For quite some time, it has been observed that the number of international passengers in major Australian airports like Melbourne and Sydney Airport (ASX: SYD) has been growing at a strong rate. However, this is not the case with domestic passengers. It has been seen that the growth in domestic passengers is slowing down. If compared to International passenger growth, the domestic passenger growth is very low.

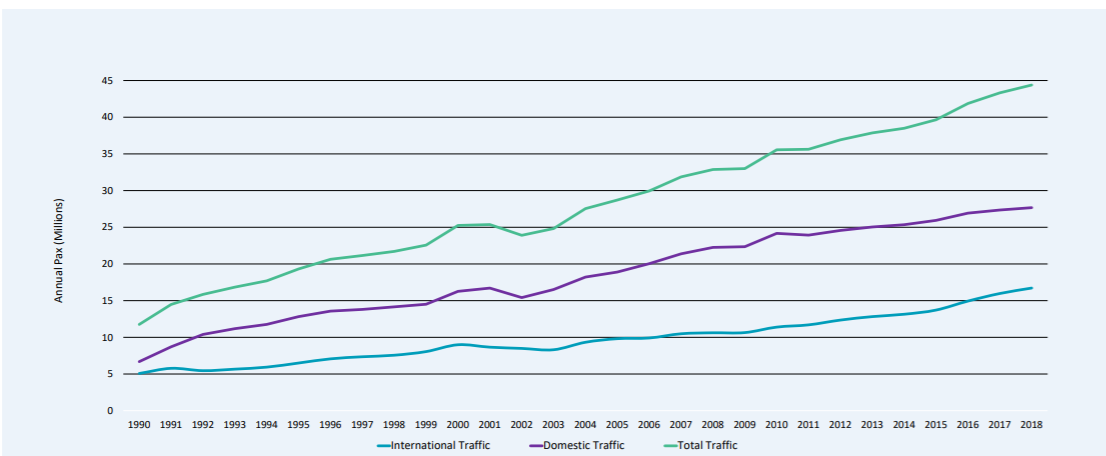

One of Australiaâs major airports, Sydney Airport has had stable and extremely resilient passenger growth, as depicted in the graph below.

Long term traffic growth (Source: Company reports)

From the above graph, it is obvious that the growth rate for domestic traffic in Sydney Airport is much lower when compared to the International Traffic.

In the month of May, SYD was Australiaâs busiest domestic airport with 2.22 million passenger movements. This was followed by Melbourne Airport, which had 2.03 million passenger movements in May month. May month saw a movement of 2 million domestic passengers, which was 0.7% higher than the previous corresponding period.

For 12 months ended May 2019, Sydney Airport reported Domestic Passengers of 27,510, which was 0.5% lower than the previous corresponding period (pcp). In case of the international passengers, for 12 months ended May 2019, the Airport reported 16,858 passengers, which was 3.4% higher than the pcp.

12 Months Traffic Data (Source: Company Reports)

Melbourne Airport Performance: In the year 2018, Melbourne Airport witnessed an intense surge in passenger growth thanks to its Airline customers and new airlines with new routes, particularly in the international market. The Airport added 1.2 million international seats in the past financial year, resulted in a growth rate of 9.4 per cent in international passenger numbers. A relatively flat domestic market, cultivated in part by the domestic carriers pursuing better yields through capacity discipline, contributed growth of 2.5 per cent.

In 2018, Melbourne Airportâs domestic market grew only 2.5% faster than any other major Australian airport. Around 25.8 million people flew in and out of Melbourne Airport during the financial year. The Melbourne-Sydney route continued to soar in popularity with 54,494 flights recorded, making it the second busiest air route in the world.

Recently, Moodyâs, a leading credit rating agency, released a report advising that the passenger growth in Australia is supporting a stable outlook for Australian airports.

Two key highlights of the reports are:

- Subdued domestic market conditions balanced by stronger international passenger growth and non-aeronautical revenue

- Sector facing large investment capital investment programs, but slowing passenger growth may lead to deferrals.

As per Moody's Vice President and Senior Analyst, Nicholas Chapman, it is expected that the aggregate passenger numbers in Australia will grow at a low single-digit percentage over the next 12-18 months, with airlines focusing on aircraft utilisation in the face of slowing consumer spending. As per Moodyâs Investors Service, the International passenger growth is expected to grow at a higher rate than domestic passenger growth.

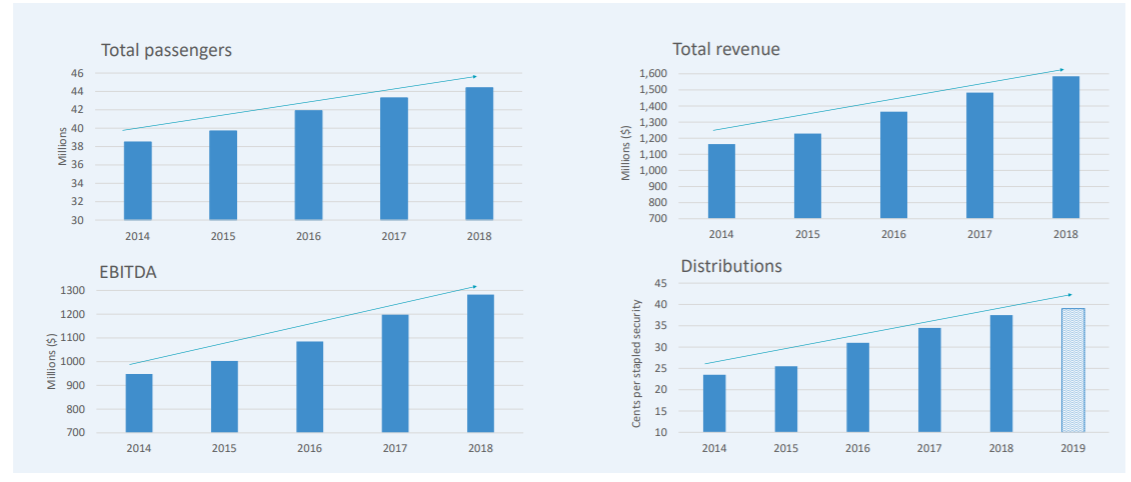

Sydney Airport Performance: Looking at the last five years, Sydney Airportâs strong passenger growth on the aeronautical side and increasingly diverse non-aeronautical business coupled with a strong strategy has delivered five-year compound revenue growth of 7.3% and EBITDA of 7.1% per annum, respectively.

At 2019 Annual General Meeting, the company informed that over the past five years, it has delivered a total shareholder return of 17.7% per annum, including the reinvestment of distributions. This compares to the ASX100 performance of 7.2% per annum over the same period. This means that if an investor invested $10,000 in Sydney Airport securities on 31st December 2013, the value of that investment, including reinvested distributions will be approximately $22,600 at 31st December 2018.

Consistent track record of revenue and EBITDA growth underpinning distributions (Source: Company Reports)

SYDâs non-aero business currently represents 51% of its total revenue, which is significant as it provides stability and resilience to the business model.

Some important stats of SYD (presented at 2019 AGM):

- 94% of SYDâs Retail revenues are underpinned by minimum guarantees

- 98% of SYDâs currently available Property sites are leased

- All Retail and Property leases have contracted escalations

- The average tenure of retail leases is five years and there is extremely high demand amongst tenants looking to gain access to sites at the airport.

In the property business, SYDâs two hotels are performing well. SYD has opened 78 new rooms at the Ibis Budget and has advanced on its plans for a new 450 room premium hotel. Beyond hotels, the Airport is looking at property expansion opportunities across the precinct. The Airport is exploring opportunities in freight, logistics, catering, lounges and advertising.

Sydney Airport expects to commence paying cash income tax from the 2022 calendar year, subject to underlying operational performance and capital investment opportunities. It is expected that the future cash tax payments will give rise to franking credits and these will be distributed to eligible investors.

In May month alone, there were 2,217 domestic passengers and 1,293 international passengers.

Highlights for the Month of May

- Qantasâ seasonal Sapporo service will commence in mid-December with a 251 seat A330-200 aircraft operating three times per week through to late-March

- Malindo Air will commence daily service from Kuala Lumpur via Denpasar in mid-August, operating a 162 seat B737-800.

Sydney Airport Stock Performance: At market close on 16th July 2019, SYDâs stock was trading at a price of $7.870, up 0.255%, with a market capitalisation of circa $17.99 billion. The counter opened the day at $7.850, reached the dayâs high at $7.920 and touched a dayâs low at $7.840, with a daily volume of ~2,890,039. In the last six months, the company has provided a return of 19.85% to its shareholders as on 12th July 2019. SYDâs stock is trading at a very high PE multiple of 48.220x and an annual dividend yield of 4.83%. Its 52-week high price stands at $8.420 and 52 weeks low price stands at $6.240, with an average volume of ~4,813,590.

A Quick Look at Melbourne Airport: Melbourne Airport has been Victoriaâs gateway to the world for almost 50 years. The airport is located around 22 kilometres northwest of Melbourneâs central business district and is well connected to Melbourneâs freeway and arterial road network. The Airport is located near to major industrial areas and three of Melbourneâs residential growth corridors. This location and accessibility mean the airport serves as a hub for the freight and logistics industry, as well as capitalise on growing labour markets. Melbourne Airport makes a significant contribution to the Victorian economy as a critical component of tourism and trade-based industries that support jobs and create economic growth.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.