Summary

- The banking sector drove down S&P/ASX200 index on 17 August with the Index 0.81% lower than its previous close.

- The shares of big 4 banks slid, while Bendigo and Adelaide Bank share price was down by 4.7% at $6.67 and NAB share price was down by 1.9% at $17.86.

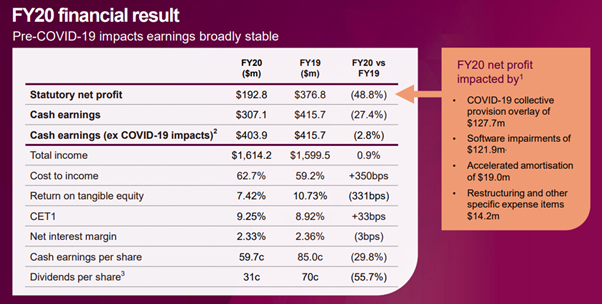

- Bendigo and Adelaide’s statutory net profits dived by 48% to $192.8 million for FY20 ending 30 June 2020 citing low-interest rates and COVID-19 as major drivers.

- NAB reported lower cash earnings, stable net interest margins and common equity Tier-1 ratio of 11.6% for FY20

The S&P/ASX 200 Index fell 0.8% at 6076.4 as the share price of banks slid. Big 4 banks were among the top drags on the benchmark index on 17 August.

The big four banks ended the trading session in red, NAB share price fell by 2.58% to $17.75, Westpac share price slipped by 2.49% to $17.6, ANZ share price dropped 2.25% to $18.26, and CBA share price was down 1.4% to $70.76.

GOOD READ: Banking Stocks under Spotlight – Is there Any Scope of Bounce Back?

Let’s have a look at Bendigo and Adelaide Bank and NAB to get a gist of the headwinds endured by the banking industry.

Bendigo and Adelaide Bank Limited

Bendigo and Adelaide Bank Limited (ASX:BEN) share price settled the day’s trading session, down by 6.571% to $6.54 on 17 August.

As mentioned in its full year report for the period ended 30 June 2020, the profits of the Bendigo and Adelaide bank nearly halved with the onset of coronavirus pandemic. The Bank’s statutory net profit was down by 48.8% compared to the financial year 2019 to $192.8 million on pcp while cash earnings after tax were down 27.4% at $301.7 million.

Some key highlights from the results are as following:

- Rise in total lending by 5.1% on pcp and above system to $65.3 billion, with solid residential lending growth of 9.4%, 3.6 times system, because of focused customer strategies.

- Net interest margin fell by 3 bps on pcp to 2.33% showing active management of pricing and volume for lending and deposits regardless of the interest rate situation.

- Common Equity Tier 1 increased by 33 basis points to 9.25%.

- Bad and doubtful debts stood at $168.5 million, substantially affected by COVID-19 provision of $127.7 million.

Source: BEN FY20 Presentation, dated 17 August 2020

The banking group deferred its final dividend amid COVID-19 impact.

Marnie Baker, Bendigo and Adelaide Bank’s Chief Executive, stated that the incurred financial damage was largely attributed to COVID-19-induced economic slowdown, which culminated in a low-interest rate setting. She added that the result for financial year 2020 had been impacted by the COVID-19 pandemic, record low interest rates and investment costs needed to aid the delivery of the Bank’s strategy. She also noted that the market conditions are expected to stay challenging due to which no guidance for FY21 will be provided.

GOOD READ: Australian Banking Space Amidst Virus-Induced Volatility; Digitalisation Turning Over a New Leaf

She asserted that the Bank witnessed rising refinancing activity as customers moved to the Bank, and Bendigo and Adelaide Bank continued to transform its services and ability to meet the demands.

Macquarie Group stated that Bendigo and Adelaide Bank results were 7% lower than its original estimates and mainly influenced by higher expenditures incurred by the Bank.

Macquarie Group also stated that the current valuation of the Bank was difficult to explain, under such challenging times of a low-interest-rate environment and higher exposure to Melbourne lockdown than peers. It also foresees further risk to dividend sustainability and has dividend cuts in its forecasts ahead.

National Australia Bank Limited

National Australia Bank Limited (ASX:NAB) share price was down by 2.58% to $17.75, as on 17 August.

NAB posted unaudited cash earnings of $1.55 billion in Q3 results for the period ended 30 June 2020, as per its trading update released on 14 August. The Bank’s results for 3Q20 were reflective of the present operating environment described by volatile markets, low interest rates, muted credit demand, declining asset quality and cost pressures.

Key metrics for FY20 Q3 show:

- Unaudited statutory net profit stood at $1.50 billion, and unaudited cash earnings were at $1.55 billion with a year-over-year fall of 7%.

- Cash earnings rose by 24%, revenue increased by 10%, and expenses increased 2% due to coronavirus related staffing concerns.

- NAB Common Equity Tier 1 capital stood at a robust 11.6% of the risk-adjusted assets after the Bank raised $4.25 billion in new equity from shareholders earlier, amid the pandemic.

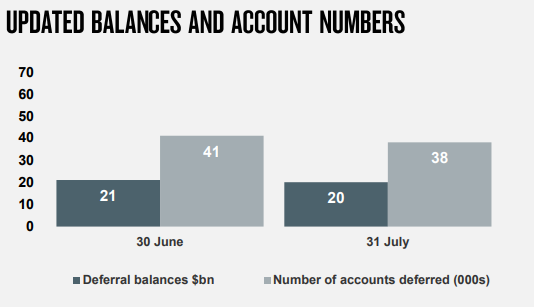

- 86,000 home loan deferrals and 38,000 business loan deferrals totalling to $55 billion by the end of June.

NAB stated that the repayment deferrals have been giving vital support to customers combined with substantial assistance from governments and regulators. However, the Bank’s credit impairment charges remain high, although down from $976 million recorded in the previous quarter to $570 million in the June quarter.

ALSO READ: Banks need A change in Operating Strategy, straight from the horse's mouth- NAB

Source: NAB’s Trading update for 3Q20, dated 14 August 2020

Ross McEwan, CEO of NAB, stated that the second wave of COVID-19 in Victoria had imposed more psychological damage than financial so far. He emphasised that the outlook is still highly uncertain, but decisive actions taken in April to bolster the balance sheet position of the Bank allows it to support customers and keep the Bank safe.

Macquarie analysts have stated that they were astonished by NAB’s move to not increase its provision for bad and doubtful debts amid COVID-19. They noticed consensus expectations around impairment charges as too positive.

Ross McEwan also stated that NAB’s repayment deferrals combined with substantial relief from government and regulators are providing vital assistance to consumers. However, Mr McEwan stated that he would not forecast the recovery number of the customers who can resume repayments after deferring loans. Recently, the Bank has contacted 24k of the 90k customers with the highest risk loans.