Adelaide Brighton Limited (ASX: ABC) is an ASX-listed material sector company focused on the production of construction material and lime.

In an announcement dated 31 July 2019, Adelaide downgraded its earnings guidance as it now expects the groupâs underlying net profit after tax to be in the range of $120-130 million for the year ended 31 December 2019. This marks an estimated reduction of over 30% on the prior yearâs NPAT of $190.1 million, extremely lower than the companyâs initial guidance of 10-15% projected decline.

The company blamed the slump in residential and civil construction markets for this revision in earnings guidance. Adelaide further explained that its weak earnings outlook is based on the competitive pressure in Queensland and South Australia combined with the sustainable increase in raw material costs and one-off shipping costs associated with cancellation of import orders.

Initially, Adelaide staged positive outlook stating that it expects a broadly stable demand environment in construction materials and lime in 2019. The group forecasted the decline in residential sector to get largely offset by the growth in non-residential engineering and infrastructure demand.

Today, the company also informed that its management has been undertaking a balance sheet review ahead of reporting interim results, and it is expected that the review will result in a non-cash impairment of no more than $100 million (pre-tax) for the six months ended 30 June 2019.

This amount reflecting no more than 5% of Adelaide Brightonâs total assets will have no impact on the companyâs operational performance or the underlying profit of the business, said Adelaide.

Dividend Cut- ABCâs Board has also decided not to declare any interim dividend for the six months ended 30 June 2019 in order to conserve capital and maintain flexibility in the companyâs balance sheet to pursue near-term growth opportunities. The priority list of the company somewhat looks like this:

- Maintain market share;

- Strengthen the balance sheet;

- Prudently manage capital spend;

- Contain costs and right size the business to improve performance; and

- Pursue future growth and investment opportunities

Singing of Supply Contract

In May this year, Adelaide inked a contract with OZ Minerals Limited (ASX:OZL) through its subsidiary Adelaide Brighton Cement Ltd for the continuation of cement supply to the OZ Minerals Prominent Hill Operation.

The contract has been extended for a period of five years under which Adelaide Brighton will also supply aggregate and sand from its Sellicks Hill Quarry and Price sand operation, in addition to the supply of cement and auxiliary logistics services.

Fiscal 2018 financial results

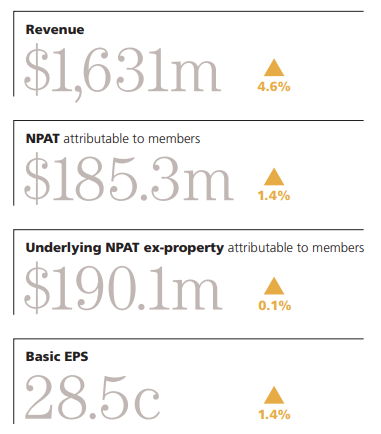

In 2018, Adelaide reported robust top-line growth with revenue increasing 4.6% to record $1,630.6 million on the back of favourable demand environment for lime and construction materials. Sales of concrete improved 14% compared to 2017 and Aggregate volumes increased 10%, assisted by the strong east coast markets and acquisitions. Overall cement and clinker sales volume increased 1.1% compared to 2017.

However, its underlying EBIT, which disregards one-off items, declined 5.7% to $273.5 million, reflecting softer cement and lime earnings and lower property profits, not fully offset by improved concrete, aggregates and joint venture earnings. Underlying EBIT margins declined from 18.5% to 16.8% in 2018, reflecting reduced cement and lime earnings and lower property profits more than offsetting earnings growth in concrete, aggregates and joint ventures.

Snapshot of Adelaideâs 2018 financial performance (Source: Companyâs Annual Report)

Earnings before interest and tax (EBIT) decreased 0.8% from the prior year to $265.4 million on an EBIT margin of 16.3%. Net finance costs increased from $12.1 million to $14.4 million in 2018 due to higher market interest rates and higher average borrowings.

Adelaideâs 2018 NPAT increased 1.4%, to $185.3 million while underlying NPAT of $191.0 million was down 3.7% on 2017. Underlying NPAT excluded restructuring and transaction cost as well as property profits.

A final ordinary dividend of 11.0 cents per share and final special dividend of 4.0 cents per share were declared for 2018, bringing total dividends declared to 28.0 cents per share, fully franked, for 2018, representing a payout ratio of 98.2%.

In 2018, Adelaide incurred capital expenditure on 27 projects above $1 million in value, comprising stay in business capex of $55 million, development projects of $58 million and acquisitions of $2 million. Proceeds from the sale of assets were $5.3 million, a decline of $12.4 million on 2017, driven by the reduced property sales. The net debt to book equity gearing ratio was 34.1% at 31 December 2018.

On the strategic front, the company aims to deliver against its long-term growth strategy of cost reduction and operational improvement; growth of the lime business and vertical integration opportunities into downstream aggregates, concrete, logistics and masonry businesses.

In 2018 Annual Report, Adelaide asserted that âConstruction demand in east coast markets is expected to remain healthy, with stable demand in Western Australia and the Northern Territory. Volumes in South Australia are likely to be assisted by demand from projects and mining. While variation in sector demand is likely, overall, Adelaide Brightonâs east coast markets are anticipated to remain at healthy levels in 2019.â

But now in the middle of 2019, the company is realising the negative impact on its earnings given the softening volumes in Victoria that reflects the massive meltdown of the Australian housing market. Adelaide reported that there has been further softening of demand for construction materials contrary to the favourable demand environment last year that led to the strongest construction markets in New South Wales and Victoria in 2018.

Stock Performance

On the news of downgraded guidance, ABC stock price crashed 18.056% to close at $3.540 on 31 July 2019. The stock last traded at a price to earnings multiple of 15.160x with a market capitalisation of $2.82 billion.

Over the past 12 months, the stock has declined by 36.06% including a negative price change of 4.63% recorded over the past six months.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.