Iron ore is an outlier amongst the traditional industrial commodities as it stands tall, thanks to the supply chain weakness over operational challenges faced by the Australian and Brazilian iron ore mining companies.

Iron ore futures on the Dalian Commodity Exchange rose from RMB 542.00 (intraday low on 2 April 2020) to the present high of RMB 621.50 (intraday high on 17 April 2020), which marked a price appreciation of ~ 14.66 per cent.

While operational challenges faced by the Australian miners at the Pilbara region and Port Hedland provided a cushion to the iron ore prices, the market and speculators anticipate the supply chain to slowly restore over time ahead.

To know more about the iron ore supply side, Do Read: ASX-Listed Iron ore Miners and Iron ore Prices to Sustain the Uptick as Supply Chain Restores?

Does that mean iron ore prices would come down?

In a standard scenario, when the supply exceeds demand, prices of commodities usually retrace; however, these are some unusual times, and there is a lot of uncertainty in the market. While the supply chain is restoring, the current restrictions on shipments across the globe could make sure that the supply constraints remain in place, at least for the short-term.

While on the demand counter, the outlook over iron ore demand is opaque as well, albeit, China has resumed majority of its economic activities, the steel sector is among the largest contributor to the Chinese economy, which adjusts its level of production in line with global demand.

China has consistently dominated the steel manufacturing space across the globe; however, steel mills across the nation has a track record to adjust production in line with the global demand. So, to answer the above question, we first need to explore the global steel demand scenario.

Global Steel Demand Scenario

The global steel consumption cooled-off early in 2020; however, the Department of Industry, Innovation and Science anticipates it to grow by 1.1 per cent during the remaining year. The DIIS also predicts that the longer-term trends are more positive, as urbanisation and industrialisation across Asia and Africa kicks-in.

The organisation forecasts that the global steel consumption would grow ~ 16 per cent between 2020 and 2025, with the majority of growth anticipated post the second-half of 2020.

The growing demand would be well met by the growth of ~ 17 per cent in steel production from 2020 to 2025.

- The Halt in Chinese steel Markets Growth

The Chinese domestic steel consumption has remained strong in recent years amid rising property market and state infrastructure spending, which is anticipated by many industry experts to continue over the long-term. However, in recent times the growing concerns around over pollution and air quality coupled with COVID-19 outbreak have led towards a production cut and closure, creating a short-term pressure on the domestic steel inventory.

To Know More, Do Read: Iron Ore Poised for Short-term Recovery as Steel Inventory Declines in China

While on the demand counter, the global steel consumption faces sluggish growth, as a result of the recent softness in industrial production, slowing automotive manufacturing, lower consumer confidence, and while it would be too early to say anything, many industry experts anticipate steel production to likely grow more rapidly in 2020, encouraged by tight inventories, if the impacts from COVID-19 outbreak remain limited.

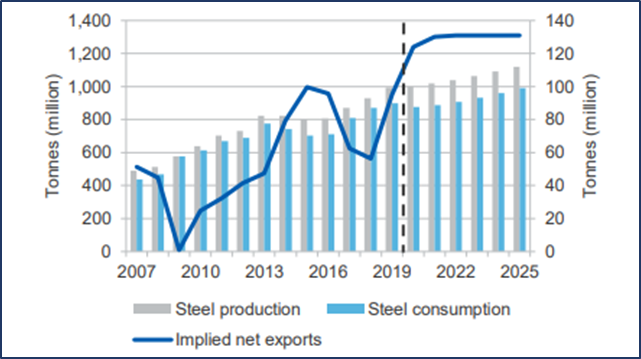

China’s steel consumption, production and exports (Source: DIIS)

While the steel production and iron ore supply both poised to regain momentum over the long-term, the variational changes on a daily basis between steel mills iron ore consumption and iron ore supply is currently deriving the price and would continue to do so over the short-term.

ASX-listed iron ore mining companies such as Rio Tinto Limited (ASX:RIO) has already announced their quarterly report, and though the short-term supply from the Australian miners seems to have taken a hit due to the operational challenges, many matter experts project that the Australian miner would now scale-up the supply.

The projection of market seems to be coming into the play with miners like Rio Tinto, which is among the top-most iron ore exporters to China announcing no major change in iron ore production and shipment due to the bad weather faced by them during the March 2020 quarter at the Pilbara region for the year 2020.

In the status quo, Rio suggested that its quarterly iron ore shipment declined by 16 per cent to stand at 72.9 million tonnes for the March 2020 quarter; however, the shipment for the period remained 5 per cent up against the previous corresponding period, and it should also be noticed that both the iron roe supply from Australia and iron ore consumption in China has shown steady growth until the recent years.

In its recent announcement, Rio suggested that the demand in China is recovering, while the same is more uncertain on the global scale, and also mentioned that the demand for the high-quality iron ores remained strong during the first quarter of 2020, mainly driven by a combination of seaborne supply disruptions and solid demand from China’s steel mills despite Covid-19 impacts.

The iron ore mining giant now estimates a shipment in the range of 324-334 million tonnes, down from its previous guidance of 330-343 million tonnes for the year 2020 on a 100 per cent basis.

While the shipment and future guidance from Rio Tinto has been announced, the market is currently waiting for guidance and update from other major Australian iron ore miners such as BHP Group Limited (ASX:BHP), and Fortescue Metals Group Limited (ASX:FMG) to further gauge the overall supply scenario over the long-term.

The DIIS has already anticipated a steady increase in the Australian iron ore production; however, the recent COVID-19 outbreak has increased the level of uncertainty with many mining experts anticipating that the planned iron ore project across the continent could face headwinds and get delayed ahead due to the travel restrictions imposed by Federal and State Governments.

On the Brazilian counterpart, Vale is facing a dual-edged gizmo from the lockdown imposed by the local authorities and the Brazilian Government, and from the ongoing investigation over the miner in relation to the Brumadinho dam collapse.

So, would the price decline in the wake of restoring supply chain?

The answer to that would be that it is too early to say anything as a lot of assumptions are present in an ideal forecast, and prices are likely to respond to the daily variations of the buy and sell created by the steel mills across China and iron ore traders for the short-term.

While over the long-term, the steel consumption and production are anticipated to rise along with a steady increase in iron ore production; however, this would also assume that the impact from the COVID-19 outbreak remains limited.