The banking sector plays an important role in the economy of any country, facilitating the flow of funds in the economy and promotes the economic growth and development of the nation. It deals with cash, credits, other financial transactions and provides various financial services. In the United Kingdom, the banking system is reliable and transparent and has a much tighter regulation as compared to their US or EU counterparts. However, there is a vast difference in its terms of structure and operations from the banking system in the United States. In the United Kingdom, the whole industry is dominated by the four largest banks:

- HSBC Holdings

- Lloyds Banking Group

- Royal Bank of Scotland Group

- Barclays

According to last year data, the financial services sector contributed £132 billion to the UK economy and 6.9 per cent of total economic output. This sector has a major dominance in London, where 49 per cent of the sectorâs output was generated. Let us discuss the two banking sector stocks of the United Kingdom which were buzzing recently.

Bank of Georgia Group PLC

United Kingdom-based Bank of Georgia Group Plc (BGEO) is a holding company, the new parent company of BGEO Group PLC. The BGEO Group demerged its Investment Business and Banking Business on 29 May 2018. Two new entities were formed - Georgia Capital PLC and Bank of Georgia Group Plc. The companyâs business is divided into geography-based operations. The company operates wealth management operations, corporate investment banking, and retail banking & payment services in Georgia and BNB (banking operations in Belarus). The companyâs retail business is currently serving a client base of over 2.4 million. The company is Georgiaâs retail banking leader with 271 branches, 3,115 Express pay terminals and 876 ATMâs. Under its wealth management business, the company has a client base of 1,528 individuals from 76 countries globally. The corporate investment banking business presently accommodate over 2,500 business from multiple sectors such as energy, tourism, trade and others. The companyâs BNB business facilitates individuals and businesses with banking services in the Belarus region.

Recent News

On 24th September 2019, the company announced the launch of Optimo platform. Optimo is a digital solution for clients to run their business operations and sales. Optimo is designed to address the requirements of MSMEs in optimising their everyday operations and improve their enterprises in general. Optimo's cutting-edge digital solution, with analytical tools and integrated software and a rich type of functions, enables businesses to easily get their most current data on revenues, sales transactions, profitability, and inventory, anywhere and anytime, and make appropriate decisions with pertinent information at hand.

On 3rd September 2019, the company reported that JSC Bank of Georgia had introduced Apple Pay, for its clients, a widely used app to make mobile expenditures in a secure, simple, and private way. Through Apple Pay on Apple Watch, Mac, iPhone, and iPad, the companyâs clients can make convenient and fast purchases on websites, in stores, and through apps.

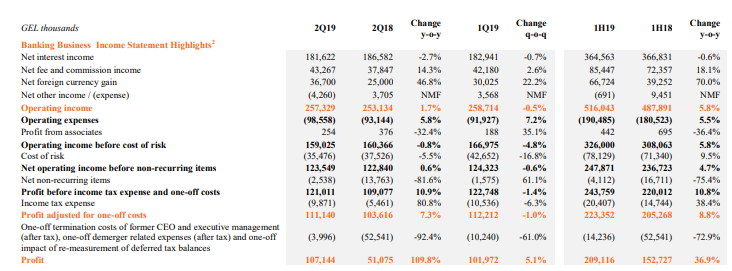

Financial Highlights (Q2 FY2019 and H1 FY2019, GEL thousand)

(Source: Interim Reports, Company Website) (GEL- Georgian lari)

For the second quarter of the financial year 2019 ending 30 June 2019, the companyâs reported net interest income was down by 2.7 per cent to GEL 181,622 thousand against GEL 186,582 thousand in Q2 FY2018. The companyâs total operating income surged by 1.7 per cent to GEL 257,329 thousand in Q2 FY2019 from GEL 253,134 thousand in Q2 FY2018, driven by a strong performance from Retail banking businesses. In Q2 FY2019, Operating income before the cost of risk was down by 0.8 per cent to GEL 159,025 thousand from GEL 160,366 thousand in Q2 FY2018. Profit before income tax expense and one-off costs was GEL 121,011 thousand in Q2 FY2019 against GEL 109,077 thousand in Q2 FY2018, an increase of 10.9 per cent. Profit from continuing operations surged by 109.8 per cent to GEL 107,144 thousand in Q2 FY2019 from GEL 51,075 thousand in Q2 FY2018.

For the first half of 2019, the companyâs reported net interest income was down by 0.6 per cent to GEL 364,563 thousand against GEL 366,831 thousand in H1 FY2018. In H1 FY2019, Operating income before the cost of risk was up by 5.8 per cent to GEL 326,000 thousand from GEL 308,063 thousand in H1 FY2018. Profit from continuing operations was up by 36.9 per cent to GEL 209,116 thousand in H1 FY2019 from GEL 152,727 thousand in H1 FY2018.

The company had a strong capital position in the first half of the financial year 2019 with Total Capital Adequacy and Basel III Tier 1 ratios of 16.7 and 13.3 per cent, respectively. The company is a market leader in its retail business and corporate invest in the business in its home market. In the H1 FY2019, the companyâs credit risk ratio has decreased as compared to the H1 FY2018âs ratio reflecting decent conditions on consumer lending. The rise in credit risk is also dependent on seasonal factors.

Outlook

The company is looking forward to becoming a leading organisation in Georgia not only in terms of financial performance but also as an innovative company with digital leadership and regional wealth management. In Q1 FY2019, the company had launched its unique real estate platform in Georgian real estate market with cutting edge technology. The companyâs cost management techniques had benefited both Retail and Corporate Investment Banking businesses. The current macroeconomic factors are benefiting the companyâs operations. The company is entering into loan agreements with various agencies with an aim to cater to the needs of different enterprises for local currency and align their businesses with the requirements of Free Trade Agreement of the European Union.

The company's support for MSMEs (micro, small and medium-sized enterprises) has expanded with the introduction of better digital solutions such as Optimo. The company would explore with additional ways to contribute to their development and success by proposing them easy and prompt entry to crucial data on their companies, and also give possible solutions to manage their businesses better.

Share Price Performance

Daily Chart as at 25-September-19, before the market closed (Source: Thomson Reuters)

On 25 September 2019, at the time of writing (before the market closed, at 2:05 pm GMT), Bank of Georgia Group PLC shares were trading at GBX 1,281, down by 3.25 per cent against the previous day closing price. Stock's 52 weeks High and Low is GBX 1,781.80/GBX 1,279. The company's stock beta was 0.62, reflecting the lower volatility as compared to the benchmark index. The outstanding market capitalisation was around £647.93 million, with a dividend yield of 5.45 per cent.

Metro Bank PLC

Metro Bank PLC (MTRO) is a London, the United Kingdom-based group engaged in the business of banking and related services. The group provides business and personal banking services. The bank is primarily focused on catering retail customers and small and medium-sized corporations.

MTRO troubles intensify as the United Kingdom lender ditches debt issue

On 23rd September 2019, the company ditched £250 million bond issue after it could not muster enough investors interest despite offering a hefty yield. After disclosing a major loan book error in January 2019, the company had suffered a torrential year that wiped over £1.5 billion pounds off its stock value, with the bank struggling to regain shareholders trust, on the same time shareholders worries about another looming problem- a no-deal Brexit, also weighed heavily upon its stock price. This deal that was launched on 23 September 2019, was to raise at least £250 million of MREL (bail-in debt) to gather an interim regulatory deadline of 1st January 2020. On the new four-year bond issue, the company proposed a chunky 7.5 per cent yield. In November 2018, the company was aiming a yield in the range of 2 per cent-4 per cent for MREL debt; orders had only touched £175 million for the day. The banks managing the deal had also decreased the volume of the deal sought from a £250 million to be in the range of £200-£250 million. In the second half of this year, the company had flagged to shareholders that it would have to raise MREL to meet its regulatory requirements.

On 24th September 2019, the company thanked the groupâs broad number of investors who gathered with interest in the bankâs inaugural MREL issuance. It further said that given the existing market conditions though the company has decided not to proceed with a transaction at this time and as a responsible issuer, the company shall consider any upcoming issuance mindful of all relevant investors.

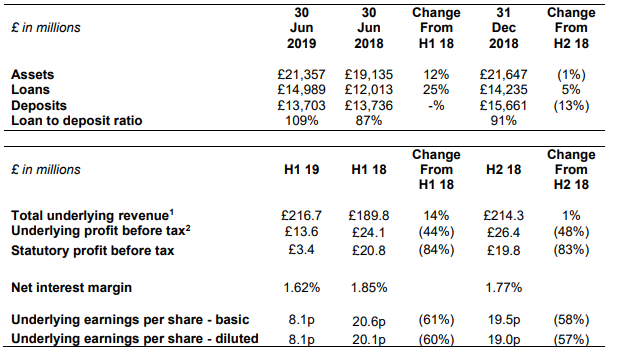

Financial Highlights (H1 FY19, £ million)

(Source: Company Website)

The companyâs total underlying revenue increased by 14 per cent to £216.7 million as compared with the corresponding period of the last year. During the half-year ended June 30, 2019, the group reported the growth of 190,000 in customers account against 201,000 recorded in a year-ago period. Total customers account as on June 30, 2019, stood at 1.8 million. During the half-year of FY19, personal current account recorded a growth of 23 per cent against the previous year and commercial current account expanded by 19 per cent on a YoY basis. Total deposits during the H1 FY19 period stood at £13.7 billion. On a half-yearly basis, net loans and advances to customers grew by 25 per cent to £15 billion. During the half-year of FY19, loan to deposit ratio increased to 109 per cent against 87 per cent in the same period of the previous financial year. Underlying pre-tax profit stood at £13.6 million against £24.1 million in H1 FY18, and statutory pre-tax profit stood at £3.4 million against £20.8 million in a year-ago period. Recorded basic underlying earnings per share stood at 8.1 pence against 20.6 pence recorded in a year-ago period.

Outlook

In the first half of 2019, total net outflows stood at £2 bn. Despite the challenges in the H1 FY19, the company will focus to build strong point of the model to deliver on the planned initiatives outlined in early part of 2019, with continued progress in capital-light fee income and initial delivery of cost efficiencies, given the current performance and store openings in the second half of the financial year 2019. In FY2019, deposits are expected to be roughly in line with December 31, 2018 data at £15.7 bn, with a 100 per cent of loan to deposit ratio by the end of this current year. In H2 2019, cost growth will moderate with low single-digit growth against the H1 2019. The bankâs broad effectiveness programme is now in place to deliver the cost savings as outlined. The company expects more decent deposit growth in the financial year 2019 with Metro Bank transitioning to a run-rate of around 20 per cent after 2019. The group will gradually try to manage its loan to deposit ratio between 85-90 per cent, due to the RWA efficiency. The growing cards and payments channel in the UK may provide growth opportunities for the bank. Introduction of new products and services will enable the bank to grow organically and enhance its customer base. In the latest survey of CMA (Competition and Markets Authority), the company was named as the United Kingdomâs best account provider.

Share Price Performance

Daily Chart as at 25-September-19, before the market closed (Source: Thomson Reuters)

On 25 September 2019, at the time of writing (before the market closed, at 3:05 pm GMT), Metro Bank PLC shares were trading at GBX 178, up by 1.71 per cent against the previous day closing price. Stock's 52 weeks High and Low is GBX 3,012/GBX 175. The company's stock beta was 0.22, reflecting the lower volatility as compared to the benchmark index. The outstanding market capitalisation was around £300.31 million.