A global mobile entertainment and digital media company, Crowd Media Holdings Limited (ASX: CM8) has been transitioning from a product-centric company to a platform company with an emphasis on marketing, predominately targeting millennials through technology. The company, at the right time, recognised the growing opportunities in the digital media space, hence this transition transpired. The increased focus on growing digital media space led the company to change its name to Crowd Media Holdings Limited from Crowd Mobile Ltd.

The company is focused on leveraging its technology and social media platforms to generate revenues by providing its advertiser clients market access to an audience, primarily millennials and Generation Z.

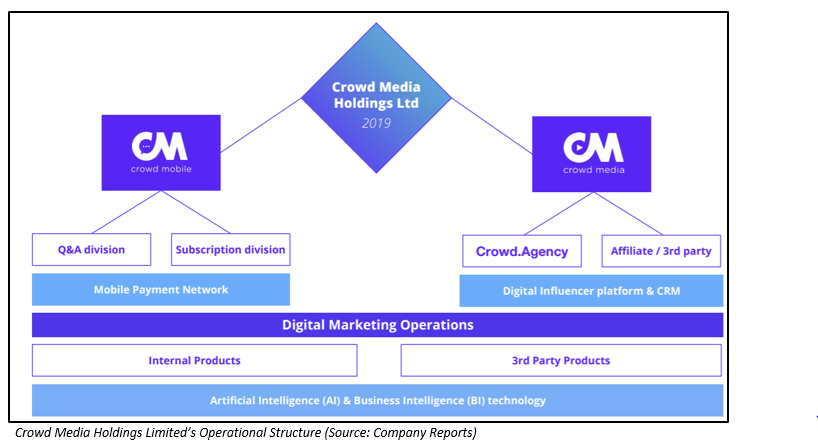

The company has two primary divisions, namely Mobile Division and a Digital Marketing division. The mobile division is primarily involved in the production of content, including apps, music, games, etc, whereas the companyâs digital marketing division offers branded content to millennial and Generation Z markets.

Crowd Media Division

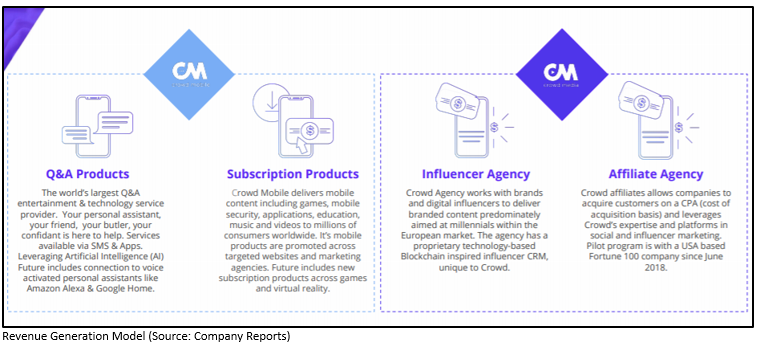

The companyâs Crowd Media division generates revenue by delivering globally competitive social media and digital influencer campaigns to its clients. The growing digital influencer sector has been the focal point for the division, creating a competitive advantage for the company.

The companyâs Crowd Media division is continuing the strong growth trajectory with FY19 expected revenues of $1.7 million, up 240% (FY18 $0.5 million). The division recently executed a pilot agreement with one of the largest digital wealth companies in Europe, Moneyfarm, under which, the division will help Moneyfarm to promote its investment services through the Companyâs proven digital influencer strategy. To better reflect the shifting focus of Crowd Media to the large and growing digital influencer and social media marketing sector, the company has also launched a revamped media kit.

The Crowd Media agency division works with brands and digital influencers and Crowd Affiliates works with companies to acquire customers on a cost per acquisition basis (CPA). The division has been running a pilot program with a US-based Fortune 100 company since July 2018. Crowd Mediaâs strong performance has been achieved by accelerating its ability to capture global growth opportunities in the digital influencer market space, leveraging the global distribution and expertise it has built up in the past six years in social media marketing with the Q&A division.

Crowd Media division more than doubled its entire FY18 revenue in the first half of FY19. In FY18, Crowd Media revenues were $0.5 million from a zero base and the company reported $1.3 million in revenues for first six months of FY19, up 160% compared to the same period last year. Crowd Media has identified a number of verticals, including Travel, Lifestyle/Fashion, Fintech, Cannabis/CBD Oils, eSports and gaming as targets for further client growth.

Till now, the companyâs media division has worked with over 10,000 digital influencers worldwide.

Mobile Division: Q&A and Subscription Business

Q&A and Subscription businesses are part of the companyâs mobile division. The company is currently a leading provider of Q&A entertainment and technology services; and via its Subscription Products, the company delivers mobile content, including games, mobile security, applications to millions of its consumers.

It expected that the Q&A division performance will further improve down the line due to the launch of its products in the new countries like Asia and Latin America. Further, the company will reap the benefits of improved margins due to Artificial Intelligence and a soon to be launched new Q&A app in the USA market while reducing its operating expenses within the division at the same time.

The Q&A division continues to test product pivots, leveraging its proprietary Artificial Intelligence (AI) technology. AI is now responsible for answering more than 60% of all questions, which will help improve operating margins.

The companyâs subscription business is currently focused on executing multiple new products and market opportunities in an attempt to return the division to a growth profile.

The Q&A division ended FY18 with revenues of $24.7 million while the Subscription division delivered revenues of $13.3 million. It is expected that the Q&A and Subscription division will generate revenues of around $23 million in FY19.

The company has continued to partner with telecommunications companies all over the world, giving them access to their billing platforms and allowing the rollout of its mobile payment technology.

The companyâs mobile division is currently operating in more than 60 countries and 30 languages.

Update on Strategic Review

Following the strategic review and the expense reduction program in the first half of FY19, the company implemented a range of aggressive cost-cutting measures, which will result in an estimated annualised cost savings of $3.5 million in FY19. The company is implementing these cost-saving measures with the objective of moving the company back to profitability (effective this month), as stated in various ASX releases.

The company has already reduced $1.4 mn in annualised costs which is related to the employment costs in the recent redundancy round.

Update on Convertible Securities Agreement with Obsidian Global Partners

Recently, the company entered in a Convertible Securities Agreement with Obsidian Global Partners, LLC as per which investor was supposed to invest up to $1.5 million across two tranches and in return the company had to issue convertible notes.

The company has now discovered an administrative error in the agreement and realised that as a consequence it has issued lesser number of convertible notes. In lieu of this, it has issued a further 877 convertible notes with a face value of US$120 each. The aggregate number of convertible notes issued to the investors is 5,259 convertible notes, pursuant to which, the company has raised $750,000.

Stock Performance: In the last three months, the companyâs stock has provided a return of 58.33% as on 2nd July 2019. At market close on 3rd July 2019, CM8âs stock was trading at a price of $0.017 with a market capitalisation of circa $4.58 million.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. The above article is sponsored but NOT a solicitation or recommendation to buy, sell or hold the stock of the company (or companies) under discussion. We are neither licensed nor qualified to provide investment advice through this platform.