Summary

- Banks may witness a trigger in defaults and fall in mortgage lending amid a sluggish economy.

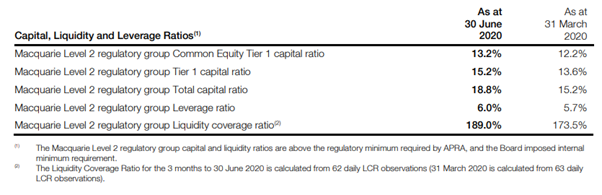

- Macquarie Bank level 2 regulatory group CET1 capital ratio stood at 13.2% on 30 June 2020 compared to 12.2% on 31 March 2020.

- Macquarie Group’s capital surplus stood at $8.1 billion as on 30 June, up from $7.1 billion on 31 March 2020, exceeding APRA Basel 3 regulatory obligations.

- Commonwealth Bank’s NPAT dipped 11.3% on pcp to $7.3 billion in FY20 ended 30 June due to steep rise in loan impairment expenses in response to credit quality concerns amid COVID-19.

As Australia recovers from after-effects of lockdown imposed to control COVID-19 spread, high unemployment can harm household finances and cause defaults as the economy witnesses the greatest slump since the 1930s. As government subsidies end and a moratorium on loan repayments are lifted, loan defaults are expected to rise considerably stressing the banks amid a slowing economy.

DO READ: Banking Stocks under Spotlight – Is there Any Scope of Bounce Back?

The risky atmosphere is expected to result in a more cautious behaviour of banks in lending out money, making it tougher for borrowers to borrow.

Let’s have a look at how these 2 ASX200 listed banking stocks have been performing.

Macquarie Bank Limited (MBL) is an authorised deposit-taking institution (ADI) regulated by APRA and offers trading, advisory, funds management, assets financing and research and retail financial services. MBL is a subsidiary company of Macquarie Group Limited (ASX:MGL).

APRA published a draft standard on the leverage ratio inclusive of minimum leverage ratio condition of 3.5% for IRB banks during November last year.

While the deadline for the implementation of Basel III standards has been postponed to 1 January 2023, Macquarie Group’s financial position comfortably exceeds the Australian Prudential Regulation Authority’s (APRA) Basel III regulatory requirements.

As at 30 June 2020:

- Group capital surplus was at $8.1 billion, up from $7.1 billion at 31 March 2020;

- The Bank Group APRA Basel III Common Equity Tier 1 capital ratio stood at 13.2%, up from 12.2% at 31 March 2020; and

- The Bank Group’s APRA leverage ratio was 6%, LCR was 189%, and NSFR stood at 118%.

Basel II capital adequacy framework was reformed in January 2013, and the Basel III framework was implemented by APRA. In few areas, APRA went a step ahead by unveiling even stricter requirements.

Macquarie Bank Pillar III disclosure report dated 20 August provided disclosure details as required by APRA Prudential Standard APS 330: Public Disclosure.

Macquarie Bank provided details of various sections like capital adequacy, credit risk measurement, securitisation, leverage ratio disclosures and liquidity coverage ratio disclosures.

Source: MBL June Pillar 3 Disclosure, dated 20 August

On 30 July, Macquarie Group provided an update on the first quarter of its 2021 financial year (1Q21) before its 2020 Annual General Meeting (AGM).

The CEO of the Group, Shemara Wikramanayake, stated that Macquarie’s operating groups were affected by mixed trading conditions with their contribution in 1Q21 slightly down on 1Q20.

Q1 Business Highlights

The following highlights were observed for the Group’s first quarter of FY21 ended 30 June:

- Macquarie Asset Management (MAM) had $568 billion in assets under management as at 30 June 2020, down 5% on 31 March 2020, majorly led by foreign exchange movements, and partially offset by market appreciation in Macquarie Investment Management (MIM) assets.

- Banking and Financial Services (BFS) total deposits were at $69 billion at 30 June 2020, up 8% on 31 March 2020, and the quarter also consisted of continued provisioning with 13% of BFS clients accessing assistance at 30 June 2020.

- Macquarie Capital’s fee revenue dropped in 1Q20 because of lower Mergers & Acquisitions and Debt Capital Markets fee revenue, partially balanced by higher Equity Capital Markets (ECM) activity, and good Equity Platform results.

- Commodities and Capital Markets (CGM) gained from growing demand as consumers tried to rebalance their holdings in a competitive market to mitigate the risk.

Though the Macquarie Group did not provide any FY21 guidance, conditions are likely to remain challenging due to COVID-19 uncertainty. The length and extent of the pandemic, global levels of government support, the completion rate of transactions, impact of foreign exchange, regulatory changes and tax uncertainties are some of the factors that are predicted to influence the short-term outlook.

However, Macquarie is well placed to give superior performance in the medium-term because its robust balance sheet, proven risk management and the ability to adapt to its portfolio mix to changing market conditions.

Macquarie Group last traded on ASX, at a price of $127.73, up by 0.235% from its last close.

Commonwealth Bank of Australia

One of the leading financial services provider across the nation, Commonwealth Bank of Australia (ASX: CBA) share price fell by 0.977% to settle at $68.95 on 24 August. The entity has operations in New Zealand, Europe, North America, and Asia regions as well.

On 21 August, Commonwealth Bank acknowledged another class action against Commonwealth Financial Planning Limited (CFPL) and Financial Wisdom Limited (FWL) in reference to certain CommInsure life insurance policies recommended by financial advisers appointed by CFPL and FWL. The proceedings that were filed by Shine Lawyers in the Federal Court of Australia have also been brought against The Colonial Mutual Life Assurance Society Limited.

ALSO READ: CBA profit down 11%, but is it bad?

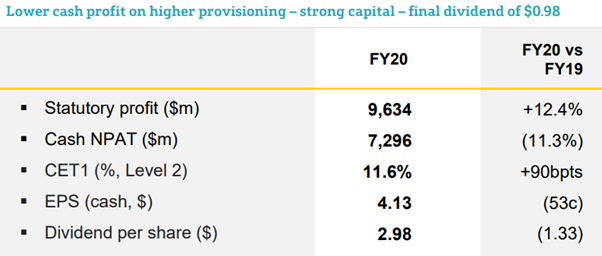

Further, Commonwealth Bank’s cash net profit after tax (NPAT) plunged 11.3% for FY20 year on year to $7.29 billion due to the impact of COVID-19 and rise in loan impairment costs.

Some of the highlights of FY2020 ended 30 June consists of the following:

- Statutory NPAT rose due to gains on sale from divestments, up 12.4% to $9.63 billion

- Loan impairment expenses stood at $2,518 million, an increase of $1,317 million inclusive of the $1.5 billion COVID-19 provision

- Common Equity Tier 1 (CET1) capital ratio of 11.6% (Level 2, APRA), up 90 bpts and net interest margin was at 2.07%, down 2 bpts because of lower interest rates

- The fully frank final dividend of 98 cents per share was declared (adding to an interim payment of $2 per share). The final dividend is due to be paid by 30 September.

Source: CBA 2020 Presentation, dated 12 August 2020

As at 30 June 2020, the Group’s Basel III Common Equity Tier 1 (CET1), Tier 1 and Total Capital ratios as measured on an APRA basis were 11.6%, 13.9% and 17.5% respectively and 17.4% on an internationally comparable basis.

The Group’s leverage ratio, defined as Tier 1 Capital as a percentage of total exposures, stood at 5.9% at 30 June 2020 on an APRA basis and 6.7% on an internationally comparable basis. The Group maintained an average Liquidity Coverage Ratio of 155% in June 2020 quarter and a spot LCR of 145% as at 30 June 2020.

CBA Chief Executive Officer Matt Comyn stated that the power of its core banking business merged with solid operational performance had posted good results for its customers and shareholders despite lower interest rate challenges and COVID-19. The Group continues to strengthen its balance sheet across key capital, funding, and liquidity metrics, as well as extend its digital leadership through increased customer engagement.