Trophon 2 to push growth: Nanosonics Limited (ASX:NAN) failed to post good numbers in FY18 with the decline of almost 79% in the net income after tax at $5.75 Mn compared to $26.15 Mn in the previous comparable period. However, the major reason behind the sudden drop in the profit was due to earlier than expected approval of Trophon 2, resulting in the rundown of the Trophon EPR inventory by the distributors. Moreover, customers also deferred the purchase of the Trophon EPR, awaiting the launch of the upgraded version.

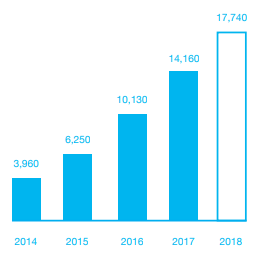

There has been a significant increase in the Trophon install base across the countries. Further, the road ahead for Trophon looks smooth as there have been certain studies in the area, talking about the limitations of current disinfection methods. The global installed base of Trophon has reached 17,740 and throughout FY18 including 26% growth in North America to 15,620 units and 49% growth in Europe to 730 units.

Trophon Installed Base Growth (Source: Company Reports)

On the analysis front, the company has maintained its debt/equity ratio of 0.01x which is less than the industry average of 0.24x. Further, NAN is sufficiently liquid with quick ratio of 6.65x compared to the industry mean of 1.67X. Meanwhile, NAN has performed well on the bourses, generating positive YTD return of 16.07%. The stock did correct from the higher levels of $3.780 on the back of a director Mr. Maurie Stang, Non-executive chairman of Nanosonics offloading 43,640 quantity. Despite the fall, the price did not break below its support level of $3.131. We believe that strong demand for Trophon 2 and increased funding towards the research and development to develop new infection prevention solution would underline the profits of the company. Investors can keep a watch on the stock for further developments in the company.

Paragon Care Limited

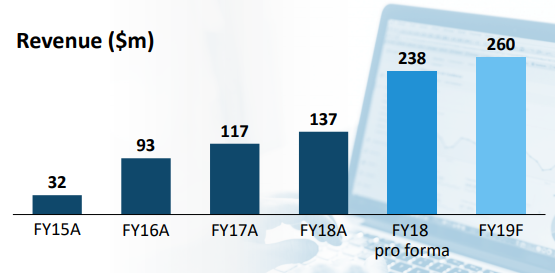

Upbeat Forward-looking statements: Paragon Care Limited (ASX:PGC) has posted good numbers and FY19 guidance looks promising as well with the company expecting a significant increase in the revenue and bottom-line numbers. In FY19, Paragon is targeting $260 Mn in revenue assuming optimum contribution from the series of acquisitions made in FY18. Recently, the company has completed the strategic private placement to China Pioneer Pharma Holdings Limited, raising AU$45.2 Mn at the premium of AU$0.91 per share. The shares were placed at a premium exhibiting the confidence that China Pioneer about the Paragon shares being undervalued. Further, the company is targeting $3 Mn in cost savings during FY19.

Revenue Projection (Source: Company Reports)

On the analysis front, the company has maintained the Net Interest Margin at 8.0% which is higher than the industry average of 4.4%. Both quick ratio and current ratio indicate good health of the company at 1.15x and 1.88x respectively compared to the Industry average of 0.91x and 1.03X respectively. On the stock performance front, the stock had a decent run on the bourses generating 1.39% in six months. Recent offloading of the shares by one of the directors caused sell-off in the stock but the price has been respecting its crucial support level. Any movement above the range $0.741 - $0.761 would take the stock higher. The stock can be watched out for growth catalysts and new developments that might trigger a rally in the share.

The Income available from dividends remains attractive for many investors.

We take a look at the best yields on the market and assess what they say about a companyâs prospect.

One Thing is certain, though, Australia interest rates are still low, making income difficult to come by and keeping the focus for many investors on high yielding stocks. Kalkineâs team of analysts bought you handpicked report for âTop 25 Dividend Stocks For 2018.â

ASX-relevant Special Reports are published year-round to provide a detailed analysis into an investing opportunity or a potential risk to your portfolio.

Click here to get your free report.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkinemedia.com  and associated websites are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.