Moat, which literally means a water body surrounding a castle, keeps perpetrators beyond the castle. Similarly, for a corporation, economic moats enable them to maintain superiority against the competition.

In 1999, Warren Buffet, in an article for a magazine, coined the term economic moat. This was the time when the world was witnessing the hype of internet companies, which was the build-up for the dotcom crash.

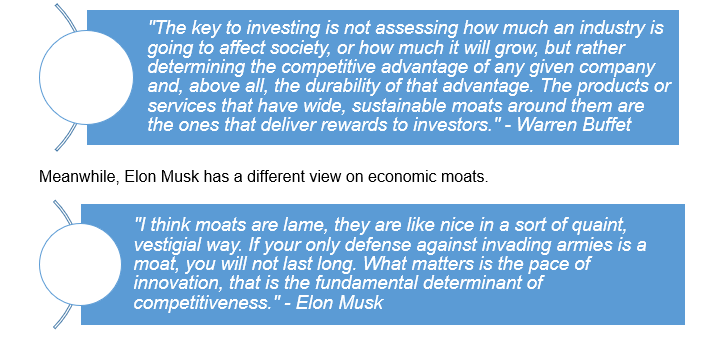

Meanwhile, Elon Musk has a different view on economic moats.

It is, indeed, appropriate that innovation remains at the heart of the many companies that are growing successfully. And, if one were to innovate continuously at a pace better than its competitors over an extended period of time, it is likely that the company would deliver sustained competitive advantages, which could be moats.

Economic moats are quite different from competitive advantages, and the key distinction lies in longevity. Moats are long-term while competitive- advantages could fade off as competition grows stronger.

Companies with high moats are generally associated with cash rich businesses and strong returns, and this translates to consistent levels of strong free cash flow generations, decent return on invested capital and a lower weighted average cost of capital. Moreover, companies with wider economic moats are more efficient compared to their peers.

Some Types of Moats

- Cost of Production

When a company is producing at a cost lower than its peers, it is highly likely that its margins would be better off its competitors (particularly on margins). And, a lower cost of production would enable the company to sustain competitive prices that could help to gain market share.

A low-cost production arrives by a large scale of operations, and productivity gains in the large-scale operation lower the costs. These productivity gains could be automation, bulk-buying and selling.

Such moats are built through pursuing an efficient strategy such as outsourcing when necessary, consider a comparative advantage, which emphasises on the potential production efficiency that could be achieved through producing at a place with structural benefits.

Companies often focus on a few areas to become the master and achieve specialisation. It would help to deliver an improved customer proposition. Whereas, when companies attempt to undertake multiple projects in a bid to deliver growth, they often fail to deliver the promised targets.

- Intangible Assets

Intangible assets are the most significant assets a company can have to build a sustainable moat. These assets allow a business to achieve a differentiation which could be impossible to emulate due to legal means or characteristics that are not fungible.

Intangible assets include trademarks, copyrights, patents, exclusive agreements, brand name, culture etc. For companies, it is a hard-earned process to achieve superior intellectual properties that would help to sustain the economic moat of the business.

Such assets often require high investments in research and developments, while a brand of the business is not something that could be manufactured. Building up a brand image requires time, customer value, culture and superior product. Consequently, building all this would lead to better customer loyalty and retention.

- Switching Costs

This moat allows a company to have a pricing power by locking customers into its ecosystem of product offering. Switching costs make it harder for customers to turn to the substitute of the products they are using, as the value they would receive from making a switch would be lower than the cost of making the switch.

Thus, the offering by companies that have substantially cost of switching, allows the supplier to enjoy pricing power, and in turn, favourable revenues. Meanwhile, switching costs are also measured in terms of time, effort and psychological barriers that become unfavourable while switching to a substitute of the product.

As an example, if you were to switch to a different cable TV provider, you would need to buy new equipment of the other supplier, and your existing equipment would be of no use. In addition, you may have to memorise the channel numbers of your favourite channels, as they would not be same with the new provider.

- Network Effect

Network effects mean when the customers using the same product increases overtime, and in turn, the growing numbers of the users increase the value of the company.

It also means that the users of the product have more compatibility among each other’s products, and in this way, businesses deliver value to the customers while increasing their own value as well.

When a company is incorporated as a start-up, the primary goal of the company is to acquire as many users as they can in order to build the network effects, which would deliver a long-term moat to sustain in the business.

- Efficient Scale

Operating in a monopoly is favourable for companies and this moat convicts that when natural monopolies exist, it allows the companies to serve their customers in an efficient manner due to the underlying scale and barriers to entry.

While companies look to build this moat, they often leverage M&A and consolidation to obtain such moats. Companies with this moat operate in a market that is not flooded with competitors.

And, the high cost of capital entering these businesses might not be justified given the level of profitability and return on investment. Consequently, this leads to high barriers to entry. Such business with this moat include utilities, railroads, pipelines, airports, and telecommunication.

Economic Moats & Stock Valuation

Risk

Investing in companies exposes investors to the risks associated with the companies and their business. The companies with a wider moat, meaning advantages over the other competitors, tend to have better visibility of the profitability amid an economic downturn that might suppress revenue generating capabilities of the business.

Thus, the companies possessing wider moat might have a lesser risk compared to their peers. And, this could drive a premium valuation on such companies as the risks perceived by the investors are relatively lower.

Moreover, the companies with sustainable advantages offer a defensive proposition to the investors, which could drive a premium valuation in the markets.

Return

Over an extended period of time, companies with wider moats could also lead to better profitability. However, the companies with less moat might have the tendency to generate attractive profitability but the consistency of returns might be similar over the period.

As companies with wider moats are able to have better pricing power due to their brand loyalty, efficient scale, etc. This might enable such wider moat companies to charge higher than their rivals, in turn, delivering better returns.

Valuation

The estimate of the company’s fair value embeds the forecast of company future economic value creation. Thus, the stock price of the company might have already considered the potential value that could be generated given the underlying moats.

The value of fairly priced wider moat stock that is usually believed to be less risky might move at a slower pace compared to narrow moat stock due to lower risk-adjusted discount rate used in the wider moat company’s expected free cash flow stream.

The intrinsic value of the company moves at a pace of its discount rate less its dividend yield. And, as a firm with wider moats pays more dividends while having a lower discount rate, the pace of increase in fair value could be slower than a narrow moat company.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.