Nickel, like many other base metals such as copper, is showing slight recovery with prices of nickel futures (CFD) rising from its recent low of USD 10,867.50 (intraday low on 23 March 2020) to the level of USD 11,997.50 (intraday high on 15 April 2020), which underpinned a price appreciation of ~ 10.39 per cent.

To Know More, Do Read: Base Metals Out of Woods Poised for an Overnight Spike or Risk of Another Sell-off Remains?

While nickel prices are recovering many independent forecasters are suggesting that post a volatile 2019, nickel prices are expected to be comparatively less volatile in 2020. In 2019, the prices were deeply supported by the export ban on nickel imposed by Indonesia; however, the recent COVID-19 outbreak exerted tremendous pressure on nickel prices, which had been trading down for quite some time to reach a low of USD 10,867.50 from its recent peak of USD 18,842.50 (intraday high on 2 November 2019), down ~ 42.32 per cent.

To Know More, Do Read: Indonesia Export Ban to Create a Nickel Boom while Mincor and Independence Develop Assets?

However, the nickel market is expected to be characterised by a growing market deficit; as healthy growth uptick led by consumption could outweigh Indonesia’s export ban. The Department of Industry, Innovation, and Science (or DIIS) anticipates the commodity to average at USD 15,300 per tonne in 2020, up by 7.7 per cent against the average price of USD 14,200 per tonne seen in 2019.

How is Price Growth Linked to New Battery and Stainless Steel Demand?

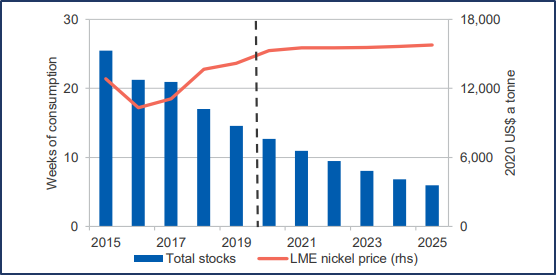

Nickel prices are estimated to derive much steam from solid stainless steel demand and battery manufacturing in the future, and DIIS projects an average surge of 1.8 per cent a year in nickel prices till the end of 2025, which would take the average price to USD 15,800 per tonne, in real terms.

Also Read: Lens Over Nickel Dynamics; CTM Reports High Quality Assay Result

Projected nickel spot prices and stock levels (Source: DIIS)

The DIIS further anticipates the ongoing growth in stainless steel production to provide nickel with a much-needed fillip ahead and improve the consumption from 2.4 million tonnes in 2019 by 0.4 million till 2025, projecting a consumption growth of 2.2 per cent a year. However, the current consumption estimations by the DIIS is slightly lower against its previous estimations amid a slowdown in growth in China and global GDP.

The current COVID-19 outbreak, which has imposed serious challenges to the Chinese growth, would keep a lid on nickel. Apart from stainless steel, the use of nickel in battery making is anticipated to expand over the years with an increase of nickel share, as technological advances are capable of making batteries with a higher quantity of nickel.

Also Read: How are the ASX Listed Lithium Stocks Placed Amidst the COVID 19 Tsunami?

Where is Australia Going To Fit in the Projected Global Deficit?

Australia holds 26 per cent of global nickel resources and produces an average of 200,000 tonnes of nickel each year, which contributes over $3 billion to the economy. The DIIS anticipates nickel export earnings to grow till 2025 amid strong prices and new capacity, which could further increase the production.

In 2019–20, export earnings are forecast to stand at $5.4 billion, up by 46 per cent against the previous corresponding period, and the momentum is expected to continue over the years till 2025, with real export earnings surging over 10 per cent a year to stand at $6.6 billion by 2024–25.

The surge in export earnings is anticipated in the wake of high prices and steady growth in volumes due to strong nickel market. Export volumes are anticipated by the DIIS to reach at 436,000 tonnes by 2024-25, up by ~ 48.39 per cent from 225,000 tonnes in 2018-19.

- The ongoing expansion and restarts

The anticipation of a global deficit and strong prices have stimulated investment in nickel capacity and potential mine restarts. The DIIS anticipates that the mine production across the continent would lift from 161,000 tonnes in 2019–20 to 275,000 tonnes in 2024–25, reflecting an average yearly increase of 9.4 per cent.

The current investment in Nickel West projects in Western Australia, including the Yakadindie and Venus deposits, operated by BHP Group Limited (ASX:BHP) and parallel investment in Kwinana Refinery would further support the growth in volumes. The Savannah mine- operated by Panoramic Resources Limited (ASX:PAN), which restarted in 2018 is anticipated by the DIIS to reach higher production ahead as ore grades improve.

Apart from the expansion and investment across the nickel capacity, the potential restart of several mines would also support the nickel export volumes ahead. Potential prospects such as Mincor’s Long and Cassini- operated by Minor Resources Limited (ASX:MCR), Ravensthorpe mine- operated by First Quantum Minerals Limited (Canada-based), and Nickel’s Black Swan-operated by Poseidon Nickel Limited (ASX:POS), are well-positioned to support Australia’s volume growth ahead.

To Know More, Also Read: Nickel Future Prospect And Lens Over The Potential Shiners- POS, MCR and MLX

- The growing exploration expenditure

The exploration expenditure for nickel and cobalt continued to increase across the continent, with expenditure reaching $63 million during the December 2019 quarter, which underpinned a year-on-year growth of 25 per cent.

To Know More, Do Read: Tesla and Others are Back for Cobalt; Australian Mines’ Sconi Project To Lead the Australian Front?

Global Production Forecast

The global nickel mine production, which grew rapidly in 2019, and is further estimated by the DIIS to further increase; however, the export ban by Indonesia would keep a large production out of the global supply chain, which could benefit the Australia nickel exporters and mining companies.

The global mine production is projected to increase at a yearly average of 2.0 per cent to reach 2.9 million tonnes by 2025; however, the growth is not expected to remain linear, and DIIS sees a potential contraction across the global front in the near-term.

The department further anticipates that a lower contribution of Indonesia across the global supply chain would be captured by Brazil and Australia.