February 2020 has arrived with the mainstream reporting season, and companies are gearing up for their result disclosure. The previous reporting season did not bring many joys to the market participants, and a series of downgrades followed up.

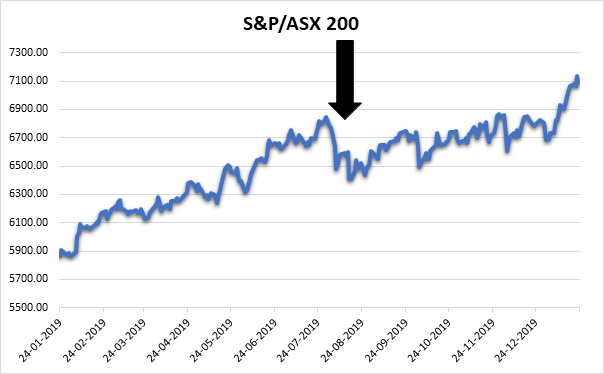

The story was somewhat similar with markets reaching new highs before the start of August 2019 only to suffer one of the steepest falls during the month (as shown in the chart below).

August Crash (Source: ASX)

This time, the markets were touching all-time highs but the recent situation pertaining to the Coronavirus outbreak has intensified some sell-off.

Fears that a slowdown in the Chinese demand is imminent have led the sell-off in the market. The tourism sector, which is amid seasonal activity, is being seen as the most vulnerable area presently.

Moreover, the Australian Universities could also lose many incoming students from China in the February window, as the travel ban persists in commuting between China and Australia.

Given the fact that China is a major trading partner of Australia, the ramifications could be far-reaching. However, the longevity of this pandemic is likely to have distinct outcomes as well.

Additionally, there persists a substantial level of uncertainty in the business environment, and the efforts of Chinese/global healthcare bodies to invent the cure for the healthcare emergency are the ultimate need of the hour.

Firms Likely to Remain Muted on Coronavirus

It is likely that Corporate Australia would wait to come across any material blows to the operating conditions, results or guidance prior to disclosing any kind of downgrades, owing to Coronavirus.

Yet, it should be noted that companies with extensive China relations are exposed to greater risk, and the risk of downgrades from such companies is higher this reporting season.

Meanwhile, it has provided immense opportunities for businesses that export goods, which are in great demand presently, such as air masks, healthcare equipment, and immune system modulators.

It is early to quantify the impact on the economic activity of China, and likewise, it would be uncertain to assess the magnitude of damage to businesses, which could suffer adverse consequences indirectly or businesses that have a small exposure to China.

Therefore, Corporate Australia is likely to remain muted, but shocks could be expected from companies with large dependencies on Chinese consumption as well as companies that have suffered material leakages on forecasts.

Three Interest Rate Cuts in 2019

During 2019, the Reserve Bank of Australia lowered the cash rate three times, and the impact of these rate cuts is likely to be felt on debt-heavy companies with a larger proportion of floating rate debt.

Large industrial companies with a higher proportion of floating rate debt capital are likely to save cash on their renewed and lesser interest payments, thus providing headroom for potential shareholder return.

Interest rate cuts would provide a further boost to the consumer-focused companies. However, the lag effects of the lower interest rates are yet to be seen by the markets.

Meanwhile, the intensified housing sector in the second half of the year could prove to be a tailwind to mortgage lenders and private real estate developers.

Household Consumption & Bushfires

The damage caused by the bushfires, which started in September 2019, could leave a dent in the economic activity as well as household consumption. Some of the businesses had disclosed the magnitude of impact earlier last month.

Using metrics like GDP could be misleading in cases when the economic damage is caused by natural calamities, as it measures the overall production in the economy, rather destruction. For instance, housing reconstruction, due to bushfires, is likely to increase the GDP even though old houses had been burnt.

Whereas, the impact of bushfires on an economy could be the personal expenditure on healthcare services, loss of working hours, depleting consumer confidence, cost incurred in remediation, destruction of assets, etc.

At the same time, natural calamities could have influences on the foreign direct investments, poor impression on tourists, intense damage on natural habitats and environment, and a possible increase in insurance premiums.

Earnings Growth & Dividends

There would be companies reporting lower than expected earnings as well as higher than expected earnings, and Corporate Australia would also provide an outlook for the next half-year, which started this January.

Earnings growth remains one of the major concerns for an investor, and when companies materialise or exceed the expectations of the investors; the markets are likely to favour that company. However, the market participants punish the companies that fail to deliver on their targets as well as earnings.

Since the last reporting season, the markets had reached all-time highs, despite a similar shift in the earnings of the businesses and the time has arrived when companies would have to meet those expectations.

High growth businesses may deliver earnings growth, but an expectation of a dividend remains bleak, as it is better to grow and capture market share for a budding business in a bid to have larger dividend pay-outs in the future

At the outset, the reporting season should act as an eye-opener for the market participants, and it would provide a solid base for the next reporting season, which might include influences of Coronavirus. Moreover, the reporting season allows the market to bridge gap between reality and expectations.

Some notable companies scheduled to report during the first two weeks of February 2020 include

- Dexus on 6 February 2020.

- Mirvac Group on 6 February 2020.

- Aurizon Holdings Limited on 10 February 2020.

- JB Hi-Fi Limited on 10 February 2020.

- Suncorp Group Limited on 11 February 2020.

- Transurban Group on 11 February 2020.

- Commonwealth Bank of Australia (CBA) on 12 February 2020.

- Downer EDI Limited on 12 February 2020.

- Insurance Australia Group on 12 February 2020.

- James Hardie Industries on 12 February 2020.

- AMP Limited on 13 February 2020.

- Goodman Group on 13 February 2020.

- Magellan Financial Group on 13 February 2020.

- National Australia Bank on 13 February 2020.

- Treasury Wine Estates on 13 February 2020.

- Telstra Corporation Limited on 13 February 2020.

- Newcrest Mining Limited on 13 February 2020.