India’s digital payments revolution runs on infrastructure built and managed by a single entity — the National Payments Corporation of India. What that means for consumers when things go wrong is less understood than it should be.

The National Payments Corporation of India (NPCI) is the organisation that owns and operates the Unified Payments Interface, better known as UPI. Every UPI transaction made in India whether on PhonePe, Google Pay, Bajaj Pay UPI, BHIM, or a bank’s own app passes through NPCI’s switching infrastructure. As of early 2025, UPI processes approximately 14 billion transactions every month, making it one of the highest-volume real-time payment systems in the world. India’s digital payments ecosystem is, in a meaningful sense, a single-infrastructure system.

For consumers who use UPI for everyday payments, understanding what happens when that infrastructure fails — and what rights apply — is more practical than it might seem. One option for recurring bill payments that runs through a parallel, regulated settlement rail is Bajaj Pay, BBPS-powered service on Bajaj Finance online platforms, which processes payments through the Bharat Bill Payment System — a separate NPCI-governed framework with its own settlement and dispute resolution layer.

What NPCI is and what it controls

NPCI is a not-for-profit organisation set up in 2008 under the guidance of the Reserve Bank of India and the Indian Banks’ Association. It operates not just UPI but also IMPS (Immediate Payment Service), NACH (National Automated Clearing House), RuPay, FASTag’s NETC network, and BBPS. The organisation is, in effect, the backbone of India’s retail payment infrastructure.

UPI itself is a protocol — a set of rules and technical standards that banks and payment apps follow to move money instantly between accounts. NPCI owns the protocol and operates the central switching system that routes transactions. When you send Rs. 500 via a UPI app, the app communicates with your bank, which communicates with NPCI’s switch, which routes to the recipient’s bank, which credits the account. Every step in that chain depends on NPCI’s infrastructure being available.

The concentration problem

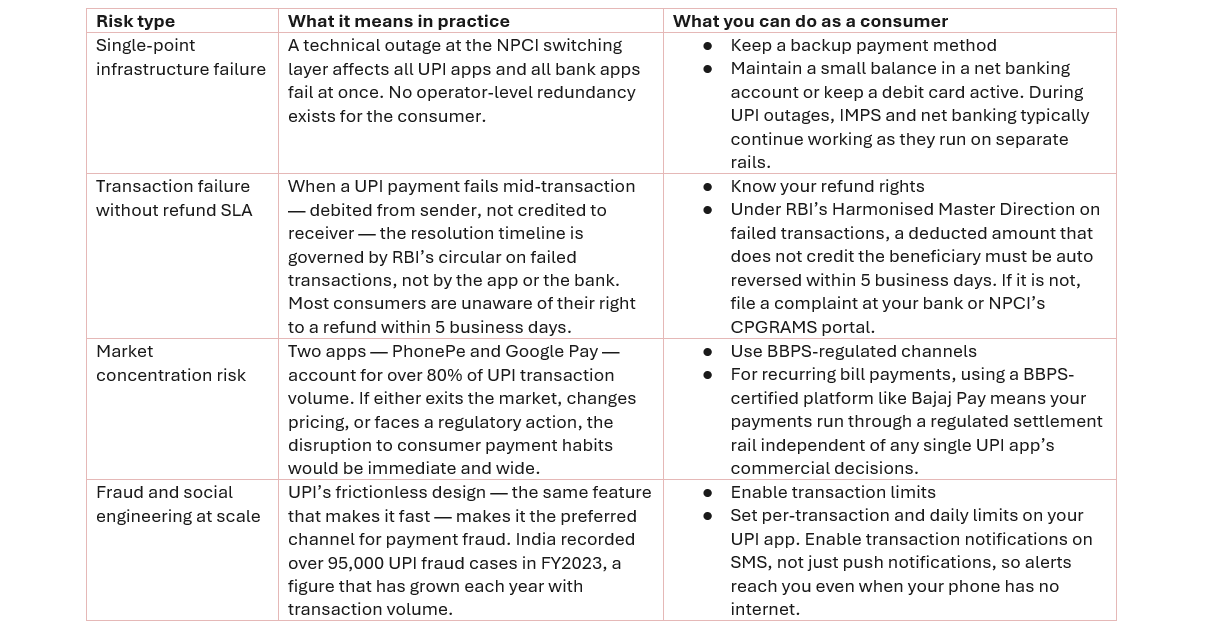

The scale of UPI is its most cited achievement — and the source of its most significant structural risk. When a payment system of this size runs through a single switching infrastructure, any disruption at that layer cascades across all participants simultaneously. A UPI outage does not affect one bank or one app. It affects all of them at once.

This has happened. NPCI’s UPI infrastructure has experienced outages that rendered all major UPI apps simultaneously unavailable — including the April 2024 outage that affected transactions for several hours during peak usage. At 14 billion transactions a month, even a two-hour outage at peak time represents hundreds of millions of failed or delayed transactions. The systemic risk is not theoretical.

What this means for consumers right now

Most consumers who use UPI daily have never thought about what happens when something goes wrong at the infrastructure level rather than the app level. Here are the four risks worth knowing — and what you can actually do about each one:

UPI transaction volumes and fraud data are published periodically by NPCI at npci.org.in. RBI’s framework on failed transaction refunds is subject to revision.

Your rights when a UPI transaction fails

A failed UPI transaction — where money leaves your account but does not reach the recipient — is one of the most common consumer complaints in digital payments. The RBI has a specific framework governing this. If the deducted amount is not auto-reversed within the stated timeline, you have a clear escalation path.

- Check your bank statement within 24 hours of a failed transaction. The reversal should appear automatically within 5 business days under RBI’s guidelines on UPI failed transactions.

- If the reversal does not appear within 5 business days, raise a complaint with your bank first. Every bank has a designated grievance officer for payment disputes.

- If the bank does not resolve within 30 days, file a complaint at the RBI’s Banking Ombudsman portal at rbi.org.in or through the Centralised Public Grievance Redress and Monitoring System at pgportal.gov.in.

- Keep your transaction reference number (UPI Transaction ID) from the payment confirmation screen. This is the primary identifier in any dispute.

How BBPS fits into a more resilient payment habit

For bill payments specifically — electricity, mobile recharge, FASTag, broadband — using a BBPS-certified platform adds a layer of settlement certainty that pure UPI payments do not provide. BBPS, the Bharat Bill Payment System, is a separate framework also governed by NPCI but with its own settlement cycle, dispute resolution process, and biller registration requirements. A payment made through a BBPS-certified platform has a documented settlement trail regardless of which payment method — UPI, card, or net banking — was used to fund it.

Bajaj Finance’s NPCI payment systems-regulated Bajaj Pay platform operates under the BBPS framework for bill payments. Every transaction generates a timestamped receipt tied to the BBPS settlement record — which means if a biller claims non-payment, the receipt is verifiable against the clearing house record, not just a screenshot from an app. For consumers making regular utility payments, this is a practical difference when a dispute arises.

The scale that makes UPI impressive is the same scale that makes its concentration a genuine risk. Knowing what that risk looks like from a consumer’s seat — and what steps provide some resilience against it — is the most useful thing to take from the conversation about India’s payments infrastructure.

The content has been authored in collaboration with our guest contributor, Sharat K.