_07_03_2026_03_50_21_133108.jpg)

US Markets: Broader indices in the United States traded on a mixed note - particularly, the S&P 500 index traded 7.61 points or 0.18 per cent lower at 4,222.28, Dow Jones Industrial Average Index dipped by 115.70 points or 0.33 per cent lower at 34,640.69, and the technology benchmark index Nasdaq Composite traded higher at 13,836.69, up by 22.20 points or 0.16 per cent against the previous day close (at the time of writing - 11:50 AM ET).

US Market News: The major indices of Wall Street traded on a mixed note as investors waited for the key inflation data to be released later this week. Among the gaining stocks, U.S. Concrete (USCR) shares surged by about 29.10% after the Company got agreed to be acquired by Vulcan Materials for approximately USD 1.29 billion. Microsoft (MSFT) shares rose by around 0.79% after the Company had won an approval to buy artificial intelligence company Nuance Communications in a USD 16 billion deal. Visa (V) shares went up by about 0.48% after the Company was upgraded by Piper Sandler from “neutral” to “overweight”. Among the declining stocks, KKR & Co (KKR) shares went down by about 1.64% after the Company agreed to buy Atlantic Aviation for almost USD 4.50 billion.

UK Market News: The London markets traded in a green zone as the strength of the housebuilding stocks neutralized the adverse impact of weakness in the mining stocks.

Taylor Wimpey shares rose by about 1.43% after Liberum Capital released an upbeat note on the UK Housebuilding sector and raised investment stance on the Company from “Hold” to “Buy’.

Reckitt Benckiser Group had agreed to sell the baby formula business in China to private equity firm Primavera for USD 2.2 billion. Moreover, the shares dropped by around 0.93%.

IWG shares plunged by around 9.00% after the Company had warned that underlying earnings for 2021 would remain below the levels of 2020 due to the prolonged impact of Covid-19 restrictions in several markets.

Mining Companies such as Antofagasta and Anglo American shares dropped by around 3.10% and about 3.09%, respectively, after the release of Chinese trade data. Moreover, they remained the worst performers on the FTSE 100 index.

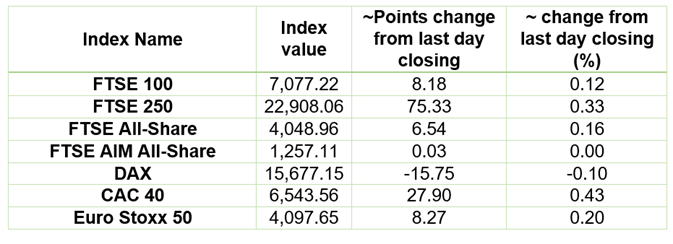

European Indices Performance (at the time of writing):

FTSE 100 Index One Year Performance (as on 07 June 2021)

1 Year FTSE 100 Chart (Source: EODHD/Others)

Top 3 Volume Stocks in FTSE 100*: BT Group PLC (BT.A); Lloyds Banking Group PLC (LLOY); and Vodafone Group PLC (VOD).

Top 3 Sectors traded in green*: Technology (0.99%), Utilities (0.77%) and Real Estate (0.76%).

Top 3 Sectors traded in red*: Basic Materials (-0.87%), Healthcare (-0.74%) and Energy (-0.39%).

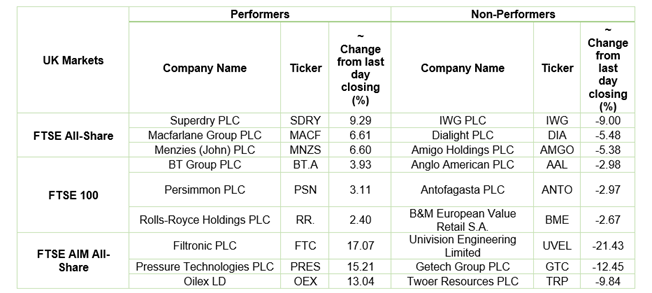

London Stock Exchange: Stocks Performance (at the time of writing)

Crude Oil Future Prices*: Brent future crude oil (future) price and WTI crude oil (future) price were hovering at $71.50/barrel and $69.23/barrel, respectively.

Gold Price*: Gold price was quoting at US$ 1,901.95 per ounce, up by 0.53% against the prior day closing.

Currency Rates*: GBP to USD: 1.4188; EUR to GBP: 0.8597.

Bond Yields*: US 10-Year Treasury yield: 1.567%; UK 10-Year Government Bond yield: 0.8130%.

*At the time of writing