Summary

- Benefits of a negative interest rate regime not very clear, especially in a very subdued demand scenario, due to the deadly impact of the coronavirus pandemic

- Banks already have a large amount of bad debts in their balance sheets, and negative interest rates could further add to them

- Consumers will lose out on savings in a negative interest rate regime, while fixed-rate loans and mortgages will largely remain unaffected

- Further quantitative easing looks more probable in the current uncertain times

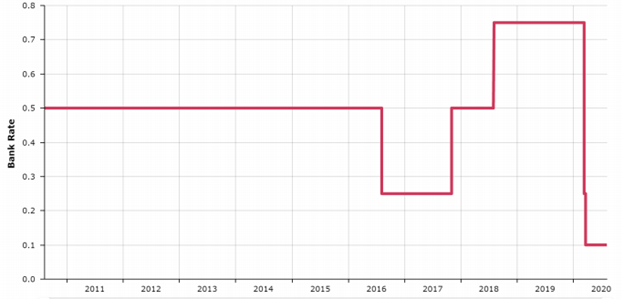

The British economy is undergoing a recessionary period and shrunk at about 20 per cent during the lockdown month of April 2020. The country’s central bank is trying its best to revive the economy as soon as possible and has been proactively lowering its bank rate beginning March 2020. The Bank of England recently announced its monetary policy update on 6 August 2020. While it kept the already low interest rate steady at 0.1 per cent, but the Bank’s Governor Andrew Bailey emphasized that the option to use negative interest rates is still open for near future, given the uncertain times the UK economy is subjected to, as a result of the coronavirus pandemic. It is to be noted here that a country’s central bank sets the benchmark for the cost of lending across the entire economy, by fixing the bank rate.

The next update is due on 17 September 2020.

Official Bank Rate in Britain

It will be interesting to take a closer look at a negative interest rate scenario and its impact on the consumers and banks, if it actually becomes a reality in Britain. Let’s see.

Also Read: Are Lithium Stocks Worth Considering in Your Portfolio?

Also Read: Top 10 richest people in the UK

Also Read: Financial Highlights of selected Banking Stocks of the United Kingdom

Banks

In a negative interest rate regime, a retail bank shall pay interest to the Bank of England. In all likelihood, they will in turn charge the same from their customers. But these retail banks might also fear that customers could pull out all their money from these banks in such a scenario, and might just end up absorbing all this cost by themselves instead.

While the BoE maintains that the British banking industry continues to have strong fundamentals, however, the micro picture does need a closer look. Many large and small banks are sitting on a huge pile of loans that might turn bad in the near future, since companies are turning red and unable to bear the brunt of the coronavirus led pandemic. Therefore, the risks in the banks’ balance sheets are definitely high. Some lenders could lose money, and this is worrisome.

In case interest rates turn negative and corporate borrowings rise, economy will show an upturn only if the higher investments get supported by a consequent rise in consumer demand, across the board. This in turn is conditional upon the availability of a Covid-19 vaccine and eradication of the pandemic as soon as possible. So just a negative interest regime might not be a sufficient condition to drive the economy into a V-shaped recovery.

Another criticism of negative interest rates comes from the argument that while in theory they drive the economic output by encouraging lending, but in practice, banks actually scale it back since their own earnings are also very low in such a regime, and the risks are multi-fold. So, they effectively end up curbing lending, instead of promoting it, defeating its very purpose itself.

Consumers

In case you had taken anything on a mortgage, there is a big chance that a negative rate will not impact you. The reason for this is that most of the mortgages across the nation are decided on a fixed-rate contract rather than a variable one.

However, for new mortgages, the scenario could be a little different. In case the BoE base rate is negative, lenders could either opt for a zero interest rate or even a negative one, depending on their policy. Mostly, the lending institutions typically charge customers marginally over the official bank rate set by the central bank. So, that is a reason to cheer because it means that effectively you owe a lower instalment with every passing month.

Now, the real sad news comes for savings, which means you total deposited sum will go down overtime, if you put it in the bank. Right now, most of the British banks are paying savings interest rate of 0.01 per cent only, lower than the BoE bank rate of 0.1 per cent.

The rates for credit card payments and personal loans are also usually set on a fixed-rate basis, so there also you would not see any changes coming in, should the interest rates dive into the negative territory.

What else is a possibility?

It is likely that the BoE provides additional quantitative easing stimulus worth £100 billion by September of November 2020. It has already purchased government bonds worth £745 billion to support the economy.

Lowering the fees on the term funding scheme can also be expected.

The BoE Governor warned that some sectors like hospitality and tourism might continue to remain unviable for at least few years to come, and we have no option but to live with such harsh realities.

Unemployment rate is going to fall to 7.5 per cent by the end of 2020, as per the central bank’s forecast. It is yet to be seen how the government minimizes the impact of this given the limited resources at its hand now. The total public borrowings are slated to reach £372 billion for the year 2020, as per government estimates.

Also Read: Embracing Disruption Through Digitalisation: Investment Banking Trends for 2020

The future is not likely to be a bed of roses and the BoE is going to be faced with increasingly tough choices in weeks to come, given the uncertain times. The net impact of a negative interest rate appears to be mixed, and could further weaken the nation’s financial sector. Therefore, while it still remains a possibility, however, the Bank of England might opt for a clearer option such as further quantitative easing, going forward. Further, till the time the coronavirus pandemic is a reality, a low interest regime is very much here to stay, whether the bank rate goes minus or not.