Western Australia ramped-up gas supply across the domestic market in 2019 through two projects, namely Wheatstone, with a total capacity of 205 terajoules per day, and Pluto, which included a 25 terajoule per day of domestic gas pipeline and ~ 15 terajoules per day, respectively.

Demand and Development

The commencement of the new projects supported the high demand for gas in WA, which remained the highest natural gas consumer and producer across all Australian state. From 2017-18, WA consumed about 644 petajoules of gas, which represented ~41 per cent of Australia’s total gas consumption during the period.

The high demand for gas in WA is predominately due to the high mining activity associated with the region, Western Australia currently tops the production of gold, copper, etc., and due to large power generation through gas-powered stations.

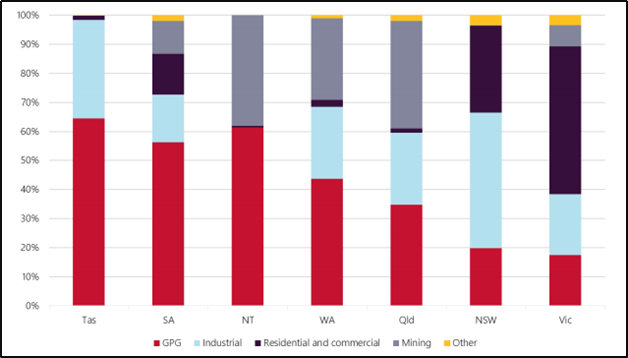

From 2017-18, gas-powered generation (or GPG) in WA accounted for 44 per cent of the overall gas consumption, while mining activities accounted for 28 per cent of the overall gas consumption, followed by industrial and minerals processing (25 per cent), residential and commercial (2 per cent), and other (1 per cent), respectively.

Gas Consumption Composition Across States During 2017-18 (Source: AEMO)

Whilst the demand for gas in WA is high, the year 2019 had witnessed a significant phase of development to support the domestic supply.

Santos Limited (ASX: STO) identified a gas reservoir in the Carnarvon basin-Corvus, Woodside Petroleum Limited (ASX: WPL) took the final investment decision (or FID) related to the development of the Pyxis Hub project, Strike Energy Limited (ASX: STX) and Warrego Energy Limited (ASX: WGO) discovered new gas at the Perth Basin; many such activities took place during 2019, which further supported the supply for high demand in WA.

While Australian oil and gas exploration companies played their part, the WA government also announced plans, such as the development of a micro-scale LNG plant with a production capacity of 10 tonnes a day, as part of an LNG Futures Facility in Kwinana.

Gas Consumption Trend

During 2018-19, large customers accounted for 86 per cent of the overall consumption, while small businesses and retail accounted for the rest. In large customers, 32 per cent remained from the minerals processing industry, 27 per cent remained from the mining sector, and 27 per cent remained from the electricity generation sector. These customers were supplied directly through the transmission network, such as of Dampier Bunbury Pipeline and Goldfields Gas Pipeline.

The retail distribution network accounted for 7 per cent of the overall consumption. However, the annual growth in customer numbers declined, or average usage per connection fell from the period of 2014 to 2019 amid increased efficiency of gas appliances, small household sizes, and penetration of alternative energy resources such as solar and wind.

Consumption Forecast From AEMO

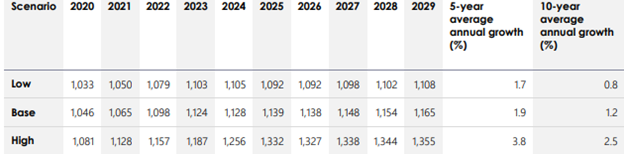

The energy market operator forecasted demand for gas across WA for the period of 2020 to 2029 under three scenarios; low, base, and high, with the base case being the standard.

AEMO anticipates the gas demand to grow at an average of 1.2 per cent in the base scenario amid demand growth in the mining sector. However, AEMO suggested that under all scenarios following demand-related assumption have been made;

- The mining and mineral processing sector would contribute ~ 62 terajoules of gas demand from 2020 to 2029.

- The South Flank project of the iron ore giant-BHP Group Limited (ASX: BHP) would commence on 2021, while the Koodaideri iron ore project of the top gunner-Rio Tinto Limited (ASX: RIO) would start its first production in late 2021.

- The global lithium chemical mammoth-Albemarle would commence its Kemerton lithium processing plant in 2021.

- Fortescue Metals Group Limited (ASX: FMG) would start stage 2 of its Iron Bridge magnetite processing project in mid-2022.

Also Read: Andrew Forrest-Iron Ore Magnet Racing towards Australia’s Richest Podium

While the above-stated assumptions are expected to increase the demand for gas in Western Australia, the following are assumption which would reduce the gas demand by 2.5 terajoules per day in the period of 2020-2029.

- The Agnew Gold Mine of global gold mining behemoth- Gold Field would shift to renewable energy microgrid in 2020.

- The biogas to hydrogen and graphite project of Hazer Group would reduce the existing gas consumption by ~ 2 terajoules at the beginning of the year 2020.

The gas demand growth projections for all the three scenarios are as below:

Source: AEMO

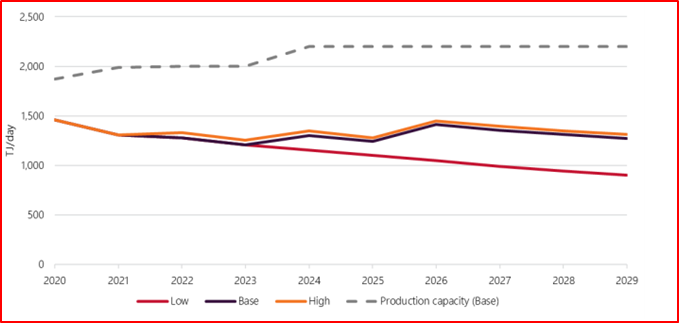

Supply Forecast From AEMO

The potential gas supply is estimated by the energy market operator to decline at an annual rate of 1.5 per cent or by 28 terajoules per day during the period of 2020 to 2029 due to reserve depletion at the existing gas producing facilities; however, AEMO also anticipates, that if developed, potential gas sources could further add 405 terajoules per day of supply.

Also Read: Assessing the Impact of Rising Oil Prices on the Domestic Gas Production

- Resources and Reserves

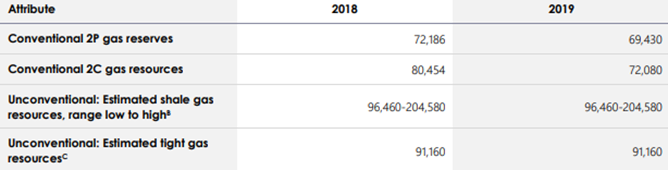

The conventional 2P (probable and Proven) gas reserves have declined by ~3.81 per cent from 72,186 in 2018 to stand at 69,430, and while gas reserves declined during the period, the 2C resources, which have the highest probability of getting converted into 2P reserves (subject to commercial or technical uncertainties impacting the likelihood), also declined by ~10.40 per cent from 80,454 in 2018 to stand at 72,080 in 2019.

Other estimates compiled by AEMO are as below:

Source: AEMO

While gas reserves and resources are declining across the production facilities, the lower gas prices amid fall in oil-linked contracts had kept the gas exploration under check across WA.

- Exploration Plunges

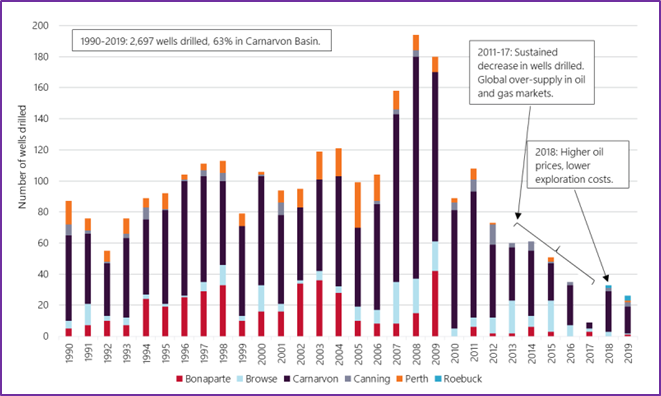

Till January 2019 to August 2019, only 26 wells were drilled, which remains significantly below the exploration in 2018, albeit, up from 2017 levels and the exploration has taken a deep hit since peaking in 2008.

Exploration and Number of Wells Drilled from 1990-2019 (Source: AEMO)

- Gas Supply Ahead

The development of potential reserves and resources would depend upon certain events, and the supply forecast from AEMO adopts following assumption;

- The prospective supply will increase if the domestic gas price surpasses the long-run production cost.

- The prospective supply will increase if the Asian LNG price surpasses the long-run production cost for LNG-linked projects.

However, even if the assumptions come true, the AEMO estimates the gas supply to remain below the nameplate capacity in all three scenarios.

To Know The Risk Associated With Gas Demand, Also Read: The Future of Energy Generation in Australia; Solar to Increase Three-Fold By 2024

Potential gas supply and production capacity Forecast (Source: AEMO)

Key Takeaways

- Western Australia ramped-up gas supply across the domestic market in 2019 amid higher demand from mineral processing, mining, and electricity generation sector.

- AEMO anticipates the gas demand to grow at an average of 1.2 per cent in the base scenario amid demand growth in the mining sector (subject to certain assumptions).

- The potential gas supply is estimated by the energy market operator to decline at an annual rate of 1.5 per cent or by 28 terajoules per day during the period of 2020 to 2029(subject to certain assumptions).