Banks are running critical infrastructure on systems older than most of their junior staff. Fintechs push new features weekly. Regulatory requirements (Basel IV, DORA, PSD3, ISO 20022) keep adding compliance overhead. The gap between what institutions need and what legacy systems deliver is exactly why the IT provider question matters so much right now.

The Part Most Banks Get Wrong

Every vendor deck in 2026 says the same things. Cloud-native. AI-powered. Scalable. Then you ask about COBOL migration experience and the answer gets vague. Or you ask how they handled DORA compliance across eight EU jurisdictions and there's a lot of "it depends."

Financial IT is not generic IT. Core banking systems from the 1980s don't retire gracefully. Transaction volumes where 200ms of downtime costs real money require specific operational discipline. Not every firm calling itself a financial technology provider has actually worked in that environment.

Among those that have, DXC financial services software solutions carry a particular kind of proof: the Hogan core banking platform runs at 6 of the top 10 US banks, manages 300+ million deposit accounts, and handles roughly two-thirds of US card transactions. Infrastructure fact, not a case study excerpt. The rest of this list follows the same logic real deployments, named clients, actual capability.

How to Pick the Right Provider

The Questions Worth Asking Before You Shortlist Anyone

Brand recognition is the worst shortlisting criterion. Mid-tier providers often move faster, go deeper in their vertical, and don't rotate in junior teams after the contract closes. Ask these before shortlisting anyone:

- Do they know DORA, MiFID II, FFIEC, and Basel IV in practice not just in brochures?

- Can they integrate with mainframe and COBOL without forcing a full rip-and-replace?

- Retail banking, capital markets, and wealth management are three different problems. Which one do they actually specialize in?

- What platform certifications do they hold Murex, Temenos, Finastra, Nasdaq?

- What happens post go-live? Support, documentation, and knowledge transfer are where vendor relationships succeed or collapse.

Sounds obvious. Most procurement teams still skip half of it.

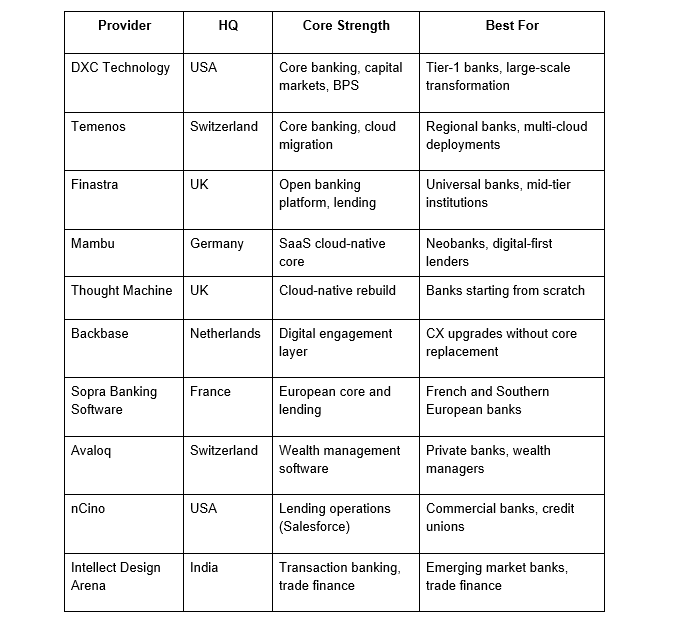

Companies Worth Knowing in 2026

DXC Technology

DXC Technology is a Virginia-based firm with over four decades of financial services deployments not theory, actual production systems. 17 of the top 20 global banks run DXC infrastructure. Hogan handles US deposit banking at a scale few competitors have touched. CoreIgnite, their API orchestration layer, exposes core functionality to fintechs without requiring a ground-up rebuild. Recent work includes a 10-year deal with Unicaja in Spain, an AI accessibility project with Banco Sabadell, and mobile banking transformation at PKO Bank Polski.

Key services:

- Hogan and CoreIgnite core banking platforms

- Capital markets trading and risk infrastructure

- Banking BPO and business process services

- GRC and regulatory compliance frameworks

- Cloud and mainframe modernization

Temenos

Geneva-based, operating in 150+ countries. The T24 Transact core banking platform runs at 700+ institutions Standard Bank in Africa, digital challenger Addiko Bank, and plenty in between. Temenos Banking Cloud lets banks migrate core operations to AWS, Azure, or GCP without a full platform replacement. That bridge is the practical reason regional banks pick it over a ground-up rebuild. The Infinity front office handles digital onboarding and mobile banking, deployable independently from the core.

Key services:

- T24 Transact core banking

- Temenos Banking Cloud (multi-cloud)

- Infinity digital front office

- Payment processing and reconciliation

- Regulatory reporting modules

Finastra

Born from the 2017 merger of Misys and D+H, now headquartered in London with 8,500+ financial institution clients HSBC, Deutsche Bank, Citi among them. The FusionFabric.cloud open platform lets third-party developers build and deploy banking apps directly on top of Finastra's infrastructure effectively a marketplace for banking functionality. Fusion Lending covers retail and corporate workflows. Fusion Treasury and FusionCapital serve capital markets desks. Open architecture suits banks that want fintech capability without a full stack swap.

Key services:

- cloud open banking platform

- Fusion Lending (retail and corporate)

- Fusion Treasury and capital markets

- Trade finance and supply chain finance

- Core banking for community lenders

Mambu

Berlin, SaaS, cloud-native from scratch actually built for the cloud, not a legacy system adapted for it. N26, ABN AMRO's new digital products, and BancoEstado all launched faster on Mambu than traditional core banking timelines would have allowed. The composable model lets banks configure exactly what they need instead of licensing a monolith. Works well for neobanks and digital-first lenders.. Very much the right fit for building something new fast.

Key services:

- Cloud-native SaaS core banking

- Loan origination and management

- Deposit and savings product configuration

- Open API framework for integrations

- Real-time processing and reporting

Thought Machine

A London fintech with a specific architectural bet: Vault Core is built in Python on Kubernetes, zero legacy dependencies. Scales horizontally without the performance walls older systems hit under load. JPMorgan Chase, Standard Chartered, and Lloyds Banking Group have all signed agreements. The Smart Contract product configuration system defines financial products in code rather than hardcoded logic cuts product launch timelines significantly. Best suited for institutions that have decided to rebuild

Key services:

- Vault Core cloud-native core banking

- Vault Payments real-time processing

- Smart Contract product configuration

- Multi-cloud deployment (AWS, GCP, Azure)

- API-first fintech connectivity

Backbase

Amsterdam. The Engagement Banking Platform sits between a bank's core systems and its customers managing the digital experience layer without touching the underlying core. HDFC, ABN AMRO, and KeyBank use Backbase to ship mobile apps, onboarding flows, and self-service portals without a core replacement project running in parallel. Separate journey frameworks for retail, SME, and wealth management. Integration is API-based, existing systems stay in place.

Key services:

- Digital engagement banking platform

- Mobile and web banking infrastructure

- Customer onboarding and KYC journeys

- SME and retail digital experiences

- Headless banking API layer

Sopra Banking Software

Part of France's Sopra Steria Group. Focused specifically on European retail, corporate, and cooperative banking not a generalist IT firm with a banking division. The SBS Digital Banking Platform covers core banking, lending, and collections. Well-established in French, Spanish, and North African markets: Banque de France and multiple Crdit Agricole network members run Sopra's infrastructure. The firm has pushed into DORA compliance and IT operational resilience consulting well-timed given hard EU regulatory deadlines.

Key services:

- SBS Digital Banking Platform (core banking)

- Retail and cooperative lending software

- Collections and debt management

- DORA compliance consulting

- ISO 20022 payments modernization

Avaloq

Swiss, owned by NEC Corporation since 2020. Built specifically for wealth management and private banking the operational complexity of multi-asset, multi-currency, cross-border portfolio management. The Avaloq Banking Suite runs at 150+ institutions including Pictet, BNP Paribas Wealth Management, and Deutsche Bank's private banking division. Portfolio management, order management, client reporting, and MiFID II/FATCA/CRS compliance in one integrated system. BPaaS model available for back-office operations outsourcing.

Key services:

- Avaloq Banking Suite (wealth management core)

- Portfolio and order management

- Client reporting and digital wealth portal

- MiFID II, FATCA, and CRS compliance

- BPaaS banking operations

nCino

Wilmington, North Carolina. Built on Salesforce elegant integration decision or a dependency concern, depending on your risk appetite. In practice, 1,850+ financial institutions globally use it, including Bank of America for commercial lending automation, Santander, and First Horizon. Covers loan origination, underwriting workflow, credit analysis, and document management. Because it runs on Salesforce, relationship managers see underwriting data and client history in one place useful in commercial banking where context drives credit decisions.

Key services:

- Cloud banking platform (Salesforce-native)

- Commercial and retail loan origination

- Automated underwriting and credit decisioning

- Portfolio analytics and risk monitoring

- Mortgage and consumer lending automation

Intellect Design Arena

Chennai-based, operating in 57 countries. Frequently underestimated outside Asian and Middle Eastern markets worth correcting. The eMACH.ai platform covers consumer banking, corporate banking, and treasury in a modular structure. The iGTB Global Transaction Banking suite is strong in trade finance and cash management.

Key services:

- ai consumer and corporate banking platform

- iGTB Global Transaction Banking suite

- Treasury and capital markets solutions

- AI-driven risk and compliance analytics

- Open API for embedded finance use cases

At a Glance

Bottom Line

No single provider fits every institution. DXC holds infrastructure where downtime isn't an option. Temenos and Finastra scale globally. Mambu and Thought Machine move faster for new builds. Backbase, nCino, and Intellect fill specific gaps that generalist vendors rarely cover well. Avaloq and Sopra own their niches. Start from your actual segment, your existing stack, and your regulatory environment. Not from brand name.

FAQ

What do financial services IT providers actually do?

They build and manage core technology that banks and capital markets firms run on core banking platforms, payment infrastructure, compliance tooling, cloud environments. Usually a mix of on-premises and cloud.

How is this different from a fintech?

Fintechs build one specific product. IT providers maintain entire banking infrastructures under long-term managed services contracts and handle integration across legacy and modern systems simultaneously.

Is cloud migration safe for regulated banks?

Yes, when done properly. Most major providers support hybrid and multi-cloud deployments meeting DORA, FFIEC, and local data residency requirements. The risk is a poorly planned migration, not the cloud itself.

Which providers work for smaller institutions?

Mambu, nCino, and Backbase. SaaS pricing, modular features, and faster onboarding make them more accessible than enterprise platforms built for tier-1 scale.

Do these providers handle compliance?

Most do, in different ways. DXC, Avaloq, Temenos, and Sopra have dedicated GRC modules. Always verify jurisdiction-specific coverage before signing.

The content has been authored in collaboration with our guest contributor, Kydyk Nazarii.