Summary

- Charter Hall Long WALE REIT has disclosed full-year results for the period ended 30 June 2020. Most of the gain in income of the trust was driven new acquisitions during the year, which totalled $ 1.4 billion.

- Since the trust has predominantly defensive tenants and assets, the impact due to COVID-19 was negligible to FY20 operating earnings. The trust provided 0.2% of net rent as a relief to tenants affected by store closures and lockdowns.

- During FY20, CLW further diversified portfolio, improved the quality of assets and extended its WALE.

- CLW expects operating EPS of no less than 29.1 cents per security for FY21.

Real Estate Investment Trusts (REITs) are popular for their income distribution. REITs invest in property assets leased to tenants and seek to deliver investment return through capital gains on assets and rental income.

Some REITs also engage in greenfield acquisition and development activities. REITs are managed by an investment manager, which is usually a professional entity, seeking to maximise investment return with sustainable leverage.

At the backdrop of COVID-19, REITs have also experienced deterioration in operating conditions due to shock to cashflows of tenants. Since there was no cash flowing into tenants due to lockdowns, the commentary from tenants largely reflects their negotiations with landlords or REITs.

REITs gave rental relief to their tenants, and many companies have intended to close stores while some have entered administration as well. Questions have also been raised on the sustainability of office REITs, driven by increasing remote working culture in society.

Charter Hall Long WALE REIT (ASX:CLW) Leaps after FY20 Results

As a long REIT, the trust invests in assets leased on long leases. CLW manages a portfolio comprising assets in the segments of telco exchange, industrial, logistics, retail and agri-logistics, and offices. Its tenants majorly include government and multinational corporates having small impact due to COVID-19.

Charter Hall provides the trust with best-in-class investment capabilities and opportunities, and it has delivered earnings and distribution growth since IPO.

Negligible COVID-19 Impact

Charter Hall Long WALE REIT manages a defensive, non-discretionary income portfolio, owing to which the impact to FY20 operating income was negligible. The trust provided 0.2% of net rent as a relief to its tenants during the financial year. The properties leased to Endeavour Group paid rent despite closures.

Convenience retail portfolio of 225 assets leased to BP was operating during lockdowns and rent was received. CLW highlighted that exposure to Virgin Australia was around 3% of portfolio income.

Strong Performance Since IPO

In FY20, the trust delivered operating EPS of 28.3 cents, up by 5.2% against the previous year. During the year, it invested $ 1.4 billion, increasing portfolio valuation to $ 3.6 billion, and WALE increased to 14 years from 12.5 years at the end of FY19.

The trust has secured average 18.7 years WALE on new acquisitions while portfolio properties increased to 386 from 118 properties. The trust also added new long lease on properties with high-quality tenants, including BP, Arnott’s, NSW Government, and Telstra.

CLW has delivered a statutory profit of $ 122.4 million in FY20 compared to $ 66.9 million in the previous year. Its operating income increased by $ 51.1 million to $ 121.9 million for the year compared to $ 70.8 million in the previous year. In FY20, CLW delivered distribution of 28.3 cents per unit, up by 5.2% over the previous year.

It was noted that the trust has successfully tripled portfolio scale since IPO, taking portfolio to $ 3.6 billion from $ 1.25 billion at the time of IPO. Between IPO and at 30 June 2020, the trust has increased WALE by almost 2 years to 14 years from 12.1 years.

Net property income of the trust increased to $ 176.6 million in FY20, up by 63.1% from the previous year. This increase in income was largely attributed to a $ 53 million gain from new acquisitions during the year and like for like rental growth of 2.6%.

The increase in operating expenses was due to higher expense on new acquisitions, including higher finance cost on partially debt-funded property acquisitions. Earnings and distribution growth were driven by organic growth and acquisitions.

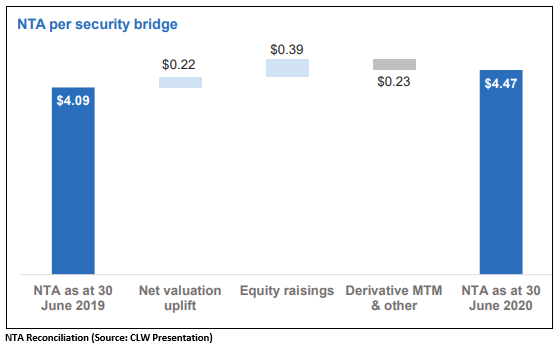

As a result of property revaluation, the trust recorded a net revaluation gain of $ 96 million. At the end of FY20, NTA per security was $ 4.47, up by 9.3% from 30 June 2019.

Capital Management in FY20

The trust raised $ 875 million through equity and established new balance sheet and joint venture debt facilities of $ 0.8 billion. Post the year-end, it divested interest in Waypoint REIT. Now the trust has an investment capacity of around $ 290 million.

As of 30 June 2020, the trust has a weighted average debt maturity of 3.9 years and a weighted average hedge maturity of 4.4 years. Its pro forma balance sheet gearing of 24.2% remains under the 25-35% range.

FY21 Guidance

CLW expects to deliver minimum operating earnings per share (OEPS) of 29.1 cents per unit in FY21, subject to unforeseen events and COVID-19 risks. The trust continues to target distribution payout ratio of 100% of operating earnings.

On 7 August 2020, CLW last traded at $ 4.970, up by 5.074% from the previous close. The trust has a market cap of $ 2.31 billion.

Good Read: COVID Diary: Strategies that helped these 100 Companies create History

All currencies in AUD unless or otherwise stated