Summary

- Amidst COVID-19 storm, economies all across the globe have started to reopen in the hope of registering a pyrrhic victory post a bleak first half 2020.

- After suffering thick and fast, America, China, Australia and New Zealand brace to raise the ante with staged reopening in place, businesses picking steam and Government support pouring in.

- The upcoming week holds an ocean of economic information to be released, a significant indicator of how these economies are performing during the pandemic.

The unprecedented COVID-19-induced “Global Virus Crisis” continues to symbolise perhaps the largest shock witnessed by the global economy in decades. The WHO affirms over 18.9 billion confirmed cases and 709k deaths in 216 countries, as on 7 August 2020.

With the pandemic stress testing political, economic, cultural and social infrastructure alike, the events of the last seven months seem to be a catastrophic reminder of the instability and insecurity that the crisis can trigger. So much so, global GDP is expected to contract by over 4% in 2020, before rising by ~6% in 2021.

However, the economies have been demonstrating outstanding ability in seizing this crisis to unite in national unity and global solidarity. Consequently, after rigorous lockdowns and quarantines, countries have been reopening in a staged manner, thriving to climb the ladder of recovery in exceptional ways to tackle business and humanitarian aspects of the current testing times.

As the “new normal” continues to garner market attention and economies lay out their projections, let us cast an eye on significant releases in the upcoming week from the US, China, Australia and New Zealand-

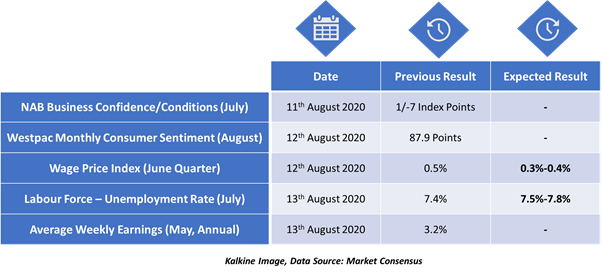

Australia: Likely to Contract by ~6% over 2020, before growing by ~5% over 2021

While Australia experienced a severe contraction during first half, some economists opine that it is currently in the early stages of recovery. However, renewed outbreaks continue to be a cause of worry, as key regions like Melbourne and Victoria experience a spike in confirmed cases.

Besides, business investment in the country is expected to decline significantly this year, though equity prices have recovered around half of their earlier decline. Subsequently, the pace of recovery is expected to be slower than previously forecast.

RBA Governor Philip Lowe recently provided below economic projections-

- The Australian economy is likely to contract by ~6% over 2020, before growing by ~5% over 2021 and 4% over 2022.

- Unemployment rate is expected to peak at ~10% by the end of 2020.

- Employment declined by over 850k in April and May and increased by ~200k in June. The JobKeeper program was reportedly a major driver to control worrying unemployment figures. It has been extended beyond September and may continue to support employment until March 2021.

- Consumption is estimated to have contracted by ~ 10% over 1H20, though consumer spending increased over recent months.

- Headline CPI declined by 2% in the June quarter, taking the year-ended headline inflation to –0.3%. However, most of the decline in headline inflation may reverse in the September quarter.

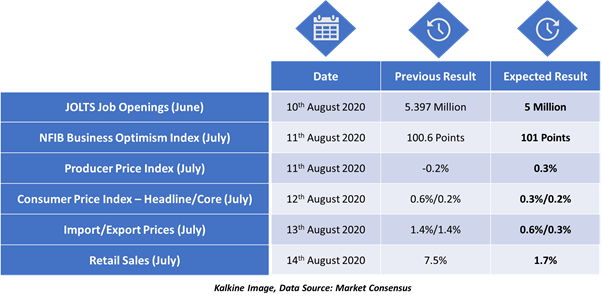

The US: Real GDP expected to grow at 12.4% annual rate in 2H20

The US economy contracted at a 32.9% annual rate in the June quarter, recording its worst quarterly plunge ever with unemployment surging to 14.7%. Moreover, COVID 19 ended the longest record of 11-year economic expansion, as the nation entered a recession this year.

With reopening prioritised across the US and lost jobs being gradually recovered, the world’s biggest economy may deliver a sharp bounce-back in the next quarter, experts opine. However, it remains to be the “current epicentre of the virus”, said WHO Director-General Dr Tedros in his latest media briefing.

According to Congressional Budget Office projections-

- From 2020 to 2030, annual real GDP will be 3.4% lower on an average than projected in January. Real (inflation-adjusted) GDP is expected to grow at a 12.4% annual rate in 2H20 and to recover to its pre-pandemic level by the middle of 2022.

- Unemployment rate is projected to peak at over 14% in the Q320. Annual unemployment rate, earlier projected to average 4.2%, is currently expected at 6.1%.

- Inflation, measured by the growth rate of the price index for personal consumption expenditures, is projected to be 0.4% in 2020.

New Zealand: GDP growth peaking at an annual average of 13.1% in the year to March 2022

Leading by example, PM Jacinda Ardern garnered global appreciation for her robust policies that got New Zealand on a brink to be “COVID free”. The economy did suffer its biggest contraction in 29 years in the first three months of 2020 and GDP shrank 1.6% in the January-March quarter, the biggest fall since early 1991.

However, early economic and health response to the pandemic reportedly aided New Zealand in doing better than predicted. While, vigilant cautions pertaining to a second wave of infections remain in place.

Stats NZ Data for June 2020 Quarter:

- COVID-19 extended unemployment rate rose to 4.6%. Jobs numbers have been recovering post the significant fall in April, registering rises in May as well as June.

- Unemployment rate fell to 4% in June quarter, while employment dipped to 66.9%.

- Overall labour cost index salary and wage rates (incl overtime) rose by 0.2% in the quarter. LCI was up by 2.1% for the year to the quarter.

- CPI fell 0.5%, down 0.4% with seasonal adjustment compared to the March 2020 quarter.

- Gross earnings were down to NZD 304 million (0.9%) on earnings in the March quarter.

The Treasury projects GDP growth peaking at an annual average of 13.1% in the year to March 2022.

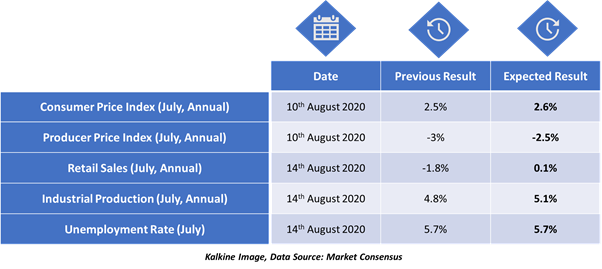

China: Not Setting an Economic Growth Goal For 2020 Owing To Uncertainties

China's economy escalated by 3.2% in the June quarter (2Q20) with GDP returning to growth following a record slump of 6.8% in the first three months of the year (1Q20) owing to COVID 19 lockdowns- the first GDP decline since at least 1992. The origin of novel coronavirus, China has restarted its economy and seems to be growing stronger than expected and is believed to have avoided entering the technical recession.

Fiscal spending, cuts in lending rates, banks’ reserve requirements and stimulus packages continue supporting recovery. Consequently, trade numbers and manufacturing activity in June expanded. Household spending jumped by 13% in June, though retail sales declined by ~2% in May.

In May, the world’s second largest economy made a rare suggestion that it would not set an economic growth goal for 2020 owing to uncertainties and fallout from the pandemic.