.jpg)

_05_16_2023_17_11_27_393572.jpg)

Warehouse REIT PLC

Warehouse REIT PLC (WHR) is a Chester, United Kingdom-headquartered Real Estate Investment Trust which is managed by Tilstone Partners Limited and focuses on being the leading warehouse provider across the whole of the UK. The portfolio and investment strategy of the group is focused on UK urban warehouses, and tenants range from local businesses to household names for key locations around the UK. The portfolio of the group is mainly located in Southern England and has close proximity from assets to urban centres or major roads. As at 31 March 2019, the group had 4.6 million square feet of the portfolio across 91 assets and 869 units.

Recent Development

The company on 18 September 2019 announced that it agreed to acquire the portfolio of reversionary warehouse and distribution assets, comprising one multi-let and seven single let warehouses providing a total floor area of 995,106 square feet, from Aviva Investors for £70 million, strengthening the Warehouse REIT portfolio from both the property and revenue perspective.

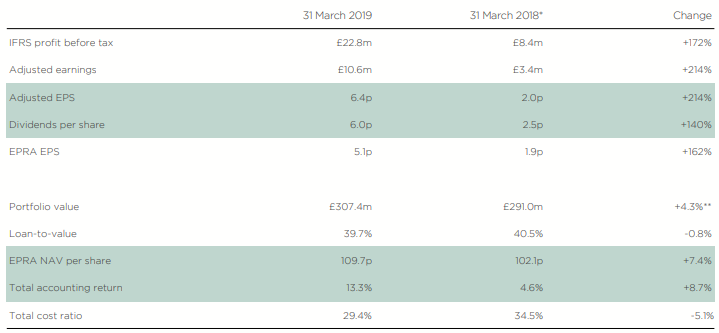

Financial Highlights (FY 2019, in £m)

(Source: Company Filings)

Total revenue, which includes insurance recharges and dilapidation income, for the year was reported at £22.0 million (FY 2018: £6.6 million), and rental income was £20.6 million (FY 2018: £6.3 million), as tenant demand remained strong despite current political and economic uncertainties. Gross profit rose from £5.7 million to £18.58 million. Operating costs were £6.8 million (Excluding one-off costs), while total operating costs for the year stood at £9.0 million (FY 2018: £2.4 million). Operating profit during the period was £27.74 million against £9.33 million, while the corresponding value before gains on investments properties was £13.01 million versus £4.15 million in FY 2018. The group reported a gain of £11.2 million on the revaluation of its investment properties while the gain on the sale of the four investment properties disposal was of £3.5 million in the year. As net financing costs amounted to £5.0 million for the year (FY 2018: £0.8 million), statutory profit before tax was £22.8 million (FY 2018: £8.4 million), which reflected an increase of 172%. Adjusted earnings per share were 6.4 pence (FY 2018: 2.0 pence), and earnings per share under IFRS was 13.7 pence (FY 2018: 5.0 pence). The EPRA NAV per share at the end of the period was 109.7 pence, up 7.4% (31 March 2018: 102.1p) and EPRA earnings per share were 5.1 p (FY 2018: 1.9p). The total dividend during the year was 6.0 pence (FY 2018: 2.5 pence) as the company declared a fourth interim dividend of 1.5 pence per share for the quarter to 31 March 2019, and the cash cost of the total dividends for the year was £10.0 million (FY 2018: £4.2 million). The loan to value ratio was 39.7% (31 March 2018: 40.5%), and the company had £127.0 million of debt at the end of the period (31 March 2018: £124.5 million).

Share Price Commentary

On 24 September 2019, at the time of writing (before the market close, at 3:25 pm GMT), WHR shares were trading at GBX 103, up by 0.48 per cent against its previous day closing price. Stock's 52 weeks High and Low is GBX 107.04/GBX 91.36. The companyâs stock beta was 0.28, reflecting a weak relationship with the benchmark index. The outstanding market capitalisation was around £247.21 million, with a dividend yield of 5.85 per cent.

Outlook

A material impact on the ability to meet the financial forecasts set by the group can be faced from a significant loss of rental income through bad debts or adverse volatility in the interest rates. Since the company continuously acquire new assets, there is an inherent risk that such acquisition may not materialise, which could reduce the returns and increase risk. However, securing lease renewals and new lettings will continue to remain a focus, and the company would seek to invest in new assets which would increase both earnings and the quality of the portfolio. As build costs are making it unfeasible to develop new space across much of the country, the supply of small to medium-sized warehouses will remain constrained, while demand for space is strong. This is supported by UK employment, which is at record levels, and e-commerce continues to grow.

Inland Homes PLC

Inland Homes PLC (INL) is a Beaconsfield, United Kingdom-headquartered brownfield regeneration specialist. The group is increasingly focusing on self-delivery of projects to create high-quality homes and provides mixed-use and residential developments in the South and South East of England. The portfolio consists of both brownfield and strategic sites, which provides opportunities that would not be available from solely dealing with brownfield land and opens up medium-term opportunities that are significantly less capital intensive. The longer-term strategic land bank has the potential for approximately 2,170 residential plots across 405 acres, and itâs land portfolio consists of 6,776 plots, with the size of the sites ranging from under 50 plots to over 1,350 plots.

Recent Development

The company on 23 September 2019 announced that planning consent had been granted for Wilton Park, which is flagship site of the group, and purchase of joint venture partner at Cheshunt. Wilton Park has an estimated gross development value of £350 million, and within the 100-acre site, delivery of 350 homes, as well as commercial and community space, will be enabled by the planning consent. The company has an arrangement with its joint venture partner at Cheshunt Lakeside, and for £29.9 million, 50% interest in Cheshunt Lakeside Developments Limited of the joint partner will be acquired by the group, which will provide the group with an opportunity to extract significant land and development profits from the site.

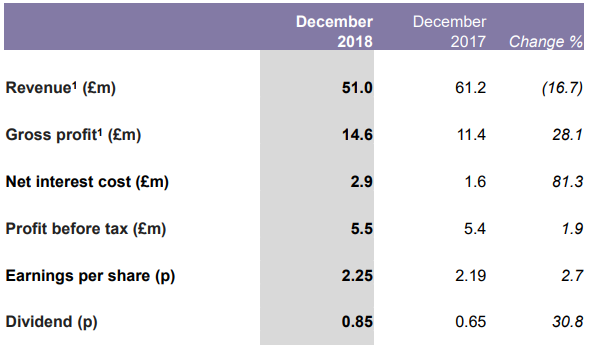

Financial Highlights (H1 2019, in £m)

(Source: Company Filings)

In the first half results for the six months ended 31 December 2018, the company reported that as a result of the expected decrease in private home completions due to the timing of the development programme and a reduced number of plots sold, revenue for the period decreased by 16.7% to £51.0 million (H1 2018: £61.2 million). However, due to management fees from a site managed by the company, gross profit increased by 28.1% to £14.6 million (H1 2018: £11.4 million). The corresponding gross margin rose from 18.6% in H1 2018 to 28.6% during the current period. The rise gross profit reflected in operating profits as well, which increased to £8.4 million from £7 million in the first half FY 2018 and operating margin rose to 16.5% (H1 2018: 11.4%). Due to a rise in finance cost from £2 million in H1 2018 to £3.7 million, an increase in profit before tax was modest at £5.5 million (H1 2018: £5.4 million). Total profit and comprehensive income for the period rose to £4.6 million from £4.4 million in H1 2018. Basic earnings per share were up by 2.7% to 2.25 pence from 2.19 pence, and the interim dividend was up by 30.8% to 0.85p per share (H1 2017: 0.65p). Reflecting the increase in the EPRA adjustment for the revaluation of projects and increase results from the profit for the period, undiluted EPRA net asset value per share was up by 6.1% to 103.57 pence at 31 December 2018 from 97.63 pence at the previous half year-end. On EPRA net assets of £212.9 million (30 June 2018: £206.7 million), net debt increased to £96.6 million due to a rise in developmental activities, with net gearing of 45.4% (30 June 2018: 38.6%), while Net Asset Value per share was up by 7.0% to 71.71 pence (H1 2018: 67.02 pence).

Share Price Commentary

On 24 August 2019, at the time of writing (before the market close, at 3:28 pm GMT), INL shares were trading at GBX 78, up by 5.83 per cent against its previous day closing price. Stock's 52 weeks High and Low is GBX 77.37/GBX 47. The companyâs stock beta was 0.37, reflecting a weak relationship with the benchmark index. The outstanding market capitalisation was around £152.09 million, with a dividend yield of 3.26 per cent.

Outlook

Due to the impending Brexit negotiation, there remains a degree of uncertainty on the outlook for the UK economy and the property market, which has the potential to influence various aspects of the strategy, operations and overall performance of the group. Revenues, profits, cash flows and asset values can be affected by further potential devaluation of the sterling as a result of Brexit, which could increase costs of materials for the group, and the impact on consumer confidence, demand and pricing for new homes. Impact on costs and delay in build activity can also result from a restriction on the availability of skilled construction workers after potential legislative changes on freedom of movement. Any deterioration in economic environment can decrease demand and pricing for new homes as the housing market is vulnerable to changes in unemployment and interest rates, though wage growth seems to be resilient amid record-low unemployment level. However, with continued demand across the core activities of the group, market segments remain stable, and demand for new homes continues to outstrip supply significantly. This is supported by low mortgage rate and growth in wages.

Comparative share price chart of Warehouse REIT PLC and Inland Homes PLC

(Source: Thomson Reuters)