Collins Foods (ASX: CKF) is involved in the operations, management and administration of restaurants, currently comprising three restaurant brands, namely KFC, Taco Bell and Sizzler. The KFC and Taco Bell brands are two of the worldâs largest restaurant chains and are owned globally by Yum!. In Australia, the group is the largest franchisee of KFC restaurants and currently the only franchise of Taco Bell restaurants. In the casual dining market, Sizzler competes with other casual dining concepts as well as taverns and clubs, fast food and home cooking.

The strong cash flow has been supporting the strategic growth of the company. Capital expenditure has also risen substantially in the last five years reflecting growth in restaurant base.

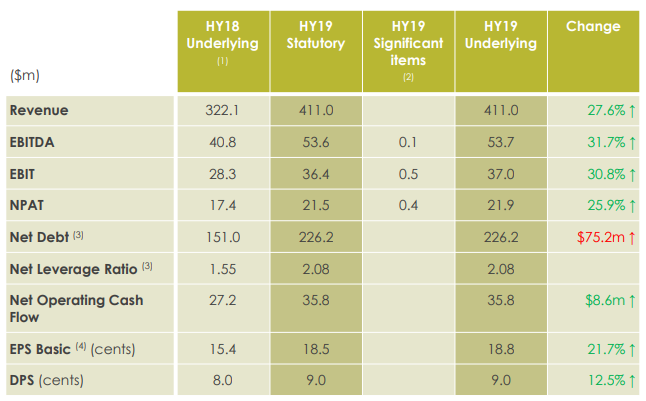

Operating and Financial Review of 1H FY19 Results: The group reported a statutory net profit of $21.5 million in H1 FY19, up 69.0% as compared to $12.7 million in 1H FY18. This represented basic EPS (earnings per share) of 18.48 cents in the period under consideration, higher than 11.31 cents in 1H FY18. Underlying net profit at $21.9 million represented a rise of $4.5 million or 25.9% compared to the underlying net profit of $17.4 million reported in the previous corresponding period.

Revenues for the half-year recorded a growth of 27.6% (pcp) to $411.0 million. Revenues in the domestic KFC restaurants segment recorded a higher pcp growth of ~22% to $330.0 million, whereas Sizzler restaurants segment recorded a 7.6% (pcp) fall in statutory revenues to $22.2 million. Variation in the revenues reported by the operating segments was largely on the back of differential in the restaurant numbers. Overall, revenue growth combined with the disciplined business controls resulted in a healthy underlying EBITDA of $53.7 million, 31.7% higher than the previous corresponding period.

Strong growth delivered across key financial metrics (Source: Company Reports)

Strong growth delivered across key financial metrics (Source: Company Reports)

The net cash flow from operations of $35.8 million was higher as compared to the prior comparable period. Higher cash flow can be attributed to the growth in cash generated by the KFC restaurant segment. Cash flow from investing activities witnessed a net outflow of $23.9 million, which was due to completion of and payment for the remaining three KFC restaurants in South Australia, along with further CapEx in the existing network. The net cash outflow from financing activities of $10.5 million reflected the groupâs dividend payment. Overall, cash and equivalents for the period under consideration were slightly higher on the pcp basis. The total debt on the balance sheet at the end of 14th October 2018, stood at $331.3 million, with undrawn facilities of $42.4 million. Debt (excluding interest and net of cash and equivalents) stood at $226.2 million.

At the current market price of $8.00, the stock is trading at a price to earnings multiple of 22.57x. The stock is trading close to its 52-week high of $8.350. Analysing the historical price movement, the stock has appreciated 44.67% in the last one year. In the short-term, the stock gained 25% in the last three months. The annual dividend yield for the stock stands at 2.25%, with a market cap of $932.09 million as on 17th May 2019.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.