J D Wetherspoon PLC

J D Wetherspoon Plc (JDW) is an owner and operator of pubs. The company was incorporated in the year 1979 and provides alcoholic and non-alcoholic drinks, food items and coffee at its pubs. Its portfolio of food items includes, small meals, pub classics, chicken and ribs, breakfast club, Sunday brunch, gourmet burgers, beefsteak club, chicken club, curry club, sides, desserts, salads, pasta, pancakes and sausages among others. The company offers real ale and beers of various brands in pints, spirits, craft cans and prosecco and sparkling rose.

Achievements

The companyâs 99 per cent pubs are Cask Marque approved. The group raised £1.6 million in the last twelve months and more than £17.6 million during the sixteen-year partnership with CLIC Sargent. Average food hygiene rating score was of 4.97 out of a maximum of 5. A total of 97.4 per cent of its pubs have achieved the maximum score of 5. 19.9 million GB customers had visited the company in the last six months.

Financial Highlights (FY2019, 壉000)

(Source: Annual Report, Company Website)

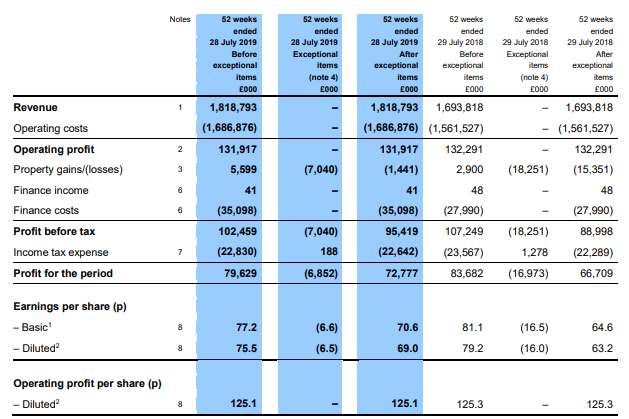

In the financial year 2019, the companyâs total sales increased by 7.4 per cent to £1,818.8 million as compared to the previous year. Like-for-like (LFL) sales rose by 6.8 per cent in FY19, bar sales climbed by 5.8 per cent, food sales surged by 8.3 per cent, slot/fruit machine sales increased by 10.3 per cent, and hotel room sales rose by 3.9 per cent. Operating profit (before exceptional items) reduced by 0.3 per cent to £131.9 million as compared with the financial year 2018 of £132.3 million. The operating margin (before exceptional items) stood at 7.3 per cent in FY19 versus 7.8 per cent in FY18.

Profit before tax and exceptional items declined by 4.5 per cent to £102.5 million against the £107.2 million in FY18, comprising property profit of £5.6 million. Earnings per share, containing shares held in trust by the employee share scheme, before exceptional items, stood at 75.5 pence against the 79.2 pence in FY18.

In FY19, the net interest by operating profit before interest, tax and exceptional items was covered 3.9 times against the 4.8 times in FY18, owing primarily to a surge in the cost of interest-rate hedges or âswapsâ and a decrease in operating profit. Total capital investment stood at £167.6 million in the current period as compared to £110.1 million in FY18. In new pubs and pub extensions, the company had invested £35.2 million, a slight decrease from the previous year. The company also invested £77.2 million in freehold reversions and £55.2 million in existing pubs and IT. Total exceptional items decreased to £7 million as compared with the financial year 2018 of £18.3 million. There was a loss on disposal of £1.6 million and a £5.5 million of the impairment charge.

In the financial year 2019, the total cash impact of exceptional items was £6 million of cash outflow. Since beginning the present disposal programme in 2015, the company has had a £20 million of net inflow from the disposal of 101 pubs. For existing pubs, free cash flow, after capital payments, stood at £54.3 million versus £68.9 million in FY18. The company had £16 million for share purchases for employees and payments of tax and interest surged by £3.6 million to £97 million in FY19. Free cash flow rose to 92 pence per share against the 88.4 pence per share in FY18.

On 28th July 2019, the groupâs total net debt, excluding derivatives, stood at £737 million, an increase of £10.8 million against the £726.2 million in FY18. At the end of the current financial year, net debt to EBITDA stood at 3.36 times versus 3.39 times in 2018. In 2019, EBITDA was £5 million higher, offsetting a slight increase in debt. In order to avoid a rise in costs, the group had fixed its LIBOR (London Interbank Offered Rate) interest rates in respect of £770 million till March 2029.

Dividend

The groupâs board proposed to pay a final dividend per share of 8 pence, on 28th November 2019, to investors on the registration date of 25th October 2019, providing a total dividend per share for the year 2019 of 12 pence. The dividend was covered 5.8 times in FY19 versus 5.3 times in FY18.

Outlook

The group aims to increase its client offering continually so that it remains competitively placed in the market in which it operates. Unfavourable economic conditions can theoretically have an impact on the groupâs performance, although, historically, these impacts have been muted.

The company had a reasonable start to the financial year 2019 and expects a reasonable outcome for the year 2019, subject to future sales performance.

There are some risks, though like, the revenue may get affected by consumer confidence, unemployment, real wages. The companyâs costs were rising from inflation, a national living wage, rents, rates, utilities. The regulatory issues such as the market rent regulations, beer duty, sugar tax etc. also affected the companyâs performance negatively. The company also faces severe competition from other restaurants/bar operators and likes of Deliveroo, Uber Eats and Just Eat; and the pubs get affected either way by changing weather patterns.

The company chairman, Tim Martin, is one of the most vocal business supporters of Brexit. The chain announced 20 pence cut in the cost of a pint of beer in nearly 700 of its pubs to highlight the advantages of leaving the European Union.

Share Price Performance

Daily Chart as on 13-September-19, before the market close (Source: Thomson Reuters)

On 13 September 2019, at the time of writing the report (at 1:59 pm GMT, before the market close), JDW stock was trading at GBX 1,542, down by 0.52 against the previous day closing price. Stock's 52 weeks High and Low is GBX 1,645/GBX 1,051. The companyâs stock beta was 0.73, reflecting less volatility as compared to the benchmark index. The outstanding market capitalisation was around £1.63 billion, with a dividend yield of 0.77 per cent.

Greencoat Renewables PLC

Ireland-based Greencoat Renewables PLC (GRP) is mainly focused on investing in operational wind farms. The group seeks to invest in euro-denominated operational renewable electricity generation assets in the Ireland, and several other Eurozone countries including the Netherlands, Finland, Germany, France and Belgium. The group also seeks to invest in both offshore and onshore wind farms through the amount invested in offshore wind farms being capped. These will usually be held with SPVs (special purpose vehicles), which hold solar farm assets or underlying wind. The groupâs investment manager is Greencoat Capital LLP.

Financial Highlights (H1 FY2019, â¬â000)

(Source: Interim Reports, Company Website)

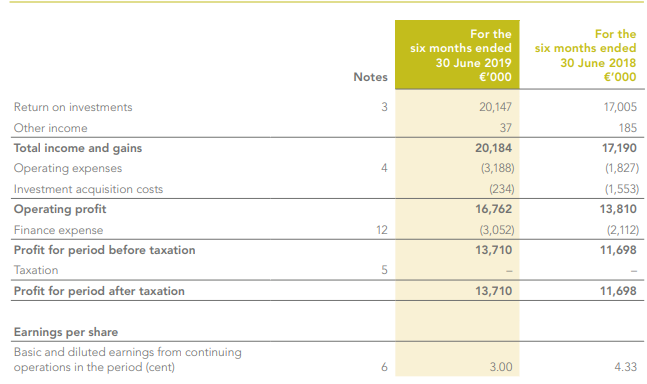

In the first half of the financial year ending 30th June 2019, the companyâs return on investments increased by 18.48 per cent to â¬20,147 thousand from â¬17,005 thousand in H1 FY2018. The companyâs total income and gains for the H1 FY2019 were â¬20,184 thousand against â¬17,190 thousand in H1 FY2018. The companyâs operating profit stood at â¬16,762 thousand in H1 FY2019 against â¬13,810 thousand in H1 FY2018. The companyâs PBT (Profit before tax) surged by â¬2,012 thousand to â¬13,710 thousand from â¬11,698 thousand in H1 FY2018. The companyâs PAT (Profit after income tax) stood at â¬13,710 thousand in H1 FY2019 against â¬11,698 thousand in H1 FY2018. The basic and diluted earnings per share from continuing operations stood at 3 cents in H1 FY2019 versus 4.33 cents in H1 FY2018.

In the first half of the year 2019, the portfolio generated 555.9GWh and 5 per cent below budget. Both wind resource and asset availability were widely on the budget for the current period, with higher than anticipated grid curtailment, particularly in the south-west area, responsible for the decrease in performance. Driven by the contracted payments under the REFIT (Renewable Energy Feed-In Tariff) regime, there was no exposure to wholesale power price variations. Accordingly, the companyâs net cash from group and wind farm SPVs stood at â¬27.1 million, offering robust dividend cover of 2.0x in the first half of 2019.

At the start of the current period, the companyâs borrowings stood at â¬490.7 million (GAV of 56 per cent). After an additional investment in Cloosh Valley and equity issuance in the current period, as on 30th June 2019, the companyâs borrowings amounted to â¬416.5 million equating GAV of 44 per cent.

Acquisition and Equity Raising

On 11th September 2019, the company announced its deal to acquire the 20MW Gortahile wind farm from Glennmont Partners. Gortahile comprised of 8 Nordex N90 turbines and raised the portfolioâs net generating capacity to 431MW. In the past two years, the company had seen constant growth with the net generating capacity gradually improving to 411MW as at 30th June 2019.

Outlook

The Irish wind market remains an attractive dominion for investment on supportive and stable regulatory regime coupled with wide public support. In H1 FY19, wind generation delivered around 32 per cent of the countryâs electricity and will remain the leading renewable technology as Ireland continues towards attaining its target of 40 per cent renewable electricity generation by the year 2020. The Irish Governmentâs newly announced Climate Action Policy is anticipated to create over â¬12 billion of additional investment prospects. The company expects that most of this new capacity will be delivered in the new RESS (Renewable Energy Support Scheme), a competitive auction structure for CFD (Contracts for Difference) support, with such auctions anticipated to commence in the year 2020 and run till 2026. The companyâs management continues to view the Irish wind market as a lucrative market for additional investment.

In line with its investment policy, the from July 2019, the company is considering investment prospects in other European Union jurisdictions. Investments outside of Ireland offer additional diversification of generation resource from renewables. The company will be impacted by the uncertainties created by the ongoing Brexit, as it will impact the companyâs portfolio. The companyâs position further strengthens due to absence of currency risk when acquiring assets in Europe. For the future, the Board has expressed its confidence in the groupâs outlook, and in an orderly approach of the Investment Managers to any possible acquisitions.

Share Price Performance

Daily Chart as on 13-September-19, before the market close (Source: Thomson Reuters)

On 13 September 2019, at the time of writing the report (at 3:45 pm GMT, before the market close), GRP stock was trading at GBX 1.15, remain the same against the previous day closing price. Stock's 52 weeks High and Low is GBX 1.20/GBX 1.02. The companyâs stock beta was 0.12, reflecting less volatility as compared to the benchmark index. The outstanding market capitalisation was around â¬595.19 million, with a dividend yield of 5.23 per cent.