_10_04_2024_16_38_50_427275.jpg)

Summary

- Anglo American PLC reported a production increase of 24% sequentially in Q3 2020.

- The Group maintains the full-year 2020 production targets.

- Polymetal International PLC reported 35% year on year increase in revenue in Q3 2020.

- The performance was supported by better sales volume and high prices for gold and silver.

Anglo American PLC (LON:AAL) and Polymetal International PLC (LON:POLY) are FTSE-100 listed metal and mining stocks. Shares of AAL and POLY were up by around 0.80% and 1.70%, respectively from the last closing price (as on 22 October 2020, before the market close at 11:40 AM GMT+1).

Will Anglo American be able to achieve full-year production targets?

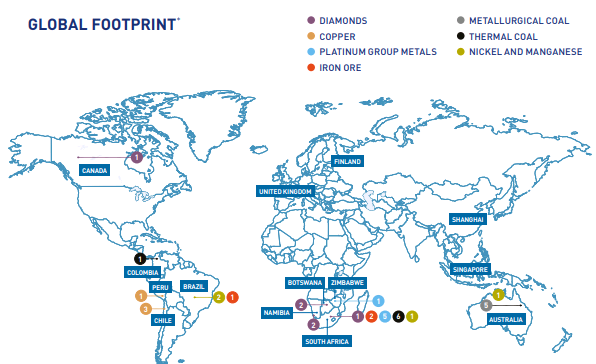

Anglo American PLC is a UK based mining group. The Group has operations in Europe, Southern Africa, North and South America and Australia. The Group deals in Diamond, Copper, Platinum, Coal, Iron ore, Nickel, Manganese and Polyhalite. Anglo American is listed on the FTSE-100 index.

(Source: Group website)

Q3 2020 Production update (ended 30 September 2020) as reported on 22 October 2020

In Q3 20, the Group reported a 24% increase in production sequentially, and it is currently operating at 95% of the standard capacity. The Group underwent planned maintenance at Minas Rio iron project and halted operation at Grosvenor in Australia, which impacted the production. However, it was offset by robust performance of Collahuasi copper project in Chile. A slight uptick in demand for the rough diamond has been seen as the holiday season is approaching.

Diamond production: The rough diamond production fell by 4% year on year to 7.2 million carats in Q3 20. The production was impacted due to the lower demand for rough diamonds following covid-19.

Copper production: The resilient operation at Collahuasi plant drove the copper production, which increased by 4% year on year to 165,700 tonnes in Q3 20.

Platinum Group Metals: The production of platinum fell by 2% year on year to 516,500 ounces, and the palladium output was flat at 352,200 ounces in Q3 20. The palladium and platinum yield increased at the Mogalakwena project due to improved throughput, whereas the production at Amandelbult declined as the Tumela Upper region is close to the end of mine life.

Iron Ore: Kumba iron ore production was 9.5 million tonnes, and it declined by 9% year on year. The production was impacted due to the supply chain disruption and higher stock level of Q2 20. Minas Rio iron ore production was 5 million tonnes, and it was down by 18% year on year. The year to date the average price for Kumba iron ore was USD 103 per tonne FOB South Africa and an average price of USD 96 per tonne FOB Brazil for Minas-Rio.

Metallurgical Coal: The production of metallurgical coal stood at 4.8 million tonnes, which was down by 26% year on year as the operations at Grosvenor were halted. The operations were suspended due to a gas ignition accident in May 2020.

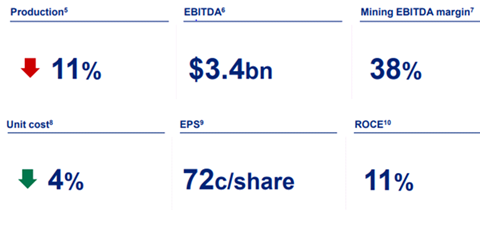

H1 FY20 Financial Highlights

(Source: Group website)

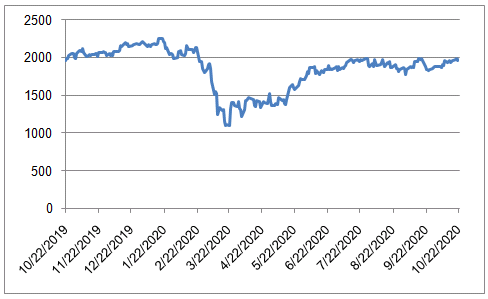

Share Price Performance Analysis of Anglo American PLC

1-Year Chart as on October-22-2020, before the market close (Source: EODHD/Others, chart created by Kalkine Group)

Anglo American PLC's shares were trading at GBX 1,966.20 and were up by close to 0.80% against the previous closing price (as on 22 October 2020, before the market close at 11:40 AM GMT+1). AAL's 52-week High and Low were GBX 2,266.00 and GBX 1,018.20, respectively. Anglo American had a market capitalization of around £26.18 billion.

Production Outlook

The Group announced the 2020 production outlook and it highlighted diamond production in the range of 25-27 million carats (Mct). The copper production is expected to lie between 630-660kt, platinum production around 1.7-1.8 Moz and Palladium production of 1.1-1.2 Moz. The Group has increased the production guidance for copper, platinum and palladium from the previous forecast. The output of Kumba and Minas-Rio iron ore is expected between 37-39 Mt and 22-24 Mt, respectively. The yield of metallurgical coal would be around 16-18 Mt. The Group has downgraded the production of thermal coal from previous guidance of around 21 Mt to about 19 Mt now.

Polymetal International PLC: Robust gold production, but silver production declined.

Polymetal International PLC is a UK based precious metal mining group. The Group has assets in Russia and Kazakhstan and it among the top global producer of gold and silver metals. It has nine gold and silver producing mines. Polymetal International is listed on the FTSE-100 index.

(Source: Group website)

Q3 2020 production update (ended 30 September 2020) as reported on 22 October 2020

The Group generated revenue of USD 884 million in Q3 20, which was up by 35% year on year. The improvement in revenue was supported by good prices for gold and silver and an increase in sales volume. Polymetal reported a strong cash flow in Q3 20. As on 30 September, the net debt stood at USD 1.61 billion, and it was down by USD 80 million from a year ago. It also paid an interim dividend of 0.40 USD cents per share that translated to a total dividend payment of USD 189 million. The Group has spent around USD 2.9 million so far that are covid related costs for providing healthcare facilities. The covid-19 related cost of the operation is close to USD 3 million per month, which is currently recorded as an operating expense.

Gold and Silver production

In Q3 20, Polymetal reported gold production of 477 kilo ounces (Koz), which increased by 7% year on year. The output was driven by strong yield at Omolon, Varvara and Kyzyl. The total production of silver was 4.6 million ounces (Moz), which declined by 13% year on year.

(Source: Group website)

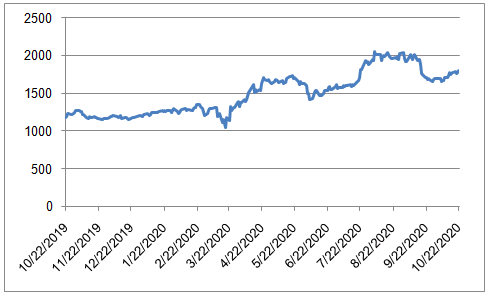

Share Price Performance Analysis of Polymetal International PLC

1-Year Chart as on October-22-2020, before the market close (Source: EODHD/Others, chart created by Kalkine Group)

Polymetal International PLC's shares were trading at GBX 1,796.00 and were up by close to 1.70% against the previous closing price (as on 22 October 2020, before the market close at 11:40 AM GMT+1). POLY's 52-week High and Low were GBX 2,085.00 and GBX 990.20, respectively. Polymetal International had a market capitalization of around £8.21 billion.

Business Outlook

The year to date performance of the Group was strong as the revenue grew by 26% year on year to USD 2,019 million. It is likely to meet its full-year reduction target of 1,500 Koz of gold equivalent. The total cash cost is expected to be around USD 650-700 per gold equivalent ounces and all-in sustaining of around USD 850-900 per gold equivalent ounces. Based on the resilient performance, the Group expects an output of 1,500 Koz and 1,600 Koz in 2021 and 2022, respectively.