Mining has been a significant contributor to the Australian economy in terms of employment, royalty payments and export income. It encompasses large quantities of minerals and resources, including iron ore, nickel, copper, aluminium, gold, silver, uranium and many more.

Now, let us have a look at the recent updates from 3 ASX-listed stocks in the sector.

Syrah Resources Limited (ASX:SYR)

Syrah Resources Limited (ASX: SYR) is an industrial minerals and technology company engages in THE development of the Balama Graphite Project in Mozambique. The company recently completed its fully underwritten 1-for-5 pro rata accelerated non-renounceable entitlement offer. The offer size amounted to $55.8 million. The institutional component of the offer raised approximately $25.1 million and the retail component raised approximately $30.7 million.

In another recent announcement, the company updated that Vanguard Group became a substantial shareholder of SYR, with 5.106% of the voting power.

Sales Agreement: The company entered into an agreement with Gredmann Group in June for sales into China. Balama Graphite Operation will undertake a monthly supply of 9,000 tonnes of fines natural graphite under the agreement. The agreement will continue until December 2021 and will include a total supply of 279,000 tonnes. The company aims to boost sales in China through Gredmannâs strong presence in the country.

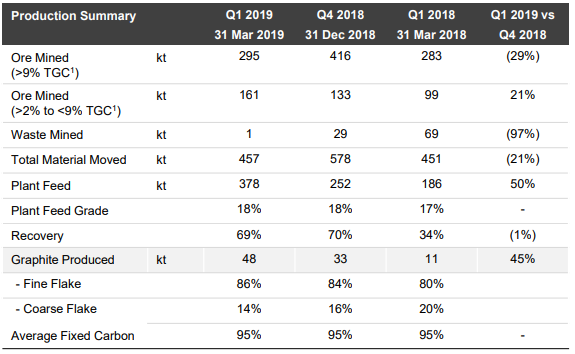

Q2 2019 Forecast: Recently, the company provided an update on the expected results for Q2 2019. Production in the quarter is expected to be in the range of 45kt to 50kt as compared to 48kt in Q1 2019. Graphite recovery and product split are expected to be almost similar to Q1 2019 at 69% and 86% fines to 14% coarse flake, respectively. Results from the production improvement plan are skewed towards the third quarter.

Shipped sales volume for the quarter is forecasted to be approximately 50kt as compared to 48kt in the first quarter of 2019. The weighted average price for the second quarter sales to date is $466 per tonne as compared to US$469 per tonne in Q1. Cash at the end of the quarter is expected to be around US$43 million.

Highlights of March Quarter: During the quarter, production from Balama Graphite Operation totalled to 48kt, up 45% on the previous quarter. The production exceeded the guidance range of 45kt â 50kt. The company achieved record production of 19kt in the month of March due to increased operational stability on the back of recovery increases and improvements in equipment management. During the quarter, demand for graphite continued to be strongest from China due to robust battery segment demand. Cash at the end of the quarter amounted to US$62.4 million.

Production Summary (Source: Company Reports)

The stock of the company at market close was trading at a price of $0.980, down 4.854%, with a market cap of $386.79 million on 11th July 2019. Over a period of one month, the stock has generated a return of 0.61%.

Whitehaven Coal Limited (ASX:WHC)

Whitehaven Coal Limited (ASX: WHC) is primarily engaged in the development and operation of coal mines in New South Wales.

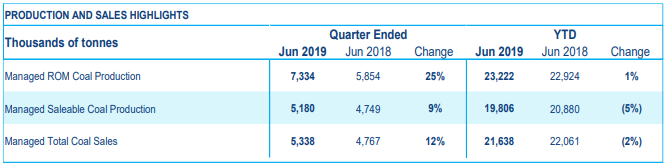

Highlights of June Quarter: The company recently released the June quarter production report. During the quarter, saleable coal production stood at 5.2Mt, up 9% on the prior corresponding period. Coal sales during the period stood at 5.3Mt, up 12% on the prior corresponding period. The company witnessed a strong finish to the year with ROM coal production of 7.3Mt in the quarter, reporting an increase of 25% on pcp. ROM coal production during the March quarter was reported at around 4.9Mt. ROM coal production for the year was reported at 23.2Mt that exceeded the full year guidance.

Production and Sales Highlights (Source: Company Reports)

Production and Sales Highlights (Source: Company Reports)

The company reported a record coal production of 11.7Mt from Maules Creek, up 7% on the prior corresponding period. The strong performance was reported by Narrabri with the production of 1.9Mt ROM coal for the quarter and 6.4Mt for the full year. This exceeded the guidance by a wide margin.

During the quarter, the safety outcome for the group improved significantly with TRIFR (total recordable injury frequency rate) falling from 8.3 at the end of March to 6.16 at the end of June. Another milestone achieved during the quarter included the declaration of the Winchester South Project as a Coordinated Project by the Queensland Coordinator-General, which now allow the assessment of the project by the government by way of an Environmental Impact Statement.

Thermal and Metallurgical Coal Outlook: Demand for thermal coal has been impacted by slowing world economic growth due to the trade tensions between the United States and China. The demand was also impacted by import restrictions from China. Moreover, the decline in gas prices in Europe led to a shift in demand from coal to gas. Seaborne coal supply from Australia, Russia and Indonesia increased Y-o-Y owing to good weather and good prices. With the softening of prices in the first half of 2019, the market is expected to rebalance as high cost producers moderate production. The outlook for metallurgical coal is healthy with steel production holding up well in China, India, Japan and several other countries.

The stock of the company at market close was trading at $3.830, up 4.932%, with a market cap of $3.75 billion on 11th July 2019. The stock has generated a negative return of 4.70% over a period of one month.

OZ Minerals Limited (ASX:OZL)

OZ Minerals Limited (ASX: OZL) is engaged in the mining and processing of ore containing copper, gold and silver. The company is also involved in the exploration activities and development of mining projects.

The company recently provided an update on the Brazilian mining assets acquired for ~$430 million.

In the Carajas province, the future of the Antas mine is considered to be limited as suggested by the mining studies and updated mineral resource estimation. The mine is expected to generate positive cash flows over the remainder of its life. The company has planned Antas pit closure in 2021. In addition, Pedra Branca ore trucking is expected to start in mid-2021.

Gurupi Province was strengthened after the completion of CentroGold pre-feasibility study, showcasing it as a 10-year open pit operation. Average annual gold production is expected to be in the range of 100koz to 120koz at an expected All-In Sustaining Cost of ~US$640/oz. Construction costs are estimated to be around US$155 million at a project NPV of approximately US$200 million.

Outlook: In Brazil, the company is confident on the capacity of the assets to add value for relatively modest capital outlay. The company expects to maintain a strong sustainable position in each province.

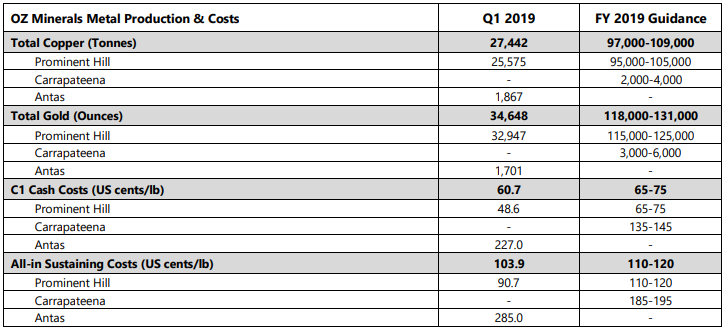

Q1 2019 Highlights: During the quarter, the company reported total copper production of 27,442 tonnes, with FY19 guidance in the range of 97,000 to 109,000 tonnes. The total gold production during the quarter was reported at 34,648 ounces with FY19 guidance in the range of 118,000 to 131,000 ounces. C1 cash costs during the period amounted to 60.7 cents/lb. Full year guidance was provided in the range of 65 to 75 cents/lb. All-in-Sustaining costs amounted to 103.9 cents/lb with a full year guidance in the range of 110 to 120 cents/lb.

Production and Cost Summary (Source: Company Reports)

Production and Cost Summary (Source: Company Reports)

The company reported unaudited net revenues of circa $1,115 million for 2018. Cash balance at the end of the period stood at $505 million.

The stock of the company at market close was currently trading at a price of $9.850, up 0.819%, with a market cap of $3.16 billion on 11th July 2019. The stock has generated a return of 5.05% over a period of one month.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.