Summary

- Coal prices are now turning around slightly after taking a considerable fall, with New Castle Coal Futures recovering by ~13.27 per cent from its low of USD 59.15 a tonne to USD 67.00 a tonne.

- Coal market has witnessed a weak performance during the June 2020 quarter over major steel production pullback from North-East Asia and India.

- In the recent past, China has again emerged the largest consumer of the Australian coal due to its ongoing zeal to capture a large tranche of the global steel industry.

- However, despite a record Chinese import of thermal coal and metallurgical coal, the uncertainty around its policies import policy is keeping a lid on coal prices.

- Amidst considerable fall in benchmark coal indices, Whitehaven Coal Limited (ASX:WHC) has witnessed strong production during the June 2020 quarter.

Coal prices are finally taking a breather from a down-plunge with prices of Newcastle Coal Futures (NCYc1) surging from its recent low of USD 59.15 a tonne (intraday low on 28 April 2020) to the present high of USD 67.00 a tonne (intraday high on 7 July 2020) to mark a price appreciation of ~ 13.27 per cent after a drastic fall from its high of USD 111.00 a tonne on 3 September 2018.

- The June 2020 quarter saw the continued impact on many economies due to COVID-19, and despite a record import of Australian thermal and metallurgical coal into China during the first half of the year 2020, uncertainty surrounding future Chinese import quotas weighed upon coal prices in the June 2020 quarter.

China is poised to grab a large tranche of the global steel industry and still remains the largest customer of the Australian supply; however, in the recent past, stringent policies adopted by the government to support the local coal mines, posed headwinds for ASX-listed coal mining companies.

To Know More, Do Read: China Poised to Grab the Global Steel Trade as Economies Open up for Trade

Furthermore, actions taken by steel producers across Asia and India to defer metallurgical coal shipments in response to weak steel demand has caused the hard coking coal price to soften during the June 2020 quarter, adding to the wide list of challenges faced by ASX-listed coal mining companies.

- For example, Whitehaven Coal Limited (ASX:WHC) witnessed a deferral of shipment in the June 2020 quarter (Q4 FY20) over steel production cut implemented by India and North-East Asia.

- However, despite a snail-paced demand across Asia and tough competition to park the coal in China, WHC’s coal sales reached 17.5 million tonnes, fulfilling the FY20 guidance.

WHC Managed and Equity Total from Continuing Operations

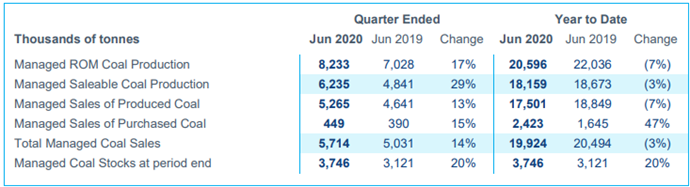

Managed Totals (June 2020 Quarter)

- WHC produced 17 per cent higher managed Run-of-Mine (or ROM) coal during the June 2020 quarter against the previous corresponding period (or pcp).

- The managed ROM coal production for the period stood at 8.2 million tonnes, while managed saleable coal production soared by 29 per cent against pcp to stand at 6.2 million tonnes.

- Furthermore, the managed sales of produced coal rose by 13 per cent against pcp to stand at 5.2 million tonnes, and the managed sales of purchased coal surged by 15 per cent against pcp to reach 449k tonnes during the June 2020 quarter.

WHC witnessed an increase of 14 per cent in total managed coal sales against pcp during the June 2020 quarter at 5.7 million tonnes and held 20 per cent higher managed coal stocks against pcp at the end of the June 2020 quarter.

The snippet of the managed totals performance from continuing operations for June 2020 quarter and on a YTD basis (end of June 2020 quarter) is as below:

Managed Coal Performance (Source: Company’s Report)

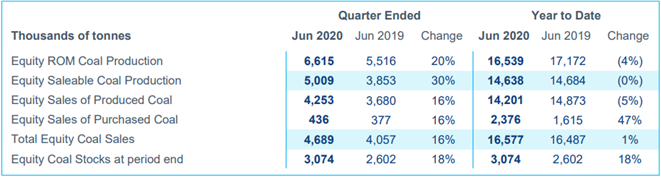

Equity Totals (June 2020 Quarter)

- WHC’s equity ROM coal production surged by 20 per cent against pcp during the June 2020 quarter to stand at 6.6 million tonnes.

- The equity saleable coal production soared by 30 per cent against pcp to stand at 5.0 million tonnes.

- The equity sales of produced coal rose by 16 per cent against pcp to stand at 4.2 million tonnes.

- The equity sales of purchased coal also increased by 16 per cent against pcp to stand at 436k tonnes.

The Company observed an increase of 16 per cent in total equity coal sales against pcp during the June 2020 quarter at 4.6 million tonnes and held 18 per cent higher equity coal stocks against pcp at the end of the June 2020 quarter.

The snippet of the equity totals performance from continuing operations for June 2020 quarter and on a YTD basis (end of June 2020 quarter) is as below:

Equity Coal Performance (Source: Company’s Report)

Equity Coal sales and Average Realised Price

- The total equity coal sales stood at 4.7 million tonnes during the June 2020 quarter, up by ~ 27.02 per cent against the previous quarter and up by ~ 6.81 per cent against pcp.

- The equity own coal sales rose by ~ 34.37 per cent against the March 2020 quarter to stand at 4.3 million tonnes, which also remained ~ 10.25 per cent higher against pcp.

On the price counter, the decline in coal demand from Asia took a toll on the benchmark SSCC and PCI coal, which settled at USD 95 a tonne and USD 101 a tonne during the June 2020 quarter, respectively. Furthermore, prices of new castle coal index benchmark tumbled ~ 19.11 per cent during the same period to settle at USD 55 a tonne.

- Despite a low-price environment, WCH realised price on thermal coal of USD 59 a tonne, a ~ 7.27 per cent premium against new castle coal index benchmark. However, due to steel production pullbacks across Asia, the average realised price on metallurgical coal of USD 76 per tonne represented a 20 per cent discount to the JSW quarterly (SSCC), though a 20 per cent premium of the spot price.

Corporate Performance and Future Guidance

WHC received a high assurance rating from the Australian Taxation Office post the completion of a comprehensive Streamlined Assurance Review, covering FY2015 to FY2018, during the June 2020 quarter.

- Furthermore, the Company finalised a fully amortised Japanese export credit agency facility of $51.7 million with two leading Japanese banks and the Nippon Export and Investment Insurance Company.

- At the end of the June 2020 quarter, WHC held fixed price contracts of 1.55 million tonnes of managed thermal coal sales, 980k tonnes and 570k tonnes of which is expected to be delivered in the September and December 2020 quarter, respectively.

- Furthermore, as on 30 June 2020, WHC had a USD 78.34 million forward AUD/USD exchange contracts in place at an average exchange rate of AUD 1.00 = USD 0.64350 or equity coal sales of ~1.2 million tonnes.

The stock of the Company last traded at $1.500 (as on 15 July 2020 02:27 PM AEST), down by 1.31 per cent against its previous close on the exchange.