_02_06_2025_07_05_23_538703.jpg)

Highlights

- The taxation office recognises cryptocurrencies as CGT assets, and this includes non-fungible tokens

- Australia’s latest Federal Budget has a section on cryptocurrencies, and a mention that a law would be introduced

- Bitcoin is legal tender in El Salvador; however, the value of the cryptocurrency has remained extremely volatile

Even though the term ‘cryptocurrency’ has currency, it does not automatically mean it is treated as such by regulators. Barring a handful of small economies like El Salvador, almost every country has avoided recognising any cryptocurrency as legitimate money. Regulations around these blockchain-powered digital currencies can be confusing, leading to erroneous conclusions.

In Australia, Bitcoin or any other cryptocurrency is not recognised as money. But this does not mean the government and/or regulators have not addressed the subject matter. In an explanation on its website, the Australian Taxation Office (ATO) clearly states that cryptos (including non-fungible tokens) are capital gains tax (CGT) assets. Now, the latest October Budget shines a light on the subject. Let us explore.

Digital currencies attract CGT

In the October 2022 Budget, the Australian government removed any doubt that might have prevailed after El Salvador designated Bitcoin as legal tender. Budget Paper No. 2 outlines that digital currencies are excluded from the tax treatment of foreign currency. The document also makes it clear that recognition as assets for the purpose of income tax would continue. It is also mentioned that the government would bring a law in this regard.

That said, Australia’s budget explains how central bank digital currencies (CBDCs) have no comparison with cryptocurrencies like Bitcoin. The document states a digital currency issued by a government agency would attract taxation as a foreign currency. Australia is also planning its own CBDC, however, its exact features and underlying technology have not yet been specified.

Not legal tender, but legal

Legal tender means legitimate money that can be used in transactions. In Australia, cryptos like Bitcoin are not legal tender, but it does not mean that these are totally illegal. Trading is allowed, but regulators have time and again warned about the speculative nature of these assets and extreme price volatility, no matter a crypto like Bitcoin or smaller altcoins like Dogecoin. Any gains on a cryptocurrency transaction attract CGT, the ATO has clarified.

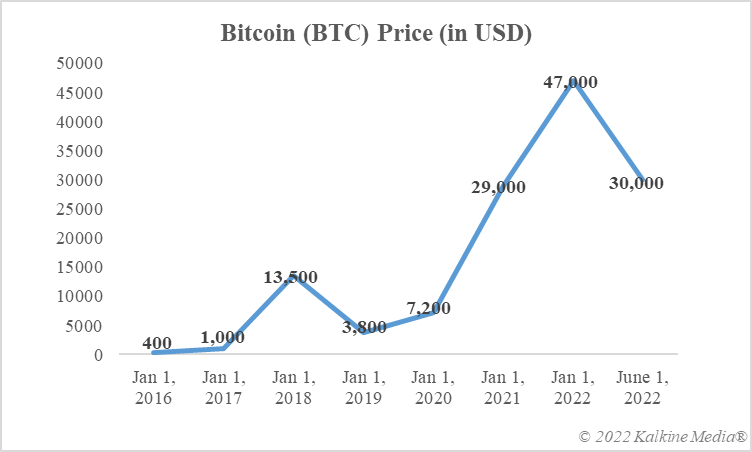

Data provided by CoinMarketCap.com

Bottom line

Australia’s latest Federal Budget mentions digital currencies and clarifies how they are recognised in the country. As of now, these are assets, and capital gains tax is payable on any profits made. There are murmurs that the Australian government is looking to have better regulatory system to oversee cryptocurrencies after the collapse of a major exchange, FTX. What all it would include is a subject of speculation.

Risk Disclosure: Trading in cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory, or political events. The laws that apply to crypto products (and how a particular crypto product is regulated) may change. Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading in the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed. Kalkine Media cannot and does not represent or guarantee that any of the information/data available here is accurate, reliable, current, complete or appropriate for your needs. Kalkine Media will not accept liability for any loss or damage as a result of your trading or your reliance on the information shared on this website.