A business loan can help you fund growth without disturbing your daily cash flow. You can use it for working capital, stock purchase, machinery, expansion, renovation, vendor payments, or business digitisation. The right funding option should match your business need, repayment capacity, and the time it will take for that investment to generate returns. Lenders like Bajaj Finance simplify borrowing by offering high-value business loans without collateral.

Read on to understand how a business loan works and how it can support your business needs.

How a Business Loan Helps Your Growing Business

Business growth usually needs upfront investment before returns begin. You may need to buy more stock before a high-demand season, upgrade old machinery, open a larger workspace, or invest in better systems. Timely funding can help you act when the opportunity is available.

A business loan gives you access to funds without using your entire cash reserve. You can repay the borrowed amount across a fixed tenure while keeping money available for salaries, rent, supplier payments, and daily operations.

For example, if you need Rs. 8 lakh to buy inventory and expect sales over the next six months, a business loan lets you purchase stock now and repay in planned instalments.

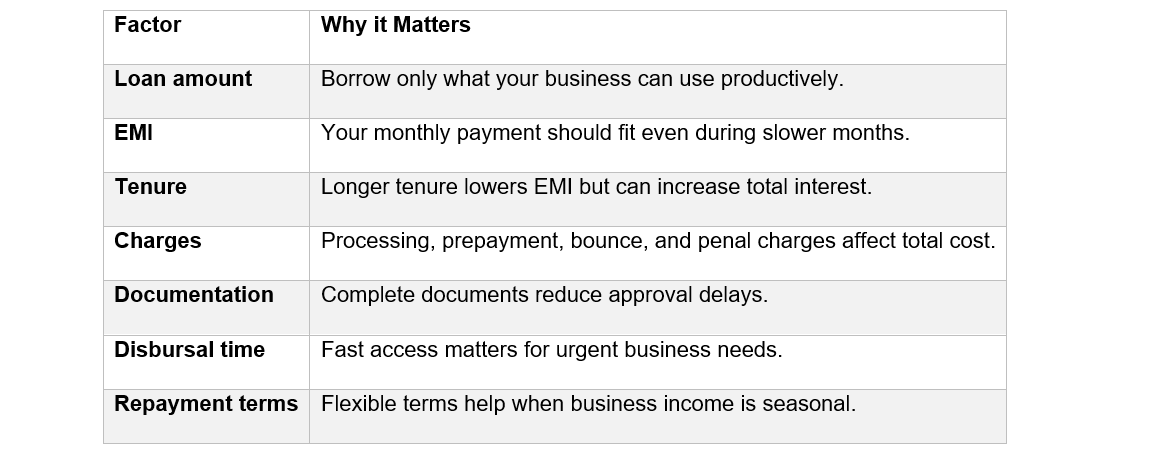

Things to Keep in Mind Before Choosing a Business Loan

Before applying for a business loan, look beyond the loan amount. A larger loan can support bigger plans, but it also increases your EMI and total interest cost.

A practical rule is to link the loan tenure to the business purpose. Short-term stock needs should not stretch into very long repayment plans. Larger investments such as machinery or expansion can justify a longer tenure because they support the business over time.

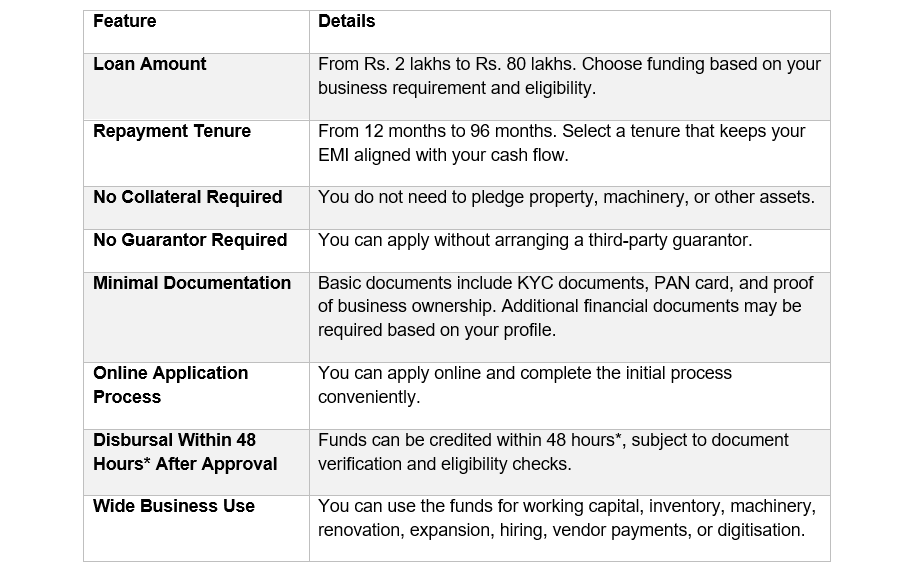

Bajaj Finance Business Loan Features

A Bajaj Finance Business Loan is built for business owners who need structured funding for operations and growth. As per the official Bajaj Finance Business Loan page, key features include:

These features make the loan suitable when you need timely access to funds without blocking business or personal assets.

What Is Mudra Loan and When Should You Consider It?

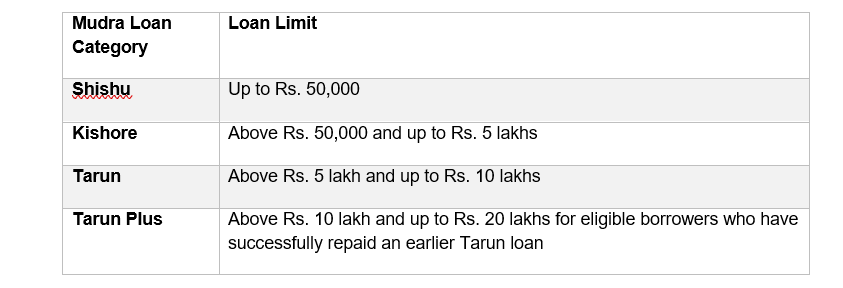

Apart from regular business loans, there are government initiatives such as Mudra Loan that support small businesses. Mudra Loan is offered under the Pradhan Mantri Mudra Yojana. It is meant for non-corporate, non-farm micro enterprises that need funds for business activities. These loans are extended through commercial banks, regional rural banks, cooperative banks, microfinance institutions, and NBFCs registered under the scheme.

Mudra Loans are categorised based on the loan amount:

You can consider Mudra Loan if your business is small, your funding need fits these limits, and you meet the scheme rules. For higher funding needs, wider usage, or faster online processing, a regular business loan may be more suitable.

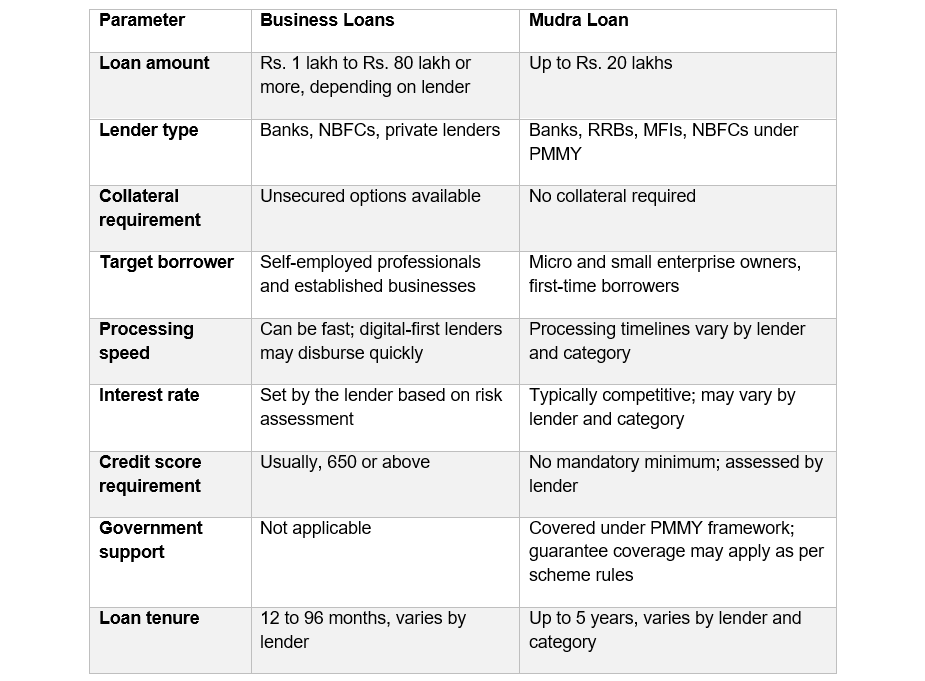

Business Loan vs Mudra Loan: A Detailed Comparison

If you need higher funding, faster processing, and broader usage, a business loan may suit you better. If you run a micro enterprise and need smaller scheme-based funding, Mudra Loan can be considered.

When Is a Conventional Business Loan the Better Choice?

A conventional business loan can be a better fit when your funding need is larger, time-sensitive, or linked to growth plans that need flexible usage.

You can consider it when:

- You need more than Rs. 20 lakh in funding, which is the upper limit for Mudra Loan.

- You require quicker disbursal and a fully digital process.

- Your business is established, with a clear financial track record and a healthy credit score.

- You need a longer repayment tenure to keep monthly EMIs manageable.

- You want flexibility in how you use the funds, without sector-specific restrictions.

When Is a Mudra Loan the Better Choice?

Mudra Loan can be useful when your business is at a micro scale and your funding requirement fits the PMMY limits.

You can consider it when:

- You are a first-time borrower or running a micro-scale business in its early stages.

- You need a smaller funding amount, typically under Rs. 20 lakh.

- You do not have an established credit history or CIBIL Score.

- You are engaged in activities eligible under PMMY, such as manufacturing, trading, or service businesses in the informal sector.

- You want to explore government credit guarantee coverage under eligible schemes.

How to Plan Your Business Loan

Start with the business decision, then choose the loan. This keeps borrowing disciplined.

- Define the purpose: Write down the exact use, such as stock, machinery, renovation, or working capital.

- Estimate the amount: Add the main cost and a small buffer. Avoid borrowing extra without a clear use.

- Check monthly surplus: Calculate how much money remains after rent, salaries, supplier payments, taxes, and personal withdrawals.

- Choose the tenure: Pick a tenure that keeps EMI comfortable without stretching repayment unnecessarily.

- Review charges: Check processing fees, prepayment charges, penal charges, and other costs.

- Compare funding options: If your need fits a micro-enterprise scheme, check Mudra Loan eligibility. If you need a higher amount, faster access, or broader flexibility, compare business loan features.

- Prepare documents: Keep KYC, PAN, business proof, and financial papers ready.

- Read the loan terms: Understand repayment dates, EMI amount, charges, and closure rules before accepting the loan.

A business loan should support growth without putting pressure on daily operations. Choose your funding option based on the purpose, amount required, repayment capacity, tenure, charges, and speed of disbursal. Bajaj Finance Business Loan offers Rs. 2 lakh to Rs. 80 lakh, repayment tenure from 12 months to 96 months, no collateral requirement, minimal documentation, and a hassle-free application process. Government initiatives such as Mudra Loan can support eligible micro enterprises, but your final choice should depend on what your business can use well and repay comfortably.

The content has been authored in collaboration with our guest contributor, Abdul Kadir.