Growth will bankrupt you faster than failure.

An older shop owner said that to me once, standing in front of a humming production line that looked, from a distance, like success. Orders everywhere. Staffrushing. Bank account gasping.

Ifyourein that strange place more demand than money, more opportunity thanapprovals you already know what he meant.Letstalk about how you keep scaling when the bankdoesntfeel like a partner, just a gate.

GrowthDoesntWait for Perfect Credit

Badcreditsnever part of the business plan.

Yet one tough season, a global scare, ormaybe justa client who ghosted on payment, and suddenlyyouregetting no more than yes at every bank.

Numbersback itup.

A 2019 Intuit QuickBooks studyfound that 61% of small businesses struggle with cash flow, and 32%cantpay themselves, vendors, or employees on time at least once a year. That stat feels different whenyourethe one hovering over your banking app on payroll day.

Growth still happens, thoughclientsdontcare about your loan rejections. They need their stuff.Somoney patchwork begins.

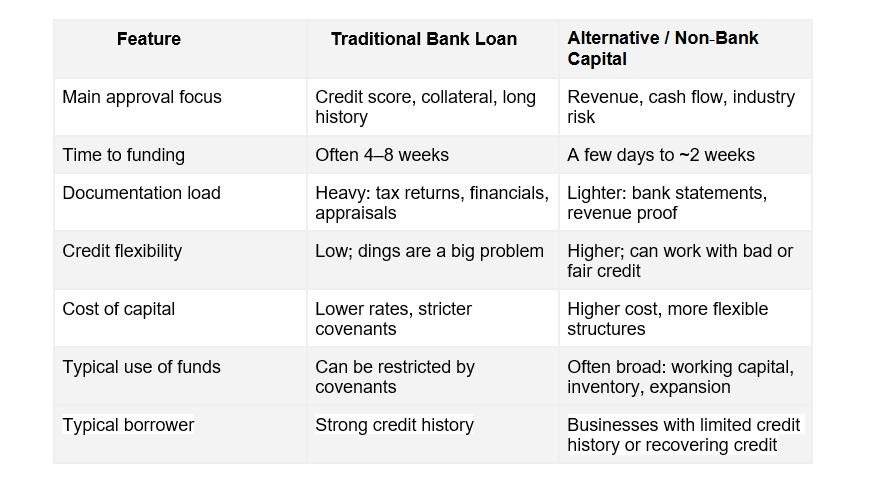

Traditional Loans vs. Alternative Capital: A Quick Snapshot

Once the bank says no (or maybe later), the question stops being Whats the cheapest rate? and becomes Whats actually available, soon, without blowing a hole in my future?

To keep it grounded,hereshow the main routes usually compare:

Then again, expensive but real capital can be safer than cheap but imaginary funding that never lands. The power move is knowing whichoptionyour business can carry without snapping.

Rethinking Capital: What You Can Do Without a Traditional Loan

Once you stop waiting for the perfect bank relationship, you start noticing other doors. Some are rough around the edges. Some are surprisinglyreasonable,if you understand whatyouresigning.

Many nonbank lenders lean more on your actual performance monthly revenue, card sales, time in business than a single credit score.

Many alternative lenders now offer financing designed for businesses that may not qualify for conventional bank loans, using current revenue, cash flow, and operating performance alongside traditional risk factors. Crestmont Capital funding options, for example, include bad-credit business loans, working-capital financing, and equipment funding that can help eligible businesses access capital when traditional lending isn't the right fit.

With such a model, owners turned down by banks stillhave a shot atcovering payroll, inventory, or expansion. That said, you still need a plan.

Two broad paths usually pop up first once the bank window closes.

Option 1: Revenue-Based and Cash-Flow Financing

Thisisnta magic solution, but for anyone processing constant salesthink retail, cafs, fast e-commerceit can keep you alive. You borrow, and a percentage of your sales pays it back.Busyweekseat the balance. Slow weeks offer relief.

It sounds easy, but cash flowisntalways kind. ACB Insights report found 70% of failed startups collapsed due to cash burn or not getting new funds. Give up too much of your daily revenue, andyoullbecome one of them. Always run the worst week numbers, not just the best.

Option 2: Collateral You Forgot You Had

Still, many owners underestimate the value of whats already in the building.

Unpaid invoices, equipment, eveninventory can be turned into shortterm cash through assetbased lending or invoice financing.

A2025 Atradius reportshowed thatnearly 40%of B2B invoices in North America were overdue at any given time. You can almost hear those dollars stuck in limbo. Some lenders will advance aportionof those receivables, then get repaid when your customers finally wire the money.

A Strong Story Matters to Lenders

Numbers crack the lock, butstoryopens the door.

Even alternative lenders want the contextwhy last year tanked, what you changed since, and how this moneys not just doubling down on a failed plan. Show your scars, not your slogans. Many lenders also evaluate recent business performance, cash flow trends, and operational improvements alongside an applicant's explanation, allowing businesses todemonstratetheir current financial position rather than relying solely on past credit history.

A few things that persuade:

- Admitting what went wrongwithout excuses.

- Explaining revenue spikes or dips.

- Showing real expense cuts or operational changes.

- Mapping how todays funding becomes tomorrows cash, not just hope.

Think of it as pitching your learning curve.Theyllsee through fakeswhat they want is someonestubborn, butawake.

Final Thoughts: Let Growth Be Imperfect, Not Reckless

Growth funded by scavenged capital is chaoticmaybe evenugly.

It can also make you unbreakable. If you keep your numbers close, treat every loan as temporary scaffolding, and say no to deals that drain your cash, you can build something real. Choosing financing that matches your business's cash flow, repayment capacity, and growthobjectivescan help create a more sustainable path forward, even when traditional financingisn'tavailable. Unpolished, maybebutyours. And sometimes, that resilience is the best kind of strategy.

The content has been authored in collaboration with our guest contributor, James Williams.