Despite global slowdown and tepid macro sentiments, there are few consumer related sectors that have shown decent growth in the recent past. Businesses with product portfolio related to retail consumption have shown good potential.

In this article, we are discussing five small-cap stocks that are related to the consumption business. Letâs have an eye on the recent updates of the following five stocks.

Select Harvests Limited (ASX: SHV)

Select Harvests Limited is in the business of growing, processing and selling almonds to the food industry from company owned and leased almond orchards. Some of the other products of the company are dried fruits, seeds and edible nuts. As on 02 December 2019, the company has a market cap of $741 million.

FY19 Key Operating Highlights (period ended 30 September 2019):

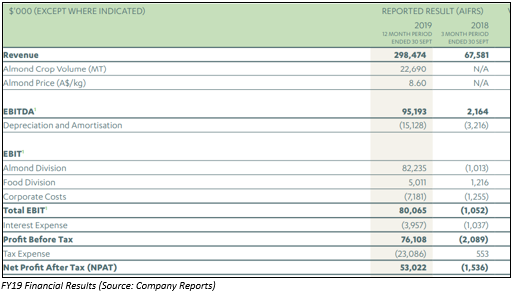

SHV declared its FY19 full-year financial results, wherein the company reported revenue of $298.474 million as compared to $67.581 million in FY18. Its Earnings Before Interest Tax Depreciation and Amortisation (EBITDA) was noted at $95.2 million, while Net Profit After Tax (NPAT) stood at $53.0 million.

The business reported almond crop volume at 22,690 metric ton (MT), up 45% year on year, aided by positive action from the greenfield investment strategy. Average SHV almond price stood at $8.60 per kg, up 6.8% on a y-o-y basis. The Almond Division delivered earnings before interest and tax (EBIT) of $82.2 million in FY19.

The Food Division reported an EBIT of $5 million in FY19. This stable result included strong demand for industrial product from the Chinese and Asian markets, while the domestic market remained challenging.

Outlook:

The global macro for almonds continues to remain positive moving forward, driven by strong demand from increasing middleclass wealth and a higher number of consumers adopting and consuming healthier diets, including the increased consumption of plant-based products.

Stock Update:

The stock of SHV closed the dayâs trading at $8.150, up 5.297% as on 02 December 2019. The stock has generated returns of 1.44% and 19.26% in the last three months and six-months, respectively. At current market price, the stock is quoting at the upper band of its 52-weeks trading range of $5.28 to $8.180.

Bega Cheese Limited (ASX: BGA)

BGA, which is engaged in activities such as processing, packaging and manufacturing of dairy products, recently updated the market with management changes. The company announced the appointment of Pete Findlay as Chief Financial Officer and the retirement of Colin Griffin, who served the position of CFO for the past 26 years. As on 02 December 2019, the company has a market cap of $809.85 million.

FY19 Financial Highlights

BGA declared its FY19 financial results for the period ended 30 June 2019, wherein the company reported revenue at $1,419.95 million as compared to $1,252.04 million in the previous financial year. EBITDA was down 3% on a y-o-y basis at $89.46 million while the company reported PAT at $11.819 million, representing a decline of 59% on a y-o-y basis.

Guidance:

The business is expected to enhance its portfolio of high-quality food products, in addition to investing in and protecting its famous Australian brands, in FY20. However, due to unprecedented competitive milk supply situation and easing demand from third party, branded businesses resulted in a change in the profit outlook for FY20.

Consequently, BGA expects to register normalised EBITDA at $95 million - $105 million in the financial year 2020 compared to $115 million in FY19.

Stock Update:

The stock of BGA settled at $3.960, up 4.762%, with approximately 214.24 million outstanding shares, as on 02 December 2019. The stock was trading at a price to earnings (P/E) ratio multiple of 66.32x on Trailing twelve months (TTM) basis. The stock has generated a dividend yield of 2.91% on an annualised basis.

Webster Limited (ASX: WBA)

Webster Limited is involved in production, processing and marketing of products including cotton, honey and walnuts. As on 02 December 2019, the company has a market cap of $711.81 million.

FY19 Financial Highlights:

WBA declared its FY19 financial reports for the period ended 30 September 2019, wherein the company reported total revenues from ordinary activities at $153.996 million, down 25.7% from $207.262 million in FY18.

- The company reported net loss at $9,11 million as compared to a net profit of $27.085 million in the previous financial year. The result was impacted by derecognition of carried forward tax losses and recognition of temporary tax differences due to entering into scheme of arrangement with Public Sector Pension Investment Board;

- Horticulture division reported a profit of $6.6 million in FY19 vs $10.7 million in FY18;

- Agriculture division posted a profit of $3.8 million vs $43.1 million in the same period a year ago;

- The business reported average cotton yields of 11.41 bales per hectare, which came slightly below the prior yearâs average yield of 11.77 bales per hectare;

- The cotton lint average sale price of $562 per bale was slightly ahead of the prior year $550 per bale;

- The company reported an additional $1.1 million of investment, which the company made during FY19 in additional containment lots specifically for the purpose of stock well-being and health;

- During the year, WBA acquired $24.1 million in additional water entitlements for future cropping activities associated with properties in the southern connected basin;

- Net debt of the company as on 30 September 2019 stood at $129.3 million compared to $199.6 million in FY18.

Stock Update:

The stock of WBA closed at $1.962, down 0.153% as on 02 December 2019. The stock was quoting at the upper band of its 52-week trading range of $1.155 to $1.975. The stock has delivered an annualised dividend yield of 1.53%.

Australian Agricultural Company Limited (ASX: AAC)

Australian Agricultural Company Limited is engaged in integrated branded beef business and is engaged in production, operation, sales and marketing activities. Recently, the company informed that Shehan Dissanayake would cease being an Executive Director of the company; however, Dr Dissanayake would continue on the post of Director. As on 02 December 2019, the company has a market cap of $632.91 million.

H1FY20 Operating Highlights:

AAC declared its first half financial results for the period ended 30 September 2019, wherein the company reported total sales of $182.8 million, down 36.4% on a y-o-y basis. The company registered operating gross profit and statutory loss at $30.6 million and $3.4 million, respectively as compared to $44.8 million and $82.9 million, respectively.

Operating profit was up, aided by 9.5% growth in underlying Wagyu meat sales on pcp terms. The company reported an adverse impact of ~$36 million during H1FY20 related to elevated expenses related draught to maintain production quality and supply in response to adverse seasonal conditions. The business reported strong y-o-y growth, which reflects one-off revenues from structural reorganisation of Livingstone and 1,824 supply chains.

Stock Update:

The stock of AAC closed at $1.085, up 3.333% as on 02 December 2019. The stock has given returns of 6.06% and 1.94% in the last one month and six months, respectively.

Asaleo Care Limited (ASX: AHY)

Asaleo Care Limited is engaged in manufacturing, marketing, distribution and sale of professional hygiene and personal care products in Australia, New Zealand and Fiji, in addition to several countries in the Pacific. As on 02 December 2019, the company has a market cap of $556.71 million.

Operating Highlights for 1H19:

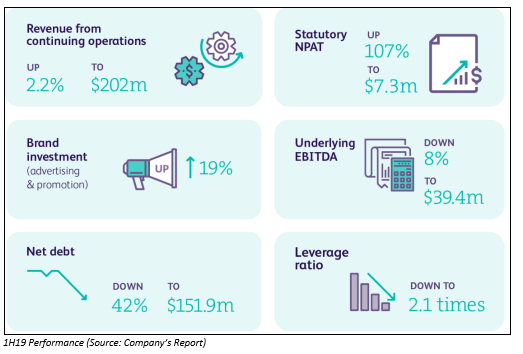

The companyâs performance during the six months to 30 June 2019 was in line with expectations. During the period, the company launched new products related to new innovative proprietary âHero Systemsâ. Moreover, it completed the sale of the Consumer Tissue Australia business.

In the first half financial results for the period ended 30 June 2019, the company reported underlying revenue at $202.0 million, up 2.2% on a y-o-y basis, driven by retail segment. The company registered underlying EBITDA at $39.4 million as compared to $42.9 million in FY18, representing a year on year decline of 8%.

During the period, the businessâ gross margins were challenged on account of higher pulp costs and increased investment in trade activity, partly offset with lease accounting change.

Stock Update: On 2 December 2019, the stock of AHY closed at $0.997, down 2.732% with a year to date return of 12.02%.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.