.jpg)

_05_16_2023_17_11_27_393572.jpg)

Real Good Food PLC

Real Good Food PLC (RGD) is a United Kingdom-based food distribution and manufacturing company. The group is involved in the manufacture, distribution, and sourcing of food to the foodservice, industrial, and retail sectors. The companyâs operations are differentiated in three operating segments, namely Food Ingredients, Premium Bakery, and Cake Decoration.

The companyâs Cake Decoration division sells, supplies, and manufactures cake decoration ingredients and products in the United Kingdom and international markets. The cake decoration segment caters to the bakery sector. The companyâs Food Ingredient division produces and supplies a variety of food ingredients, like sauces, dry powder blends, jams, chocolate coatings and snack bars to the wholesale, retail and foodservice divisions. The groupâs Premium Bakery business produces, sells and distributes dessert and bakery goods to the retail customers and UK foodservice.

Financial Highlights (FY2019, 壉000s)

(Source: Interim Reports, Company Website)

(Source: Interim Reports, Company Website)

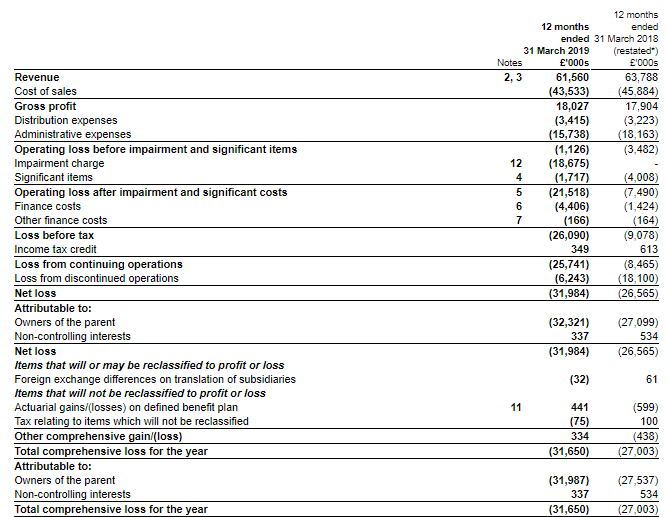

For the 12 months ending 31 March 2019, the companyâs revenue from the continuing operations stood at £61.6 million, a decrease of 3.4 per cent against the £63.8 million in FY2018. The revenues declined because of reductions in Food Ingredients of £0.9mn (5.9%) and Cake Decoration of £1.2mn (2.6%) over the corresponding prior-year period. In Cake Decoration segment, there was a reduce because of the loss of one significant client, while the Food Ingredients segmentâs revenue decreased, due to the practical difficulties arising out of the installation of new equipment and plant and rapid surge in the number of employees.

For the overall Group, gross profit from continuing operations increased to £18.0 million as compared to £17.9 million in FY18. At 23.7 per cent, the delivered margin in the year 2019, for the continuing businesses, was above the previous yearâs 23 per cent delivered margin and significantly above the one reported for the whole group during the last year at 14.9 per cent, strongly indicative of the improved quality of earnings for the Group as on whole. In the year 2019, the operating loss was £21.5 million after an amortisation and depreciation charge of £3 million, significant costs of £1.7 million and impairment charge of £18.7 million.

After finance costs was £4.6 million and the inclusion was £6.2 million loss from the discontinued operations, it resulted in a loss after tax for the financial year 2019 stood at £32.0 million against the loss of £26.6 million in 2018. Basic loss per share on continuing operations was 28.64 pence against the restated of 11.82 pence in FY18 and a loss per share on discontinued operations was 6.85 pence.

On 31st March 2019, net debt was £35.7 million, a decrease from £37.8 million in 2018 and consisted predominantly of shareholder loans. This is in the form of convertible loan notes of £9.6 million.

Outlook

The company had faced a very difficult period in the past and had undergone a great deal of corporate restructuring activities. The company now contains two-divisions, with clearly articulated purposes and defined plans to accomplish those purposes. The group now has the senior management, the leadership, and the resources capable of improving performance from both the divisions and a considerably lower central cost base aligning with the objectives.

During the new financial YTD (year to date), current trading from the two remaining, strong and profitable businesses was in line with the uncertain prospects available for the upcoming year. The company remains continuously attentive on improving its results and on declining in net debt, as well as supporting the business's strategy and thereby increasing returns and shareholder value.

The company had made substantial progress in the corporate governance domain, and now has in place a suitable governing board, balanced as far as the numbers of Non-Executive, Independent Non-Executive, and Executive Directors are concerned. The Board expressed its confidence for the Groupâs performance as on the whole.

Share Price Performance

Daily Chart as at 16-August-19, before the market closed (Source: Thomson Reuters)

On 16 August 2019 (at the time of writing, GMT 3:55 AM), Real Good Food PLC shares were hovering at around GBX 6.750, down by 6.89 per cent against the previous dayâs closing prices. Stock's 52- week High and Low are GBX 9.00/GBX 5. Stockâs average traded volume for 5 days was 38,130.80; 30 days â 119,252.90 and 90 days â 153,986.24. The average traded volume for 5 days was down by 68.03 per cent as compared to 30 daysâ average traded volume. The companyâs stock beta as on date was 0.55, reflecting lower volatility as against the benchmark index. The outstanding Mcap (market capitalisation) was around £7.20 million.

Corero Network Security PLC

Corero Network Security PLC (CNS) is a United Kingdom-based company engaged in DDoS (Distributed Denial of Service) defence solutions. The group's DDoS protection solutions offer detection and automatic mitigation of Distributed Denial of Service attacks for Internet hosting providers, the online enterprise and service providers. The companyâs product portfolio comprises of SmartWall TDS (Threat Defence System). The SmartWall TDS is a network security device adaptable to meet the requirements of hosting and service workers, and online enterprises, all of which is driven by the challenges of DDoS attacks. The SmartWall TDS devices are differentiated into two products: SmartWall Network Bypass and SmartWall Network NTD. The company offers SecureWatch PLUS, which provides a suite of Distributed Denial of Service defence optimisation, around the clock monitoring, attack mitigation, and configuration services. The companyâs technology offers the First Line of Defence as compared with the DDoS attacks. The company has a presence in the United Kingdom, North America, and Other countries.

Trading Update (as on 16th August 2019)

The company announced a trading update for the six months ended 30th June 2019. In H1 FY2019, the companyâs revenue is expected to be around $4.2 million, a decrease of $0.8 million from the corresponding period of the prior year. The revenue was impacted by a lower than the projected conversion of the Juniper pipeline of prospects into revenue and orders. Operating costs were expected to be around $5.3 million in H1 FY19 and remained flat against the same period in 2018. The EBITDA loss for the six months ended 30th June 2019 was projected to be around $2.0 million against the loss of $1.4 million in H1 FY18. On 30th June 2019, cash at bank stood at $6.9 million, a decline from the $9 million in 2018. The debt was $3.2 million, and net cash was $3.6 million in H1 FY19.

Financial Highlights (FY 2018)

In FY2018, the companyâs revenues increased from $8.5 million in FY2017 to $10 million in FY2018, comprising almost entirely of sales from SmartWall, Corero's market-leading DDoS mitigation solution, which grew by 23.1 per cent in 2018. Recurring revenues, comprising security maintenance and support services and DDoS protection as-a-service revenues, increased to 51.1 per cent of total revenue versus 47.1 per cent in the prior year.

Corero closely managed its costs in 2018, with adjusted operating expenses of $9.9 million, 13.3% below the prior year (2017: $11.4 million). Further, the EBITDA loss for the year reduced to $2.1 million (2017: loss $5 million).

Revenue growth and progress towards EBITDA break-even was impacted by the longer than anticipated time required to secure contracts and develop revenues from new go-to-market partners in the year.

Loss per share stood at 1.4 cents, a decrease from the prior year of 3.0 cents. Net cash used in operating activities in the year ended 31 December 2018 was $1.8 million (2017: net cash used $6.0 million) reflecting the loss for the year and working capital investment for the period of $0.3 million (2017: an increase in working capital investment at $0.7 million).

Outlook

For the full year ending 31 December 2019, the companyâs management expects revenue to be around 20 per cent higher than revenue for the prior year of $10.0 million and anticipates a spike in EBITDA loss for the full year 2019, as a result of the additional Corero direct sales investment in the second half of the financial year 2019 of around $1.0 million. The company will have a requirement for extra working capital prior to being cash generative, and the group would undertake a modest amount of fundraising. The group's Chairman and the principal shareholder have shown their support for the ongoing activities. On 25th September 2019, the company will announce its interim results for the financial year 2019.

Share Price Performance

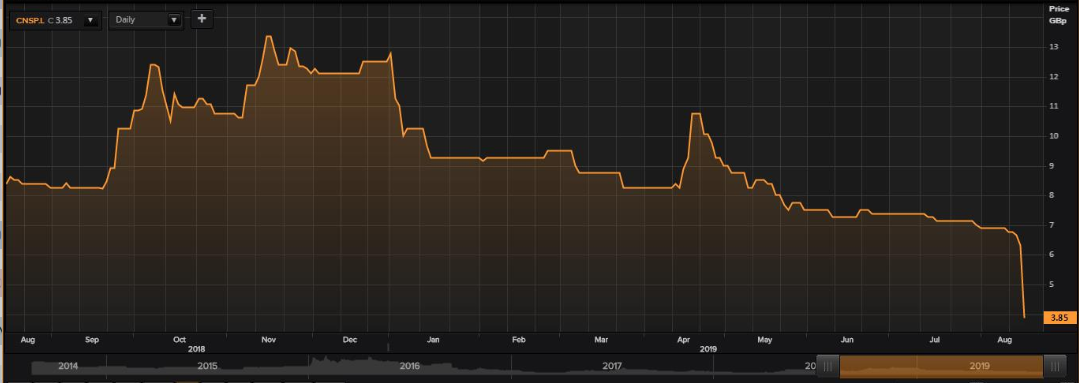

Daily Chart as at 16-August-19, before the market closed (Source: Thomson Reuters)

On 16 August 2019 (at the time of writing, GMT 8:40 AM), Corero Network Security PLC shares were hovering at around GBX 3.85, down by 38.88 per cent against the previous dayâs closing price. Stock's 52-week High was GBX 13.60, and it has touched a fresh 52 week low in current dayâs trading. Stockâs average traded volume for 5 days was 140,862.60; 30 days â 68,901.57 and 90 days â 66,974.13. The average traded volume for 5 days was up by 104.44 per cent as compared to 30 daysâ average traded volume. The companyâs stock beta as on date was -1.30, reflecting the inverse relationship with the benchmark index. The outstanding market capitalisation of the stock was around £25.27 million.