Natural gas prices are observing large spread decline across various geographies over the varying demand and supply dynamics. While the domestic market is running short of natural gas, which is also supporting the ASX oil & gas stocks such as Santos Limited (ASX:STO), the international markets such as of the United States is under natural gas supply glut, which has constantly exerted pressure on the Henry Hub spot.

To Know More, Do Read: ASX-LISTED OIL & GAS STOCKS- A PERFECT BUY FOR SHORT-TERM GAINS?

The shortage of natural gas in the domestic market is mainly over the higher LNG exports, which is again forecasted by the Department of Industry, Innovation and Science (Or DIIS) to surge by 8 per cent from 75 million tonnes (2018-19) to 81 million tonnes in 2020-21.

The booming LNG industry is depleting the natural gas supply chain, which is propelling the natural gas prices in the domestic market. The increase in gas prices combined with a higher spread between LNG spot and oil-linked contract prices, at which most of the LNG exporters sell their LNG, could now bring potential headwinds for the LNG sector.

Short-Term Challenges Ahead for LNG Industry

· Nuclear Again Gaining Momentum in Japan

Japan, which is the primary market for Australia’s LNG export, is now observing resurrection in the nuclear-based energy generation. Australia earned 43 per cent of its LNG export revenue from Japan in 2018-19; however, the LNG imports in Japan is now consistently declining.

The overall LNG imports in Japan fell by 7.6 per cent on a yearly basis in the first nine months of 2019 and is further anticipated by the DIIS to drop by 6 million tonnes to stand at 75 million tonnes in 2021.

Nuclear Generation Revives in Japan: ASX-LISTED ALTERNATIVE ENERGY STOCKS UNDER INVESTORS’ LENS AS OIL RISK SURMOUNTS

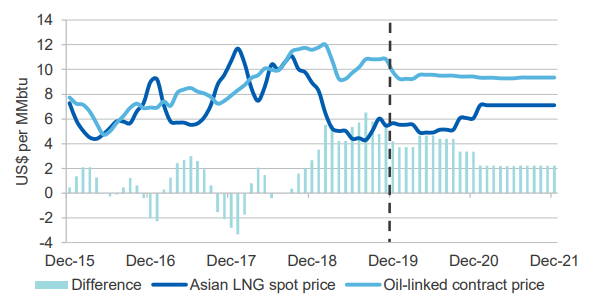

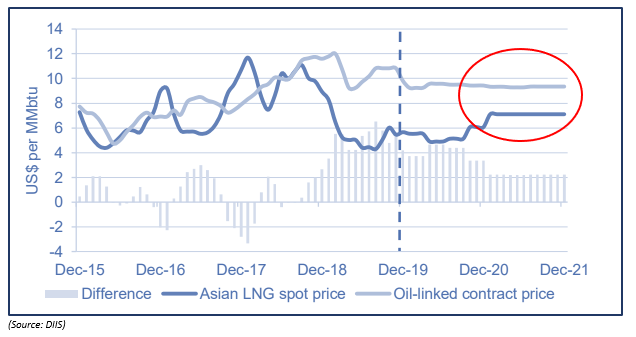

· Weak Demand Over Large Spread Between LNG Spot and Oil-Linked Contracts

In Asia, the spot prices of LNG improved slightly from the record lows observed by the market during the end of September 2019 quarter; however, still remained at multi-year low, over the industry anticipated LNG supply glut across international energy markets.

The LNG spot prices in Asia averaged about $8.80 a gigajoule during the December 2019 quarter, up by 25 per cent against the previous quarter; however, 40 per cent lower on a yearly basis. The prices boosted over minor supply disruptions across major LNG exporting countries, albeit, the arrival of long-anticipated overcapacity in LNG supply kept the prices under check.

Currently, the LNG spot prices in Asia are witnessing a large spread with the long-maturity oil-linked contract prices, which most of the LNG players in Australia deal, which in turn, is further reducing the demand for gas contracts.

(Source: DIIS)

The large spread, which makes the LNG costly for buyers is reducing the demand in the status quo; however, the falling spot prices of LNG in Asia could eventually reduce the spread ahead and boost the demand.

Booster For LNG Players

· High LNG Demand In China

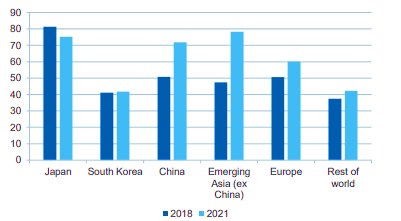

China generated the second-largest tranche of LNG export revenue by accounting 35 per cent of the overall LNG export revenue in 2018-19. China imported 51 million tonnes of LNG in 2018, and the imports continued to grow during the first ten months of the year 2019 to mark a 14 per cent rise against the previous corresponding period.

However, in the status quo, the relaxation in the policy to switch from coal-to-gas in China coupled with a temporary shutdown in the Jiangsu Rudong LNG terminal due to a typhoon is exerting slight pressure on LNG demand in China as well, which could be considered as short-term challenge faced by the LNG industry in China.

The local government in China has relatively eased the coal-to-gas switching to boost the GDP, which took a plunge over the escalated bilateral trade issues in the recent past. Apart from that, the coal prices in Chian is now plunging, which is further allowing the energy generation from coal-fired power stations.

Despite such short-term challenges, the industry experts anticipate the gas consumption in China to increase in the coming years over the continuous efforts from the government to reduce the carbon footprints.

The DIIS anticipates the gas consumption to reach 364 bcm, up from an estimated 280 bcm in 2018 to represent higher gas proportion in energy generation from 7.0 per cent in 2017 to 8.3-10 per cent in 2020-21.

Furthermore, domestic gas production in China is also anticipated to increase along with an improvement in gas-related infrastructure.

LNG Import Forecasts (Source: DIIS)

· Falling Spot Prices To Increase Demand

As we mentioned above, the higher spread between the oil-linked contracts and spot prices is narrowing down the demand in China; however, over the short-term, the LNG supply is forecasted by many independent research houses to surge, which would eventually bring the spot prices down.

The fall in LNG spot prices could eventually prompt the buyers to secure more flexible deals in terms of gas-linked prices. The fall in spot prices could further prompt the buyers to purchase more spot cargoes as compared to long-term oil-linked gas contracts.

Such a fundamental shift would eventually reduce the spread between spot prices and oil-linked contracts by improving the LNG demand. The improvement in LNG demand, coupled with a reduced spread between the oil-linked contracts and spot LNG, could eventually ignite the demand for LNG over the long-run.

Thus, the short-term price challenges faced by the LNG sector could eventually lead towards the cascade of long-term supporting factors.

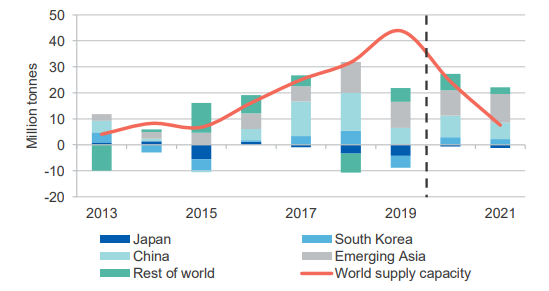

· Re-Balance in the Demand and Supply Dynamics

As explained above, the short-term fall in LNG spot prices could align the market with gas-linked prices, which derives its value from demand and supply fundamentals of LNG rather than oil-related factors, which is further anticipated by the DIIS to rebalance the demand and supply dynamics in the LNG market.

Once rebalanced, the higher forecasted demand and lower forecasted supply (by many industry experts such as DIIS), could eventually support the domestic LNG industry.

Annual change in LNG demand and world supply capacity (Source: DIIS)

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.