_07_03_2026_03_50_21_133108.jpg)

Summary

- In July 2019, the French Parliament had passed Digital Services Tax (DST) regime to impose a 3 percent tax on the revenue of the US digital services providers, which resulted in an investigation by the US to determine whether France was unfairly targeting the tax on the US tech companies.

- With grim inevitability, the investigation concluded that French DST was discriminatory and imposed undue burden on the US companies, calling for retaliation, with proposed tariffs on French products such as wine, make-up, handbags, and cheese.

- Of late, the US unveiled its plans to impose 25% on French imports over its DST but has delayed the action for until next 180 days.

- The US has started investigating DST implemented or deemed by several nations including Austria, Spain, Brazil, the UK, the European Union, Indonesia, India, and many more under section 301 of the Trade Act, 1974.

On 10 July 2020, the US announced plans to impose 25 per cent tariffs on about US$1.3 billion (estimated trade value for CY2019) worth of French imports in response to the France's DST (Digital Services Tax) that impacts major US tech companies.

However, the US would hold off from implementing the move for up to 180 days, i.e. tariffs would be effective from 6 January 2021.

United States Trade Representative (USTR) said that they had delayed the start of the tariffs until January 2021 for enabling further time for bilateral and multilateral negotiations that might go ahead in the direction of agreeable solution for this matter.

As per the notice issued by USTR, products that were subject to tariffs included beauty, soaps, and handbags. These tariffs were lesser than the December proposed tariffs, in terms of the tax rate and the number of products.

The products such as sparkling wine and cheese were excluded from the latest imports facing the tariff.

Did you read; Blue-chip stocks: Value versus Growth in Covid-19 Era

Let us get back in time and get acquainted with the buzz around French Digital Services Tax:

First, let’s familiarise ourselves with the concept of French DST.

DST is built on the simple prognosis that data creates value, so taxation of the data that produces such value is different from other goods.

Why the French digital services tax came into the picture?

As per French government, there was an inconsistency between the location and way of taxing profits derived from digital activities.

Furthermore, technology entities apparently had gained huge benefits as France’s tax system laid more emphasis on the taxation of companies with brick and mortar operations.

Which digital entities were impacted?

DST was mostly concerned with those entities whose turnover from the provision of digital services surpassed €750 million at global level and €25 million at domestic level.

DST was levied at the tax rate of 3% on turnover derived from digital activities to, or aimed at, French users.

Passing of the DST regime and investigation of DST under Section 301

On 11 July 2019, a law providing for DST was approved after a final vote by the Senate of the French Parliament. Subsequently, the US initiated trade-related investigation of France’s DST on digital giants under Section 301 of the US Trade Act of 1974.

A quick fact, it was the same section that the US had used to justify tariffs on Chinese goods.

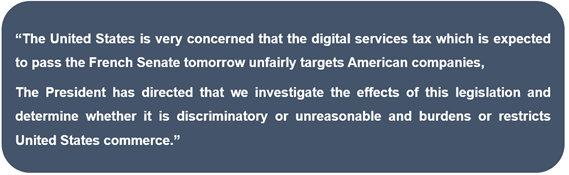

In light of the above DST regime, US Trade Representative, Robert Lighthizer said that-

Source: Notice from the USTR’s office

Did you read; Pioneering Global Technology Companies: A part and Parcel of Consumers’ Lives

USTR opened a new front in trade wars with proposed tariffs on French imports.

On 6 December 2019, USTR announced that France’s DST was discriminatory and was imposing undue burden on the US companies, and further actionable under sections 301(b) and 304 (a) of the Trade Act.

Furthermore, the USTR took action against digital tax regimes and unveiled a preliminary list of French products that could be subject to punitive duties of up to 100%, containing handbags, makeup, sparkling wine, and cheese with an approximate annual import value of US$2.4 billion.

Starting December 2019, the US and France had continued to work together on international tax rules via the Organization of Economic Cooperation and Development (OECD), an intergovernmental economic organization.

Additionally, USTR had invited public comments on the proposed trade restrictions on French services, while following further steps were taken in the investigation:

- 6 January 2020 was the deadline for written comments on the proposed action.

- 7 January 2020 was the date when a public hearing was convened under Section 301 in the US International Trade Commission office in Washington DC.

- 14 January 2020 was the deadline for the submission of post-hearing rebuttal comments.

These steps had boosted USTR’s progress expeditiously to have an effective discussion at the OECD regarding taxation of digital services.

As per various media reports, even though the US withdrew from negotiation on DST in mid-June, citing a lack of progress in negotiations amid pandemic, the OECD is determined to develop a multilateral tactic for challenges related to international tax regimes of the digital economy prior to the close of 2020.

As per the latest update, the US stated that its trade representative is investigating DST that has been embraced or being contemplated by countries like Austria, Spain, the Czech Republic, Brazil, the UK, the European Union, Indonesia, Italy, India, and Turkey under section 301 of the Trade Act, 1974.

Did you read; China’s Internet Play: Issues, Censorship and ByteDance in Action