The below-mentioned stock belongs to the funerals, cremation and memorials services industry or commonly known as the death care industry. These stocks have fabricated strong operational progress in the recent past and in addition, have also provided significant returns to its shareholders in the past few months. Letâs take a quick look at the performance of these stocks.

Propel Funeral Partners Limited (ASX:PFP)

A leading funeral service provider, Propel Funeral Partners Limited (ASX: PFP) recently completed acquisitions of Morleys Group, Waikanae Funeral Home and Kaitawa Crematorium. The company has been building on its strong and long history of acquiring and integrating profitable acquisitions of private businesses, tie-ups, infrastructure and related assets, which operates within the death care industry in Australia and New Zealand.

The company operates in the death care industry, which provides essential services to individuals and families dealing with or preparing for, death and bereavement. This includes the collection and transfer of the deceased, mortuary services, embalming, arranging and conducting a funeral, cremation, burial and memorialisation. Propel was founded in FY2012 with one funeral home and since has experienced significant growth, successfully expanding its geographical presence and diversifying its operations through the completion and integration of 24 profitable acquisitions. Propelâs location footprint is difficult to replicate as many of its funeral homes have been operating since the late 1800s and early 1900s. Propel has a strong presence in the regional areas of New South Wales, Victoria, Queensland, Tasmania, South Australia and New Zealand along with an emerging metropolitan presence. The financial year 2018 was a milestone year for Propel, with a key highlight being the companyâs successful debut on the ASX on 23rd November 2017.

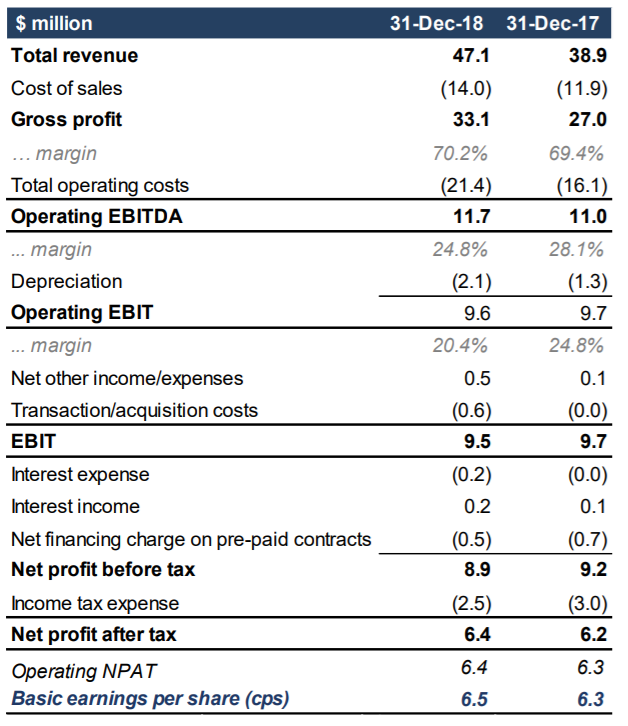

On the financial front as well, the company has been producing encouraging financial results. For the half-year ended 31 December 2018, the company earned a revenue of $47,095,000, which was 20.9% higher than the previous corresponding period (pcp). Further, the company reported operating earnings after tax of $6,352,000, which was 21.8% higher than pcp.

The profit for the half-year period increased by 100% to $6,421,000 as compared to the pcp. The company reported a gross profit margin of 70.2%, which was 0.8% higher than 1H FY18, due to the financial contributions of recent acquisitions and price increases.

The companyâs operating EBITDA (Earnings before interest, tax, depreciation and amortization) increased 6.4% on 1H FY18, primarily on the back of impact of six acquisitions completed in FY18 and 1H FY19. As at 31st December 2018, the company had net cash of $10.3 million of cash with no senior debt.

Income Statement (Source: Company Reports)

At the end of the half year period, the company had a strong and conservative balance sheet with further debt capacity. Together, with the positive operating cash flows and freehold assets, the company carries enough financial flexibility to support future dividends and growth initiatives.

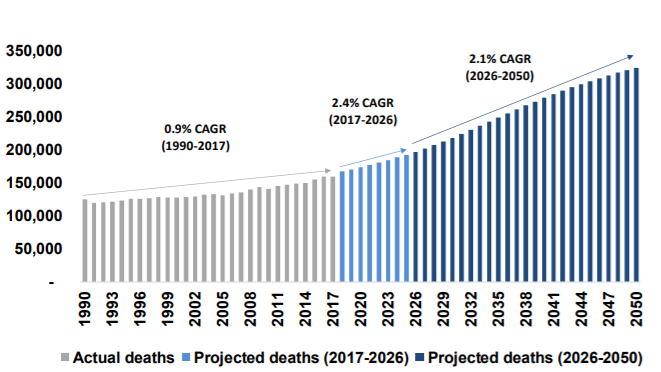

Surprisingly, a number of deaths is the most significant driver of revenue in the death care industry. Death volumes in Australia have increased by 0.9% per annum between 1990 and 2017. This is expected to increase even further by 2.4% per annum from 2017 to 2026 and 2.1% from 2026 to 2050.

Number of deaths in Australia (Source: Company Reports)

Demand for death care services is expected to grow in Australia and New Zealand as a result of increasing death volumes due to population growth and ageing of the âbaby boomersâ.

On the stock performance front, the companyâs stock has provided a return of 29.88% in the last six months as on 25th June 2019. With the recent expansion through acquisitions and strong financial and stock performance in the recent past, Propel Funeral Partners stands tall from a defensive angle.

At the time of writing, i.e. on 26th June 2019, AEST 01:30 PM, the companyâs stock was trading at a price of $3.200, with a market capitalisation of circa $321.14 million. The stock is trading at a PE multiple of 11.500x.

InvoCare Limited (ASX:IVC)

International funeral services provider, InvoCare Limited (ASX: IVC) showed significant progress in implementing both of its growth strategies (Protect & Grow and Regional Acquisitions) in 2018, despite soft market conditions, which impacted the operational performance of the business.

As part of Protect & Grow, the company is spending a net $200 million across three core streams â Network and Brand Optimisation (NBO), People and Culture and Operational Efficiencies. The company also invested $70.6 million in the last year to acquire 11 businesses to both in-fill its core markets (Adelaide and Auckland) and extend its market coverage into new regional areas. The rationale for 11 acquisitions has been driven by the detailed demographic and market analysis undertaken through the companyâs Protect & Grow program. This work identified a shift in the demographic profile in metropolitan areas, where people are taking either a âseaâ or âtreeâ change in retirement. By securing high quality businesses in high growth markets, the company has demonstrated its commitment to creating long term value.

In the month of March 2019, the company announced an $85 million fundraising, a step taken by the company after meeting with many of its shareholders post the full year results, where there was a clear preference for InvoCare to continue with the strong momentum generated by both growth strategies in 2018. The company was conscious of the need to balance surety of securing capital at a minimal discount and introducing high quality new investors, ensuring that the existing investors were not unduly diluted.

In FY18, the companyâs operating EBITDA results decreased 4.3% over the previous corresponding period (PCP). Further, the companyâs operating earnings after tax decreased by 22.1% on the PCP, reflecting increased depreciation and interest stemming from the Protect & Grow and acquisition investments.

The FY18 net profit after tax was down 57.7% on the PCP to $41.2 million, primarily from the impact of the mark-to-market valuation of prepaid contracts in 2017, which included a significant gain due to property revaluations.

The companyâs growth strategies ensure that the company is building on its core business and fulfilling the changing needs of customers for a contemporary funeral service, through investing in locations, brands, systems and people to deliver the highest level of customer service.

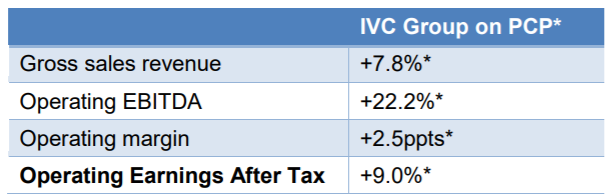

Recently, for the quarter ended 31st March 2019, the company reported a growth of 7.8% in its gross sales revenue and 22.2% growth in its operating EBITDA as compared to the previous comparable period. The companyâs operating earnings after tax increased by 9% as compared to the previous comparable period.

Results summary for the quarter ended 31 March 2019 (Source: Company Reports)

Due to a significance on IVC operating results and the inability to accurately forecast the severity of the flu season, IVC has not yet provided a full year forecast. On the stock performance front, the companyâs stock has provided a return of 51.87% in the last six months as on 25th June 2019. With the recent strong financial and stock performance of the company, Invocare Limited can be considered as a good stock from a defensive angle.

At the time of writing, i.e. on 26th June 2019, AEST 2:00 PM, the companyâs stock was trading at a price of $16.225, with a market capitalisation of circa $1.89 billion. The stock is trading at a PE multiple of 42.910x, with an annual dividend yield of 2.28%.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.