Credit Corp Group Limited (ASX: CCP) is positioned as Australiaâs largest debt buyer and collector which helps customers repay their outstanding balance. The company is committed to providing sustainable financial solutions like longer-term repayment plans, consistently working on refining its business approach to deliver the right products and services as per the individualâs personal needs.

Fiscal 2019 market update

The company plans to inject more funds across all consumer lending segments and in the United States business segments to build further operational and financial capacity for future growth.

Credit Corp, therefore, has increased its FY19 investment guidance; Purchased Debt Ledger (PDL) acquisitions has been upgraded from its previous range of $200 - $210 million to $210 - $215 million. It maintains its NPAT guidance at $69 - $70 million with the estimate to deliver EPS within the guidance range of 144 â 146 cents.

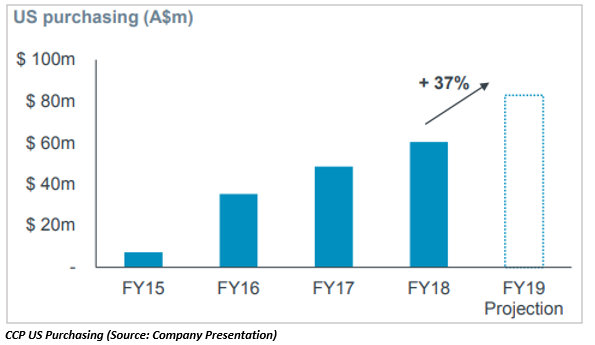

In the recent market update, Credit Corp confirmed the favorable market conditions in the US, thereby allowing the company to accelerate its US strategy with investment almost 40% higher relative to FY2018. Increased investment and growth in productive capacity has improved the companyâs medium-term outlook for the US debt buying segment.

The core Australia/New Zealand debt buying operation has performed well with cash collections tracking close to the record levels of FY2018.

As per the announcement dated 1 April 2019, CCP loan book stands at $208 million suggesting an improved segment growth outlook for Fiscal 2020. The report further read that Credit Corp is on track to deliver strong earnings growth in Fiscal 2019.

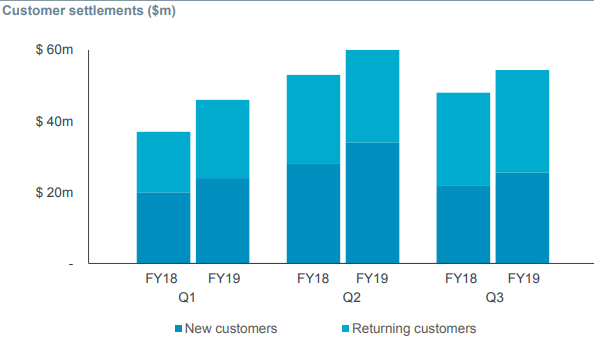

Moreover, in the consumer lending segment, the company has reportedly experienced growth in new customer volumes and settlements of almost 20% relative to FY2018.

CCP Customer Settlements Summary (Source: Company Presentation)

Underwritten Placement

In April, Credit Corp raised A$125 million via a fully underwritten institutional placement. The strong support from new and existing institutional investors increased the size of the placement by A$25 million from the initial placement size of $100 million. Proceeds from the placement strengthened the companyâs strategic position with further flexibility in the balance sheet. In settlement of the placement, ~6 million New Shares were intended to be issued at an offer price of A$20.45.

The additional equity raising pulled down the groupâs gearing initially to ~17%, which was earlier expected to be reduced to ~20%. But ROE is expected to remain comfortably above the target range of 16-18% while the company ramps up its strategic expansion initiatives across Australia and United States.

These additional funds were believed to provide a significant headroom to Credit Corp in committed undrawn debt facilities and a robust balance sheet, enhancing its capacity to pursue strategic growth initiatives.

Credit Corpâs CEO Thomas Beregi said that: âCredit Corp is witnessing very favourable market conditions for its business in Australia and the opportunity in the US continues to be increasingly attractive. The equity raising provides the Group with the flexibility and liquidity to take advantage of these opportunities, further bolstering the outlook for the business over the medium term.â

Use of Capital Proceeds from Placement

Credit Corp intended to utilise the proceeds to accelerate the execution of the groupâs strategic expansion initiatives including three major areas that include:

Australia/New Zealand Debt Buying: Amid the tighter capital availability, the company attempts to maximise the opportunity to participate in a potential re-balancing of the Australia/New Zealand debt buying market and derive benefits from the industry dynamics by the utilisation of these proceeds.

US debt buying: At the backdrop of favorable market conditions in the US, the company intends to accelerate growth with a second operational site planned to be opened in Q2 of FY2020, with the existing Salt Lake City, Utah site expected to be filled in Q1 of FY2020.

Balance sheet flexibility: Debt buying can be opportunistic and increasing capital headroom maximises Credit Corpâs flexibility to respond to market conditions. The reduction in groupâs gearing and ROE above the target range have been the major highlight of the placement offer as stated above.

Non- Underwritten SPP

In May, the company completed A$15 million Share Purchase Plan, intending to issue ~0.734 million shares at A$20.45 per share (Same as that of institutional placement). The applications received massively exceeded the A$10 million target; the company decided to scale back the SPP applications to A$ 15 million on pro-rate basis.

Half-Year Results for 1HFY19

For the first half of Fiscal 2019, the company reported 13% increase in Net Profit after Tax (NPAT) to $33.6 million, largely driven by 18% growth in the consumer loan book to $203 million. With respect to US business, Credit Corp generated 71% revenue growth with solid PDL investment pipeline. The companyâs consumer lending growth has been the key highlight during the period, resulting from the 20% increase in new customer volume.

Further, CCPâs total investment in financial assets grew by 5% compared to the prior year. In the US segment, the company secured a A$83 million investment pipeline, representing 37% increase on FY18 purchasing. This investment includes the largest seller of charged-off debts in addition to the other new issuer.

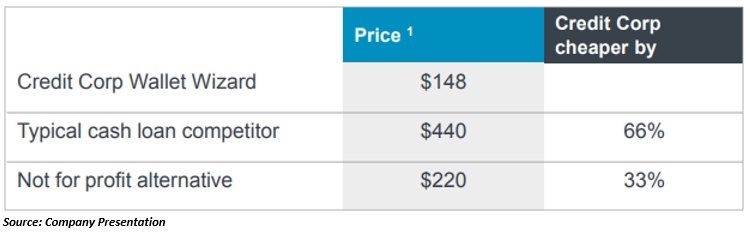

Commenting on the cheapest and sustainable product offering, Mr Beregi stated that Wallet Wizard is the cheapest cash loan available in the segments in which the company operates in the market. It represents the extremely cheaper offering compared to any commercially provided offering or even any charitably funded alternative from the not-for-profit provider.

As per the companyâs investor presentation, banking facilities have expanded the limits to $350 million, maturing in 2022 and 2023. It is expected to provide a projected headroom of ~140 million at year-end Fiscal 2019.

Going forward, the company continues to build its Salt Lake City site and plans to grow its purchasing accordingly. It is eyeing further US profit growth in FY20 while investment in FY20, assisted by additional balance sheet capacity, will position US segment for stronger profit growth beyond FY20. Further, the groupâs 2019 earnings guidance has been revised to represent profit growth in the range of 7% to 9%.

Stock Performance

CCP is currently trading at $27.0 on 21 June 2019 (1:37 PM AEST). The stock is trading at a price to earnings multiple of 18.950x with a market capitalisation of $1.48 billion.

Since its listing on ASX in 2000, CCP has surged up by 1691.95% including a positive price change of 210.34% in the past five years. Whereas, in the short-term, the stock price has gone up by 16.63% in the past three months. It has offered a YTD return of 44% to its investors.

Also Read: A Lens Over Credit Corp Groupâs Strong Operational Performance

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.