Introduction

Sydney Airport (ASX: SYD) an Australian ASX listed company, consists of Sydney Airport Limited and SAT1 or Sydney Airport Trust 1. The company manages runaways, terminals, retail, car parks, car rental operators, lounges etc. Sydney Airportâs assets are on a very long-term lease till 2097. The company has monopolistic grip on the airways of New South Wales (NSW) and substantially contributes to NSW through about $38bn in economic activity each year.

Over the last five years, the company has reported topline compound increase of 7.3 percent and EBITDA of 7.1 percent per year respectively. Further, the company in the past 5 years period has given the total stakeholder return of 17.7 percent per year (that includes the reinvestment of distributions) against the performance of ASX100 of 7.2 percent per year across the similar period. The stock is driven by rise in the earnings, record passenger numbers, dividend distributions coupled with lower interest rates.

Moreover, the International passengersâ forms about 70% of passenger driven revenues. The company is ranked third globally within Sustain analyticsâ airports sub industry sector. It is rated âAAAâ by MSCI. In addition, the company according to Dow Jones Sustainability Index is ranked seventh globally and as a âSustainability Leaderâ in the transport infrastructure sector.

Sydney Airport (ASX: SYD)

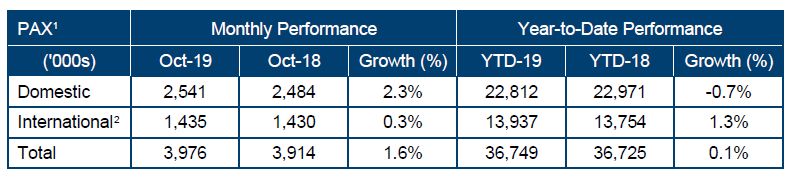

Traffic Performance for October 2019:

Sydney Airport posted 2.3% growth in the domestic traffic with more than 2.5 million people crossing through the domestic terminals in October 2019, though during year to date there has been negative growth of 0.7%. In October 2019, the company posted 0.3% rise in International traffic, though in year to date there has been growth of 1.3%. The travelers from USA, India and Indonesia continues to increase in 2019 period.

Sydney Airport Traffic Performance October 2019 (Source: Companyâs Report)

Restructuring of the Organisation:

During the first half of 2019, the company continued to undertake the restructuring of the organisation & management, to build an effective & simplified organisation. The company during late last year had consolidated its four business units into two, as it grouped the three former non-aeronautical businesses (retail, parking and property) together into a single entity. This entity was kept under Chief Commercial Officer, Vanessa Orth.

Further, in June 2019, SYD reduced the number of direct reports to the CEO from ten to five and had grouped the complementary corporate functions together, under the Chief Operational Officer, Hugh Wehby, for the enhancement of collaboration and service delivery. The company reduced its headcount by 8% and there were 22 talent moves all over the organisation. This organisational restructuring done in the first half of 2019 is expected to deliver benefits in the second half of 2019 & thereafter.

Additionally, the company was focusing on reducing its operating expenses through mindset shift, procurement/contract management and project prioritisation. For the first half of 2019, the companyâs operating expenses fell by $1.6m (1.4%) compared to the prior corresponding period.

Capital Management:

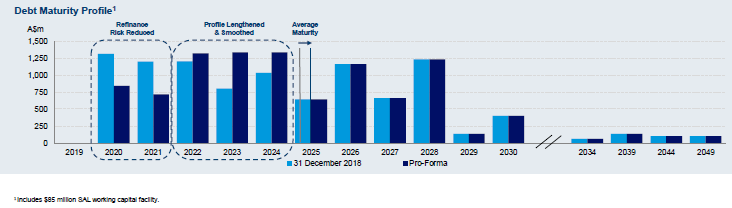

During the first half of 2019, SYD had undertaken the proactive capital management approach and had successfully refinanced $1.4 billion bank debt facilities through a market-leading sustainability linked loan. The loan forms the direct link between the sustainability performance and the funding cost. SYD had refinanced all the debt facilities at lower margins and had extended the weighted average debt maturity from three months to mid-2025.

As a result, the debt maturities over the time period 2021-22 got reduced by 38% and maintained the strong liquidity position with more than $1.1 billion of undrawn facilities available as at 30 June 2019 for funding future debt maturities and investment. This is the first syndicated (multi-bank) sustainability linked loan (SLL) in Australia, which is the largest syndicated SLL across Asia Pacific.

Additionally, for the first half of 2019, the company had reduced the net debt to EBITDA ratio to 6.6x compared to 6.7x in the pcp. The company has also managed the interest rate risk exposures, as the company had hedged 96% of the debt on a spot basis, as on 30 June 2019. Overall during the first half of 2019, the company increased the cashflow cover ratio to 3.2x versus 3.1x for the pcp.

Debt Maturity Profile (Source: Companyâs Report)

Decent Performance for the First Half of 2019:

For the first half of 2019 for the period closed 30 June 2019, SYD delivered 4.1% increase in the Earnings before Interest, Tax, Depreciation and Amortisation (EBITDA) (excluding other expenses) to $649.2 million on the pcp and 4.8% increase in the net operating receipts (NOR) to $431.2 million on the pcp. There has been 3.4% growth in the topline in 1H 2019 on the back of growth in the international passenger and a strong performance from the retail business.

During the first half of 2019, there has been 4.7% increase in the aeronautical revenue, 4% rise in the retail revenue and 1.8% increase in the property and car rental revenue. However, car parking and ground transport revenue fell by 1.4%, which is in line with the growth of domestic passengers.

Outlook for FY 19 & thereafter:

For FY 19, SYD in 2019 reaffirmed its dividend distribution guidance of 39 cents per stapled security, which represents the increase of 4% on the 2018 distribution and 5- year CAGR of 10.7%. The dividend distribution is anticipated to be more than fully covered by Net Operating Receipts across the full year 2019. Further, it is also dependent on the operational performance (underlying) and opportunities related to capital investment. The company has projected to start paying the cash income tax in the calendar year 2022.

However, this distribution guidance depends upon the aviation industry shocks and material forecast changes. Moreover, for FY 19, the company projects the capital expenditure to be in the range of $300-$350m and anticipates the capital expenditure over the period of 2019 to 2021 to be in the range of $0.9 billion to $1.1 billion. The company is also on track to reduce its operating expenses for the full year 2019.

Future outlook (Source: Companyâs Report)

Opportunities:

The passengers are growing which means more new airlines are required. The company is going for more development of international and domestic terminal and is engaging the government for the support in aviation development, that can be done through air service agreements, visas and tourism promotion.

Moreover, the companyâs 93% of retail leases are supported by minimum guarantees. There is a strong demand but has limited supply of all commercial real estate assets. The company is increasing the services for international lounge as the arrivals lounge and hotel, that includes the sleeping pods is expected to open in 1H20 and new AMEX lounge is being planned to open in the second half of 2019.

Recommendation:

On 3 December 2019, SYD last traded at $9.050, declining by 1.416 percent from its last close.

Meanwhile, SYD stock has risen 9.81% in the past three months as on December 2, 2019. The stockâs 52 weeks high was noted at $9.300 and low at $6.370. SYD has market capitalisation of $20.73 billion and 2.16 billion shares outstanding.

The company has realised the cost savings as multiple initiatives have been undertaken, including a simplified organisation, energy procurement and other contract negotiations. Apart from cost savings, the restructuring of the organisation & management has also created capacity to simplify the business and to further invest in the new teams created.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.