Websites and financial magazines produce a wide range of investing information each day, but do you actually have the time to assess it and take the best investment decision? With abundance of financial instruments and knowledge available in the market, market players often find it hard to finalise investment products that offer them the required returns.

While herd mentality in the investment space is not the right approach, investors are increasingly approaching financial advisers to maintain their financial fitness.

As per the NZ government, the demand for financial advisers is anticipated to increase over the coming years due to:

- a shortage of highly skilled advisers in the nation,

- an increasing number of workers close to retirement stage who may need investment advice, and

- the possible retirement of a large number of existing financial advisers in the next 10 to 15 years.

In this article, we will give you a general overview of the role of Financial Advisers and the significance of Financial Adviser Services. We will also touch upon the key difference between Class Advice and Personalised Advice.

Who is a Financial Adviser?

A financial adviser is the one who offers financial guidance or advice to customers to enable them to meet their financial goals. Such advisers advise clients on a range of areas, including taxes, portfolio management, investments, mortgages, savings accounts, retirement, and estate planning.

Using their financial know-how, financial advisers guide you on the best investment and plan of action for your wealth management.

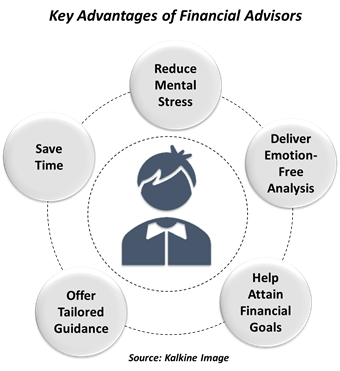

Why are Financial Advisers Important?

Financial advisers can help you address different complex investment needs that occur when you amass abundant wealth. This is because these experts possess deep knowledge of complex financial market instruments and can interpret the nitty-gritty of different products.

You can easily map your financial goals with the help of an adviser, who may suggest you to split your objectives into long-term, short-term, and medium-term for better financial management.

While DIY (Do-It-Yourself) is gaining popularity, financial advisers can help you take investment decisions without committing too many mistakes. The ease of convenience offered by a financial adviser enables you to take a right investment decision and learn about different investment vehicles and the investing space to improve your knowledge.

In addition to these benefits, financial advisers help eliminate the single biggest cause of mistakes, the lack of objectivity. In the financial market, keeping an objective view and executing trades on the basis of emotion-free analysis come to the crunch to strengthen the performance of your investment portfolio. Financial advisers enable objective decision making, timing your entry and exit in the right investment vehicle.

What is Financial Adviser Service?

According to the Financial Advisers Act 2008, a person A provides a financial adviser service if, in the ordinary course of a business, A offers any of the below-listed services:

- giving financial advice

- providing an investment planning service

- providing a discretionary investment management service

Besides, the Act states that person A also provides a financial adviser service if, in the course of business of a financial service provider registered under the Financial Services Providers (Registration and Dispute Resolution) Act 2008 or FSP Act, A provides any of the services already listed above.

It is imperative to note that all financial service providers in NZ must be registered on the FSPR (Financial Service Providers Register) to legally offer financial services, as per NZ’s Financial Markets Authority (FMA).

What are the Different Types of Financial Adviser Services in NZ?

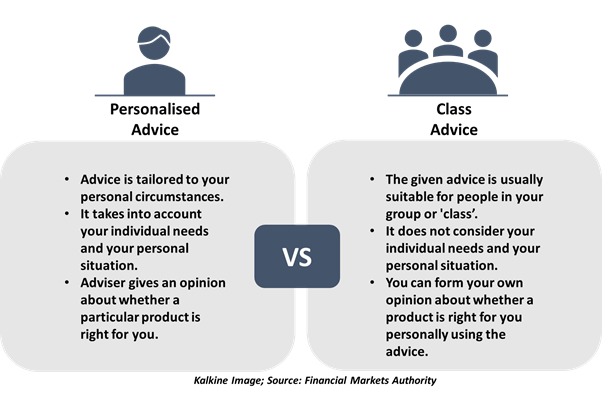

In Kiwi Land, financial advisers offer two different types of advice – Personalised Advice and Class Advice. It is important to be cognizant of the distinction between these two categories, before you engage a financial adviser.

NZ government agency, FMA defines personalised advice as the advice tailored to your personal requirements. In case of personalised advice, the financial adviser can help you evaluate whether to invest in a specific product and whether that product is suitable for you or not, as per your return expectations and risk profile.

While receiving personalised advice, you can expect that your adviser has taken your personal goals and situation into consideration. Your financial adviser will provide you an opinion about whether a specific product is appropriate for you and then you can make your investment action plan basis their suggestions.

On the other hand, FMA describes a piece of financial advice as class advice where the financial adviser will be able to advise you about what is generally suitable for people in your ‘class’ or group. In contrary to personalised advice, the class advice does not take into consideration your personal situation and individual needs.

In case of a class advice, you can utilise the generic advice from the adviser to create your own opinion about whether a specific product is right for you personally or not.

Who can Provide Class Service to Retail Clients?

As per the Financial Advisers Act 2008, the following persons are only permitted to provide a class service to a retail client:

- an authorised financial adviser

- a registered person (whether an entity or an individual)

- Qualifying Financial Entity (QFE) adviser

- an exempt provider (whether an entity or an individual), other than an overseas financial adviser

Here, exempt provider means a person who is not ordinarily resident in NZ (within the meaning of section 4 of the Crimes Act 1961) and does not have a place of business in NZ. Besides, a person is considered as an exempt provider when no financial adviser services provided by the person are received by retail clients in NZ.

It is important to note that the Financial Advisers Act 2008 does not permit a person to provide a class service that is a discretionary investment management service. Besides, persons may be licensed as DIMS licensees or services may be exempted (Part 6 of the Financial Markets Conduct Act 2013).

Are there any Regulatory-Specific Conduct Obligations While Offering Class Services to Retail Clients?

The Financial Advisers Act 2008 requires a financial adviser, when providing a class service to a retail client, to comply to one or more of the following requirements that apply under the regulations (if any):

- ensure that the prescribed warning is given in the prescribed manner that the class service is not personalised

- ensure compliance with the prescribed requirements relating to the competency of, or the use of adequate care, diligence, and skill by, the persons involved in providing the service (for example, a requirement to obtain a certificate from the principal officers of the adviser or a requirement to obtain the approval of financial advice by an authorised financial adviser or individual registered financial adviser)

- comply with any prescribed record-keeping or procedural requirements relating to those matters

Remember, class advice is a general advice and does not consider your individual investment financial situation, objectives, or needs. You should therefore analyse whether the advice is appropriate to your investment requirements before acting upon it. You may seek further advice from a stockbroker or other financial professional as necessary before acting on any such advice.