âPast teaches us not to repeat mistakes, however, whilst coming across a legit mistake; we shall accept the mistake in the first place and look out for best preventive measures for the times ahead.â

Westpac Banking Corporation (ASX: WBC)

During the trading session on 28 November 2019, shares of Westpac had lost 0.161% (at AEST 1:33 PM). And, its annual dividend yield reached 7.1%, according to data available on ASX.

Amongst the major banks, Westpac has been in the headlines of dailies in the country, following an investigation by the financial intelligence agency and regulator â AUSTRAC, which revealed substantial counts of non-complaint transactions.

Less than a week into the revelation, the market participants were made aware that the Group Chief Executive Officer is set to step down from the role, effective from 2 December 2019, via an exchange release on 26 November 2019.

The release stated that Mr Peter King, current Chief Financial Officer, is going to replace Mr Brian Hartzer in the capacity of acting CEO. Also, Mr Gary Thursby would be taking up the role of CFO.

In addition to this major shuffle, Mr Ewen Crouch has decided not to seek re-election at the upcoming Annual General Meeting of Westpac. And, Chairman of Westpac â Mr Lindsay Maxsted has preponed his retirement to the first half of next year.

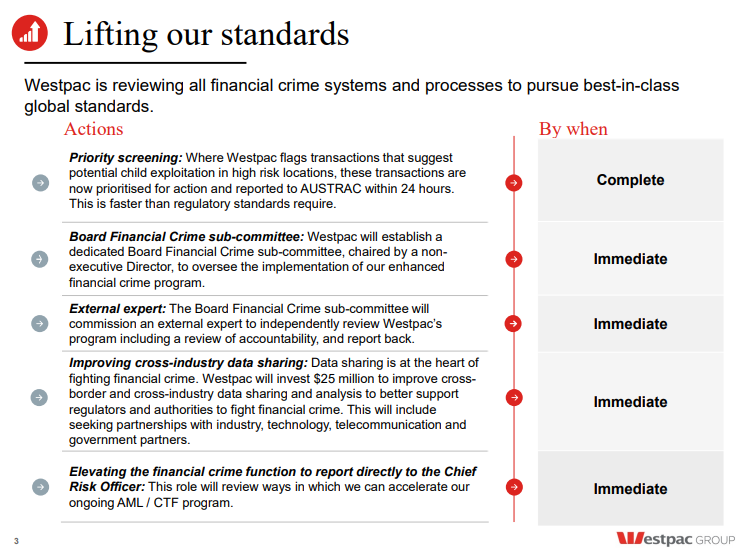

In a statement to exchange on 25 November 2019, Westpac said that it estimates to incur expenses of up to $80 million (pre-tax) in a comprehensive response plan released by the bank a day before.

Westpacâs Response Plan (Source: Company Announcement)

The response plan is intended to strengthen the existing system and other objectives, including commitments to enhance financial crime program, support industry initiatives, improve financial monitoring, provide additional support to the organisations engaged in eradicating child exploitation.

In response plan, the bank had completed a number of actions, including;

- fixing the non-reporting issue of IFTI cases on the relevant product,

- consolidation of various financial crime into a single group-wide platform,

- doubling the headcount engaged in financial crime to 750 people,

- sharing of Financial Crime Strategic Plan to AUSTRAC, and

- made changes to the leadership in financial crime and risk with numerous external appointments.

How has the bank performed in FY 2019?

At the year-end 30 September 2019, the bankâs gross loans to customers were $718,378 million compared to $712,504 million a year ago, and the provisions for expected credit losses/impairment charges on loans were $3.6 billion compared to $2.81 billion in the previous year.

In superannuation obligations, across all plans, the bank had net superannuation deficit of $335 million compared to net superannuation surplus of $64 million in the previous year. Additional break-up suggests that one superannuation plan was in a surplus and three were in superannuation deficit.

In FY 2019, the bank adopted two accounting standard AASB 9 and AASB 15, as a result, the comparative data have not been restated.

In consolidated terms, the bank generated an interest income $33.22 billion compared to $32.57 billion in the previous year, and the interest expense of the bank was $16.31 billion, resulting in a net interest income of $16.9 billion against $16.5 billion in the previous year.

In FY 2019, the trading income, net fee income and net wealth management and insurance income were down compared to the previous year. And, the trading income came down to $929 million against $945 million in the previous year, net fee income was $1,655 million compared to $2,424 million in the previous year, while net wealth management and insurance income came down to $1,029 million against $2,061 in the previous year.

The operating expenses amounted to $10.1 billion for the period against $9.56 billion in the previous year, and impairment charges were $794 million against $710 million in the previous year.

Net profit for the year was $6.79 billion compared to $8.09 billion in the previous year, and profit before income tax was $9.74 billion against $11.73 billion in the previous year. Basic earnings per ordinary share was 196.5 cents per share against 237.5 cents per share in the previous year.

Despite these headwinds, the bank declared dividends of 174 cents per share compared to 188 cents per share in the previous year, representing a dividend pay-out ratio of 88.83%.

What has damaged the performance of the bank?

A decrease of 16% or $1.31 billion in net profits over the previous year was credited to notable increases in provisions related to expected customer refunds, remediation payments, associated costs with remediation, and litigation. In addition to these, and wealth business reset had dragged the profits of the bank to lower territories.

In FY 2019, the bankâs increase in net interest income was due to reclassification of line fees from net fee income to net interest income, having an impact of $686 million. The impact of reclassification was partly offset by an increase in the order of $239 million in provisions related to refunds, payments, associated costs and litigation.

A similar reason was provided by the bank in relation to a decrease in net fee income. The bank said net wealth management and insurance income was decreased due to higher claims from severe weather conditions, cessation of grandfathered advice commissions, lower wealth management income, exit from Hastings business. In addition to these, the income was adversely impacted by provisions related to refunds, payments, associated costs and litigation.

In trading income, the bank has suffered fall in income on the back of a change in methodology for derivative valuation, which was offset by higher non-customer income.

Whatâs the outlook for FY 2020?

In its CEO letter in Annual Report 2019, Mr Hartzer had voiced out a conservative tone, recalling the sluggish economic situation in the country. He mentioned that economic outlook for the country remains weak, backed by global trade issues, weak real wages growth, the softer housing market, low interest rates and subdued economic activity; all of this led to a suppressed consumer confidence.

He also talked about the favourable circumstances, including targeted tax cuts, infrastructure investments, lower Australian dollar. In relation to banks, he said that the existing low interest rate environment presents challenging trading conditions for banks.

He mentioned that regulatory outcomes from the Royal Commission had impacted the financial services industry. And, the regulators across ANZ are conducting various reviews, including home loan pricing, remuneration, risk-weighted asset methodologies.

On 28 November 2019, WBC was trading at $24.77, down by 0.161% (at AEST 1:33 PM).

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.