Running a company requires capital to operate in any business. Companyâs capital structure defines the routes through which funds can be raised. If a company requires additional capital, it may issue equity or debt to meet the capital requirements. Nevertheless, the company would assess the merits of various options available such as private equity placement, share purchase plan, rights issue, notes issue, senior notes issue, secured & unsecured notes, term loan, convertible debt etc.

For equity shareholders, the company would have an obligation to repay income to its preferred shareholders. Similarly, the companies also raise capital through debt instruments and pay the determined interest over the tenure of the debt along with principal repayment at the end of the tenure.

The companies need sufficient capital to service the debt, which involves interest payments, principal repayments, lease payments and sinking fund. Rating agencies rate the debt of the company; these rating agencies provide an assessment of the companyâs creditworthiness based on the financial strength of the company. Accordingly, a rating is granted to the debt of any company, which allows investors to consider the health of the company prior to investing.

Debt Service Coverage Ratios measure the companyâs ability to repay its debt obligations. Debt obligations involve a variety of secured or unsecured notes, which might force the company to bankruptcy procedures conditional on repayment of the obligations or the terms of the debt deal. These ratios try to shed light on the companyâs ability to repay its short-term obligations, and maybe long-term.

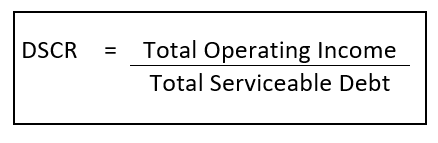

Debt Service Coverage Ratio

Debt Service Coverage Ratio (DSCR) is a financial ratio to assess the firmâs worthiness to service the debt. Servicing the debt of the company involves interest payments, principal repayments, sinking fund and lease payments. DSCR considers debt obligations due within a year and assesses the short-term ability to meet its obligation.

Operating Income = It is the income generated by the revenue of the company, and it is calculated by deducting the operating expense from the total revenue. Subsequently, this gives the Earnings Before Interest & Tax (EBIT). Many analysts also use EBITDA (Earnings before interest, taxes, depreciation, and amortization).

Serviceable Debt = interest payments, principal repayments, sinking fund and lease payments, which are due within one year.

Implications

Debt Service Coverage Ratio implies the ability to repay the current debt obligation due within one year. The ratio equivalent to 1 indicates that the company is at break-even, and it would require all operating income to be paid in the form of serviceable debt to meet the obligations due within one year. Any figure above 1 indicates that the company would have some balances left after payment of the current serviceable debt. Below 1 indicates that the company would not be able to meet the debt obligations fully through exhausting all of the total operating income earned during the year.

For instance, If DSCR is 0.95, It means that the company is only able to meet 95% of the current debt obligations due within one year. Also, it would require further sources of capital to service the current obligations due within one year.

If DSCR is 2, It implies that the company is able to service, twice the figure of the current debt obligations within one year. Further, it also depicts the companyâs strong cash flow positions.

At the outset, any company with DSCR close to 1 is at the risk of a reputed cash shortfall. Nevertheless, the companies may raise additional capital to service the debt, or it could burn the retained earnings of the company etc.

Generally, the investors consider the macro-economic conditions of the jurisdiction. Subsequently, if the macroeconomic conditions are not great or there exists a slowdown in the economy; the general investor expectation might consider a healthy DSCR â above 1.25 or 1.35. Similarly, if the macroeconomic conditions are robust and healthy; the investor sentiment might hit the lower levels of the DSCR prior to investing â an investor may consider DSCR below 1.25 or 1.35.

Applications & Examples

The ratio can be used to asses any company, and it can be used to assess the particular projects, acquisitions etc. Below is an example from an acquisition perspective on how to use DSCR to evaluate the capability of the target company to repay the debts raised by the parent company to fund the transaction.

Letâs say ABC Pty Ltd is amid the acquisition of XYZ Pty Ltd, and while looking at the terms of the acquisition; it appears that ABC had raised $200,000 from a notes issue at 3% per annum, the frequency of the coupon payment is yearly, and the tenure is set for five-years. Further, XYZ is expecting the EBITDA to be $450,000. Now, we would test the ability of the company to the service the debt raised for acquisition, through the income earned by the same acquisition.

DSCR = EBITDA/Total Serviceable Debt

In this case, we have only considered the debt raised for the funding of the acquisition. Subsequently, the total interest payment due for the upcoming year would be 3% of $200,000, which is $6000. Also, XYZ is expecting EBITDA at $450,000.

DSCR = 450,000/6000 = 75 times

This depicts that the acquisition is utterly capable of meeting parentâs serviceable debt obligations due within one year, which had been raised to finance the acquisition.

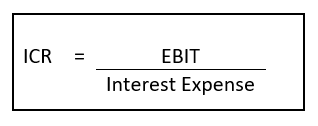

Interest Coverage Ratio (ICR) Versus Debt Service Coverage Ratio (DSCR)

Interest Coverage Ratio measures the capacity of the business to meet its current interest payments with the earnings. Interest Coverage Ratio is particular to the interest payments, and it doesnât consider the principal repayments to be made the company. Additionally, ICR is calculated by dividing the Earnings Before Interest & Tax (EBIT) by the Interest Expenses due within the same period.

DSCR & ICR are a kind of debt measurement ratios; ICR measures the ability to meet the interest obligations, and it does not consider the principal repayments, sinking funds or lease payments. Whereas DSCR is a more comprehensive approach to measure the debt; it considers the left-out part from the ICR, which are principal repayments, sinking funds or lease payments.

Limitations

Debt Service Coverage Ratio is a comprehensive tool to measure the ability to fund the debt obligations in the short-term or within a year. It should be noted that the long-term bonds mature after the completion of tenure. Therefore, the DSCR might reach at lower levels in the preceding year of the maturity of the bond.

Example Letâs assume that our EBIT is $497 and Serviceable Debt is $1417. So, the DSCR is 0.35 â which represents that the company can only service ~35% of the debt through its operating income. Nevertheless, the companies always have an option to refinance the existing debts. DSCR = EBIT/Serviceable Debt = $ 497.00 / $ 1,417.00 = 0.35Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.