ReadCloud Limited (ASX: RCL) is engaged in delivering eLearning software solutions, including eBooks, to schools within Australia. The company has distribution agreements for digital content with more than 25 of the worldâs leading publishers.

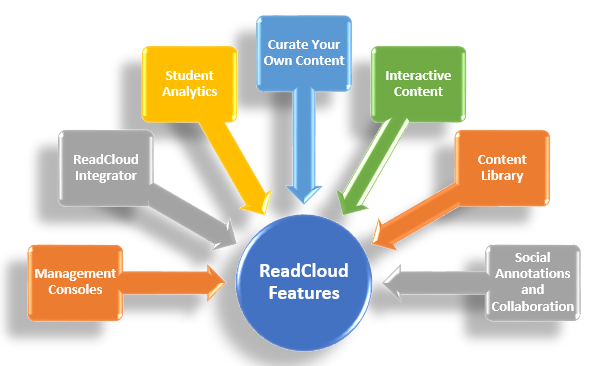

ReadCloud can provide the Australian school curriculum on a single platform in digital form, across all states. The proprietary eBook reader of ReadCloud offers digital content to teachers and students with substantial functionality. The eBook reader enables students and teachers to collaborate by sharing notes, questions, videos and weblinks directly inside the eBooks. The reader improves the learning outcomes as the eBook can be turned into a place for discussion, collaboration and social learning.

ReadCloudâs subsidiary Australian Institute of Education and Training (AIET) delivers digital vocational Education and Training (VET) course materials and services to schools. In November 2018, ReadCloud declared acquisition of AIET for up to $2.95 million, to be satisfied via a combination of cash and RCL shares. The consideration was to be paid in up to three tranches. The company paid the initial consideration comprising $350,000 cash and the issue of 250,000 RCL shares in November itself.

ReadCloudâs subsidiary Australian Institute of Education and Training (AIET) delivers digital vocational Education and Training (VET) course materials and services to schools. In November 2018, ReadCloud declared acquisition of AIET for up to $2.95 million, to be satisfied via a combination of cash and RCL shares. The consideration was to be paid in up to three tranches. The company paid the initial consideration comprising $350,000 cash and the issue of 250,000 RCL shares in November itself.

The company recently informed that AIET has generated revenue over $900,000 for FY19 (year to date), comfortably exceeding the performance hurdle set for the payment of the first tranche. Thereby, ReadCloud has paid the first tranche of deferred consideration comprising $50,000 cash and the issue of 1,000,000 RCL shares.

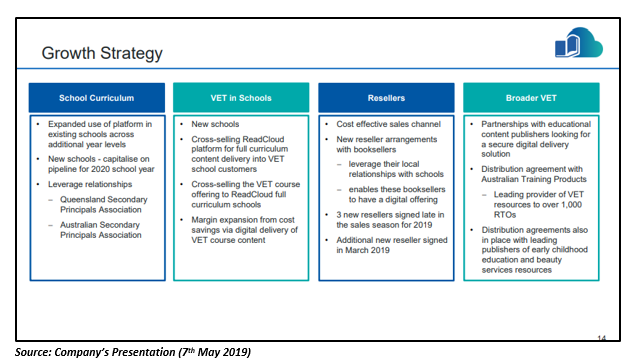

Below are the anticipated synergies realised from the acquisition:

- The cross-selling of VET courses to full curriculum schools and selling the full curriculum ReadCloud platform into VET schools.

- There will be a significant printing and handling cost savings in the digitisation and delivery of VET course materials via the ReadCloud platform.

ReadCloud has made a significant investment in the transformation of AIETâs course materials and processes into a digital end-to-end enrolment and learning resource delivery platform. The VET segment is expected to record almost all of its revenue in 2H19.

ReadCloudâs Outlook

ReadCloudâs Outlook

- ReadCloud forecasts its 2H19 revenue to be more than double the revenue of FY18 ($2.1m), exceeding the revenue of $2.3 million in 1H19.

- Many of the contacted schools have decided to defer digitisation to school year 2020 as the schools are indulged in preparing internally for a digitally delivered curriculum.

- The company expects its pipeline for 2020 to be stronger than ever.

- ReadCloud targets to leverage new partnership agreement with ATP.

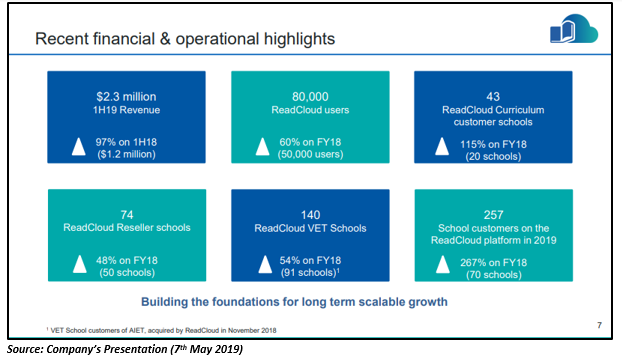

The Operational Update of the company was released in the first week of April. The FY19 onboarding season of ReadCloud was better than any previous years, with existing and new customers providing positive feedback around the new 2019 ReadCloud App suite and services provided. ReadCloud reported an increase in its school customer numbers for the school year 2019 in comparison to FY18:

- A 267 per cent rise in the schools using the ReadCloud platform (including VET courses).

- Direct school customers using ReadCloud improved by 115 per cent.

- A 48 per cent increase in the Reseller schools using ReadCloud.

- The schools signed by AIET grew 54 per cent.

Recently, ReadCloud entered into a three-year exclusive Strategic Distribution Agreement with Australian Training Products (âATPâ). The agreement involves a commitment by ATP in using ReadCloud exclusively for three years. ATP will be using ReadCloud as its eReading delivery platform and digital content encryption for its customer base.

Recently, ReadCloud entered into a three-year exclusive Strategic Distribution Agreement with Australian Training Products (âATPâ). The agreement involves a commitment by ATP in using ReadCloud exclusively for three years. ATP will be using ReadCloud as its eReading delivery platform and digital content encryption for its customer base.

Let us take a look at the financial performance of the company during March 2019 quarter:

The company received 1.55 million dollars from customers in the March 2019 quarter, which was a 131 per cent increase over the March 2018 quarter. The company expects its June quarter cash receipts from customers to surpass the March quarter.

The companyâs stock last traded at A$0.340 (as on 23 May 2019) with a YTD return of 13.33 per cent.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.