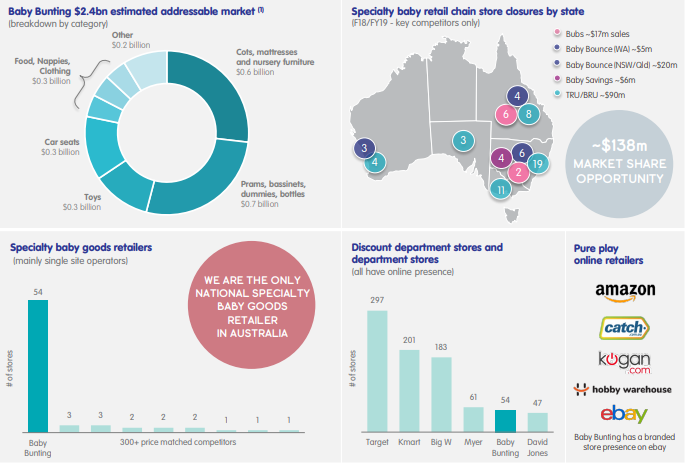

Established in 1979 as a single store, Baby Bunting Group Ltd (ASX: BBN) has evolved to become Australiaâs largest specialty baby goods retailer. Incorporated in 2007, it comes under the consumer discretionary sector serving as a one-stop baby shop that offers various baby products ranging from prams to food and formula products, and accordingly gets linked with the product category occasionally. Currently, BBN operates 52 stores across Australia with a network plan of over 80 stores.

Baby Bunting Group Ltd released a Chairmanâs and CEO & Managing Directorâs address and trading update to the stakeholders with respect to the summary of FY19 and FY20 guidance and the presentation (delivered in the Annual General Meeting on 08 October 2019).

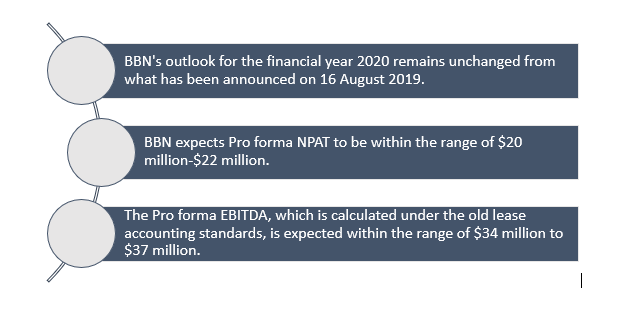

With respect to the FY2020 outlook, Baby Buntingâs CEO & Managing Director Matt Spencer stated that BBN group had a robust start to the year with the business remains to be on the path to deliver FY20 guidance

Comparable Store Sales

On a year-to-date basis, the Comparable store sales grew 3.1%, indicating the cycling of unusual trading conditions in first quarter of FY19 because of Babies R Us closure and the clearance drive of some high-end cots and prams in September 2018. The online sale reduced due to a technical problem which arose from the transitioning process from the old to new web platform; however, the company is expecting to see an acceleration in online sales. As per the FY20 guidance, the comparable store sales growth is predicted to be mid-single digits for the year.

Q1 FY20 Gross Profit Margin

For the first quarter of the financial year 2020, the gross profit margin remains to fortify by over 36.6% year-to-date, representing an increase of 270 basis points on the prior corresponding period. The growth in gross profit has outperformed the Companyâs expectation, reflecting progress on the front of private label and exclusive products range together with fewer activities on clearance in comparison to the previous year. The Company is expecting that this level of performance would continue throughout the year.

A New Refreshed Visual Identity

Baby Bunting crossed a significant milestone on its 40th anniversary year, with the launch of an exciting new brand. The Company opened a new store at Westfield Doncaster which is the first to have the new branding. Additionally, BBN group has planned to open further two stores at Wetherill Park and Casula in Sydney, in the first half of FY20 with additional two stores to be opened in the second half of the year.

FY20 Outlook

The release issued by Baby Bunting Group Limited also threw light on the FY 19 results.

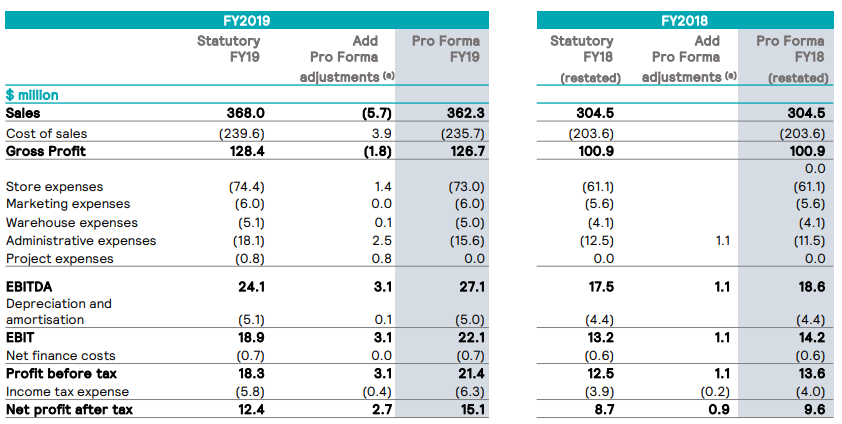

FY19 pro forma results summary

BBN set up itself as the go-to spot for baby goods in the Aussie land in 2019. Below are the highlights of the FY19 results summary.

| BBN held a net cash of $ 2.7 million at the end of the year placing the Company in a sound financial position. | |

| Sales | · On a 52 weeks pro forma basis BBN reported a growth of 19% in total sales on the previous corresponding period (pcp), amounting to $362.3 million. The comparable store sales grew by 8.7%. |

| Gross Profit | · BBN group reported a Gross profit of 35%, wherein the gross profit income was $126.7million, the Gross Profit growth was 25.6% and the Gross Profit % up 190 bps. |

| EBITDA | · The earnings before interest, tax, depreciation and amortization was $27.1 million, which was 45.9% higher on the pcp, with the EBITDA margin of 7.5%. |

| NPAT | · Pro forma net profit after tax was recorded at $15.1 million, representing a growth of 58.2% to end the year. |

| ROFE | · The FY19 capex stood at $11.8 million and operating cash flow amounted to $25.4 million. |

| Dividends | · A total dividend of 8.4 cents per share (fully franked) has been paid by the Company reflecting an increase from 5.3 cents compared to the prior year. |

BBNâs Growth Strategy

BBNâs growth strategy of âGrow market shareâ remains unchanged with four key fundamentals-

-

Investment in digital delivering the best possible customer experience across all channels

- Online (Click and Collect) sales grew by 46%, representing 11.6% of the total sales for FY19.

- Growth of 55% in click and collect sales.

-

Investment to increase sales from existing stores

- BBNâs leading customer service offering is underpinned by knowledgeable advice and guidance with an NPS score of ~75, a rise from ~70 on the previous corresponding period.

- BBNâs car seat fitting sales increased 29% year-to-year across all comparable stores.

- Leveraging store network, the Company aims for same-day online fulfilment (metro markets), with operational Hobart & Cannington hubs.

-

New Market Growth

- The Company plans to roll out more than 80 new stores.

- A new store at Doncaster Westfield opened on 5 October 2019, and two new stores at Casula & Wetherill Park (both in NSW) are anticipated to open in first half of FY20.

- Improvement in Profit Margin

- Expansion in gross margin through increases in scale, improvements in the supply chain, sourcing improvement, and progress in private label and exclusive product development.

The Platform for Future Growth

After the Company experienced the competitor disruption in FY18, BBNâs objective was to raise market share and recuperate profitability with an aim to make capital on the market share opportunities arising from shutting down of competitor stores, to secure potential key locations from store network, to stabilise gross margin without compromising on the value of the product, to gear up and invest in Private Label & Exclusive Product expansion program, to fetch some investment from stores, people and systems to support the growth.

Turning to the Board

In FY19, the Company appointed Gary Kent as a non-executive director. Mr Gary has rich experience in the retail and services sector and has led successful careers at Coles Myer and the Coles Group, at Skilled Group and at Healthscope.

Changes in Structural Landscape

During FY19, the Company witnessed changes in the structural landscape whilst the market opportunity remains significant during this changing retail landscape.

BBNâs Structural Landscape (Source: BBNâs Report)

Transformation â Investing to grow

The Company invested significantly in transformational projects for increasing profitability and supporting future growth. For the financial year 2020-2021, BBNâs expenses involved nearly 20 million capex, nearly 5 million project expenditure, nearly 4 million accelerated amortizations.

The Company also has substantial business transformation project in the pipeline over the next 2 years including:

Operational Priorities for FY20

BBN mapped out the priorities that support its operational and financial performance for the year. A key priority is to grow its strategic investments to plan. In this regard, the Company has already made significant investments during the financial year with the ability to fund the transformation agenda. Another priority is to progress its gross margin to more than 36% without any compromise on value offered to the consumer. Furthermore, the Company is focused on accelerating the capitalisation in private label to expand its private label and exclusive product with sales exceeding 35%. Aiming further to capitalise on shopping centre opportunities as they come. And finally, attaining operating leverage via its retail network.

Statutory - Pro Forma Income Statement Reconciliation. Source: Company Presentation

Stock Performance

BBNâs stock is trading at $3.55, up by approximately 1.42% on 09 October 2019 (2:05 PM AEST). The Company has a market capitalization of $442.54 million and 126.44 million outstanding shares with a YTD return of 56.25%.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.