_07_03_2026_03_50_21_133108.jpg)

The Office of the National Statistics of the United Kingdom in its latest report published on 13 January 2019 has revealed that the GDP of the country actually shrunk in the month of November 2019. As per the data compiled by the office, the economy of the country grew by -0.3 per cent in the month of November 2019 compared to a growth of 0.1 per cent in the month of October 2019 and 0.1 per cent growth on September 2019. The biggest contributor to this fall has been the index of production which fell by -1.2 per cent during the month followed by the index of services which fell by -0.3 per cent. The sectors which performed better were the construction sector which grew by 1.9 per cent during the month followed by the agriculture sector which grew by 0.1 per cent during the month.

The data, which is a reflection of what the state of affairs in the United Kingdom was just before the General elections, is a testament of how bleak the situation had turned out to be at that time. The British economy, which had been reeling under the Pre-Brexit headwinds of anxiety and uncertainty has been under a downward spiral for the past couple of years. The sentiments of the British public have been at a long-term low during the period, with businesses curtailing their expansion plans and consumers postponing their non-essential expenditures. Several important economic indicators of the period started turning negative which, by the mid of 2019, threatened to push the British economy into a long-term recession. Of the different figures that were working against the United Kingdom was the difficulty of arriving at an agreement regarding a planned Brexit withdrawal which would have ensured a less painful event for the businesses on both sides.

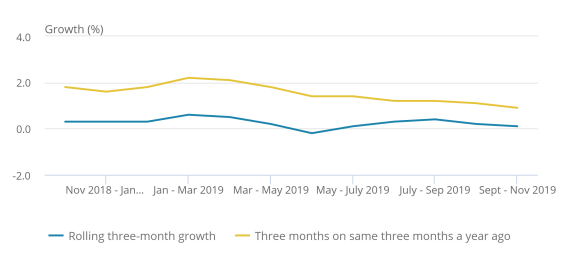

In terms of three months rolling GDP growth rate figures, the British economy this year has fared much worse in comparison to the similar periods in the previous year. The three-month rolling GDP growth rate was 0.1 per cent in the month of November 2019, down from an upwardly revised 0.2 per cent for the month of October 2019.

Picture source â Office of National Statistics, UK

While the growth rate in 2018 was higher, it fell at a faster pace through the first half of 2019. However, in the year 2019, the growth rate began to improve by the second half of the year. It is noteworthy, however, that the three months rolling GDP growth rate figures were in the negative territory between the May to July quarterly period of 2019.

Breaking down the GDP growth rate figures in the most recent quarter ending in November 2019, the index of production stood at -0.6 per cent, falling by -0.08 percentage points; the Index of services stood at 0.1 per cent, increasing by 0.08 percentage points while the index of construction stood at 1.1 per cent, increasing by 0.07 percentage points. The decline in the production sector is its second three-month decline in a row.

The services sector of the British economy has been one of the most battered due to the pre-Brexit adverse economic headwinds. The falling business activity levels meant that there was less work for the banking, insurance, legal services and several such service industry verticals. The industry activity flattened in the month of September 2019 when it grew at 0.0 per cent; it then grew by 0.3 per cent in the month of October 2019 and finally shrunk by 0.3 per cent in the month of November 2019.

The manufacturing sector of the British economy has been suffering due to the climate of uncertainty hovering over it. The producers of the country have been uncertain about the economic situation of the country post-Brexit and have been curtailing their unplanned expansions and postponing the planned ones. The production in the country also suffered as the consumer confidence declined witnessing a fall in consumption levels. The sector grew by -0.2 per cent in the month of September 2019, it grew by 0.5 per cent in the month of October 2019 and finally the growth fell by -1.7 per cent in the month of November 2019.

The construction sector faired relatively well during the past three-year period. While the London Market performed relatively poorly, other areas of the country performed fairly well, with the Scotland market performing the best. The sector grew by 1.6 per cent in the month of September 2019, shrunk by 2.2 per cent in the month of October 2019 and finally grew by 1.9 per cent in the month of November 2019.

The agriculture sector of the British economy has been relatively flatlined over the period. In the month of September 2019, it remained flat; in the month of October 2019 it also remained flat while in the month of November 2019, it registered a miniscule growth of 0.1 per cent.

Towards the end of November 2019, the situation has dramatically improved for the British economy. The results of December 2019 general elections alleviated a lot of the uncertainty-related headwinds hovering over the British economy. The new government, led by Boris Johnson, has received a clear mandate and a clear agenda regarding how it wants to take the British economy forward. In the second week of December 2019 itself, a lot of important economic indicators have started to turn northwards indicating that the effect of the election results on the psyche of the British population has been massive. The consumer confidence index, the housing pricing index and the permanent employees hiring index for the month of December 2019 have all been in the positive zone. The next big event for the British economy, that will indicate how the future will unfold, will be the actual Brexit event taking place on the 31st of January 2020. The economic headwinds then will determine which way the British economy will trend into in the year 2020 and beyond. The GDP growth figures for the Month for December 2019 and January 2020 could very well tell a different story.