.

Interesting Read: Double Whammy for ASX LNG Stocks

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.