GrainCorp Limited (ASX:GNC), based in Sydney, Australia, operates as a food ingredients and agribusiness company. The Company processes and distributes wheat, barley, and canola, as well as offers a range of malt products and service to brewers and distillers. GrainCorp also supplies and refines edible oils, serving customers worldwide.

Today, on 7 June 2019, the company announced to the market that it has executed a 10-year agreement with White Rock Insurance (SAC) Ltd to manage the risk associated with the volatility of eastern Australian winter grain production (the Contract).

White Rock Insurance is a subsidiary of UK-based Aon plc which offers a diverse suite of risk, retirement and health consulting solutions to clients worldwide.

Significance of contract

As previously announced on 4 April 2019, the Contract is significant and will support in smoothening GrainCorpâs cash flow and earnings across the strained east coast Australia grain harvests. The Contract will be effective from 2019-20 FY onward. During the term, a fixed payment of AU$15 per tonne (Production Payment) will be made for each tonne of actual east coast of Australia winter crop production in any given year which is:

Source: Companyâs announcement dated 7 Juneâ19

The total pre-tax annual cost of the Contract to GrainCorp is expected to be less than AU$ 10 million (including associated financing costs), excluding the Production Payments.

Update on sale of Australian Bulk Liquid Terminals

Recently on 10 May 2019, GrainCorp updated the stakeholders about the proposed sale of its Australian Bulk Liquid Terminals business to ANZ Terminals, subject to a condition that GrainCorp did not enter into a change of control transaction or other material alternative transaction before 10 May 2019. GrainCorp confirmed that this condition had been satisfied as of the date.

On 4 March 2019, GrainCorp announced to have entered into an agreement to sell its Australian Bulk Liquid Terminals business to ANZ Terminals Pty Ltd for a total enterprise value of approximately AU$ 350 million (representing ~13.0 times EBITDA).

Under the business segment mentioned above, GrainCorp operates around 8 liquid terminals sites located in different parts of Australia. These sites have a total storage capacity of around 211,000 m3. The sites are specialised to store and handle bulk fuels and chemicals as well as liquid fats & oils for a diverse client base, including GrainCorp Oils. Under the terms of the deal, GrainCorp Oils and ANZ Terminals would also reach a long-term storage agreement.

Commenting on the development, GrainCorp Managing Director and CEO Mark Palmquist explained that the decision to divest the companyâs assets to another skilled operator based on a long-term storage agreement, would allow the company to obtain continued access to the storage needed to support its oils business and thereby enhance shareholder value.

One of the current portfolio review considerations of the company includes sale of the Australian Bulk Liquid Terminals business.

The transaction is subject to a number of conditions including the one mentioned above: no significant opposing change, regulatory approvals, lessorsâ consents and completion of arrangements.

The financial adviser for the transaction was Blackpeak Capital and Gilbert + Tobin acted as the legal advisers.

Financial Results

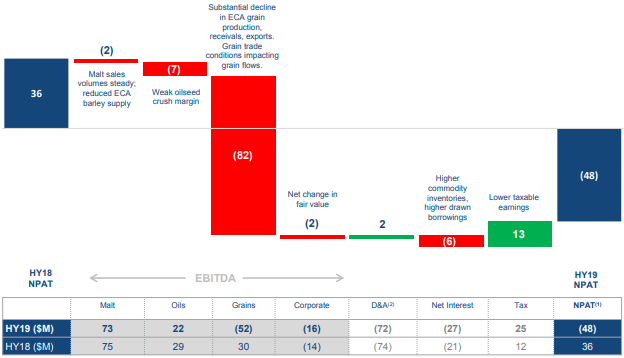

GrainCorpâs Half yearly results (for the six months to 31 March 2019), demonstrate a particularly challenging period in grains and oilseeds, including severe drought conditions in eastern Australia and disruptions in grain flows by grain trade conditions. The earnings loss due to ECA drought and grain trade conditions is explained in the figure below.

Source: Investor Presentation - Half Year Results to 31 March 2019

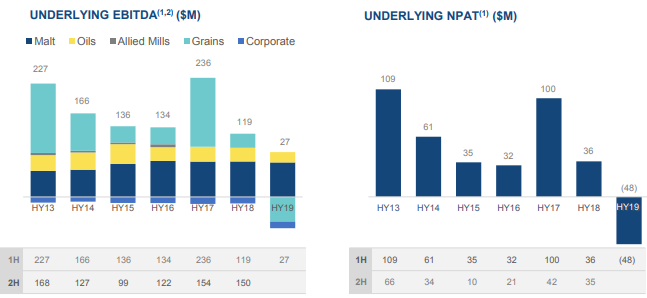

The company reported an underlying EBITDA of $ 27 million, compared to $ 119 million in the prior corresponding period in 2018 (HY18). There was also an underlying net loss after tax of $ 48 million (HY18 net profit after tax: $ 36 million) and a statutory net loss after tax of $ 59 million (HY18 net profit after tax: $ 36 million).

Source: Investor Presentation - Half Year Results to 31 March 2019

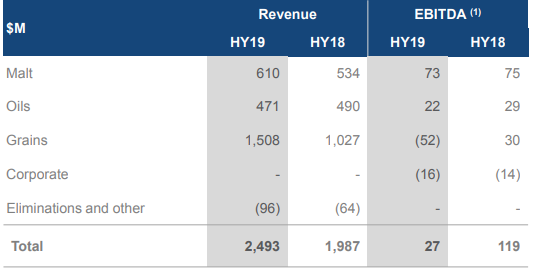

The business segment wise performance of the company is tabulated in the figure below:

Source: Investor Presentation - Half Year Results to 31 March 2019

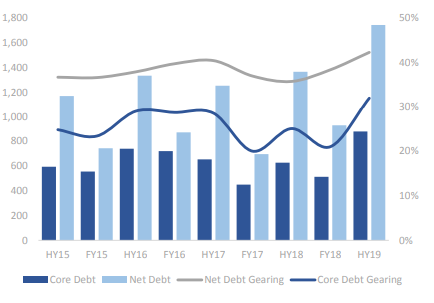

As for GrainCorpâs balance sheet profile as at 31 March 2019, the core debt stood at $ 880 million and net debt at $ 1,744 million with core debt gearing (core debt / (core debt + equity) at ~32% and net debt gearing (net debt / (net debt + equity) at ~42%.

The net debt gearing was higher due to higher inventory levels and timing of commodity shipments (increase in receivables). Besides, the range of maturities on term debt from April 2022 to March 2023 had an average term debt of 3.7 years. It includes the refinancing of the 4-year, $ 500 million evergreen facility during the half-year.

In addition, the barley inventory facilities for Malt valued at ~$171 million were included in core debt.

Source: Investor Presentation - Half Year Results to 31 March 2019

The companyâs capital expenditure has continued to decline since peaking in FY16; in line with the completion of major capital works.

Outlook

The demand for GrainCorpâs Malt products is estimated to be continually strong in the 2019 northern hemisphere summer. Besides, the company expect to obtain further benefits from the consistent improvements in Foods during the second half of the calendar year 2019.

However, challenging conditions may still prevail in eastern coast Australia (ECA) in 2HFY19 . While company is involved in planting for the winter grain crop, it is still too early in the season to forecast grain production levels.

Stock Performance

On 7 June 2019, GNC closed the market session at AU$ 8.170, climbing up 5.97% by AU$ 0.460 with around 2.26 million shares traded. The company reported a market capitalisation of AU$ 1.76 billion and ~ 228.86 million outstanding shares.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.