Santos Limited (ASX: STO) is an ASX-listed energy pioneer and one of the substantial natural gas provider in the domestic market, which is currently experiencing a shortfall of natural gas amid booming LNG industry. The company owns and operates assets in Papua New Guinea, Western Australia and other regions in Australia.

To know more about the booming LNG industry, Do Read: Australia To Jostle Qatar for the LNG Crown; How Long Would the Reign Last?

In the status quo, Santos increased the 2025 production target by two-fold from the 2018âs output, and now the company would aim a production of 120 million barrels of oil equivalent by 2025.

The new target aimed by Santos is 20 per cent up against the 2018 production target of 100 million barrels of oil equivalent and also represents a cumulative annual growth rate in production of over 8 per cent to 2025.

Santos Reduces Production Guidance

The company reduced the production guidance for 2019 to 74-76 million barrels of oil equivalent as compared to the previous production guidance to 73-77 million barrels of oil equivalent, and also reduced the sales volume guidance to 93-95 million barrels of oil equivalent as compared to the previous guidance of 90-97 million barrels of oil equivalent.

Santos also slashed the upstream unit production cost for 2019 to $7.25 to $7.50 per barrel of oil equivalent from its previous guidance of $7.25 to $7.75 per barrel of oil equivalent, and also mentioned that the capital expenditure is anticipated to stand at $1 billion as compared to the previous guidance of $950 to $1,050 million.

2019 and 2020 Operating Guidance (Source: Companyâs Report)

Santos anticipates the production to increase in 2020 to stand between 79 to 87 million barrels of oil equivalent, of which 73 to 80 million barrels of oil equivalent would be from the companyâs base business excluding the ConocoPhillips acquisition.

The ConocoPhillips acquisition is expected by Santos to get complete in the first quarter of the year 2020, subject to a third-party consent and regulatory approvals, and upon the completion, the company anticipates a 25 per cent sell-down to SK E&S.

The interest of the company in Bayu-Undan and Darwin LNG would increase to 43.4 per cent to further add 6 to 7 million barrels of oil equivalent under the production chain.

Santos further forecasts the sustaining capital expenditure to stand at approx. $950 million in the base business, and major growth capital expenditure for Barossa, Dorado and PNG LNG expansion to stand at approx. $500 million.

Santos Growth Story

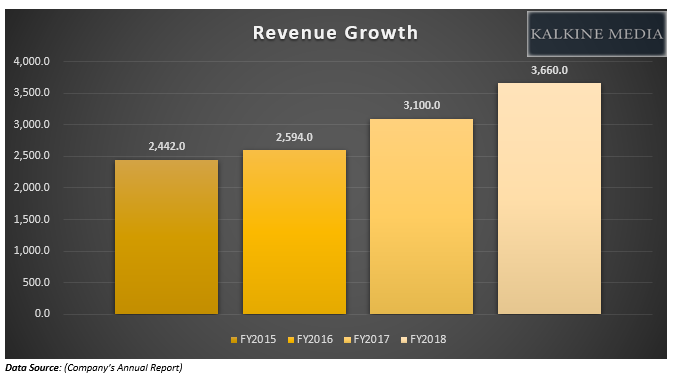

The revenue of the company witnessed a steady increase from the financial year 2015 to the financial year 2018. The total revenue of the company in FY2018 stood at USD 3,773 million, as against USD 2,442.0 million in FY2015, which marked an increase of 54.50 per cent.

The net profit of the company has contoured the same growth story, and the net profit after tax (or NPAT) of the company surged to stand at USD 630 million, against the FY2015 net loss of USD 1,953 million.

Santos Reducing Operating Cost and Increasing Profitability

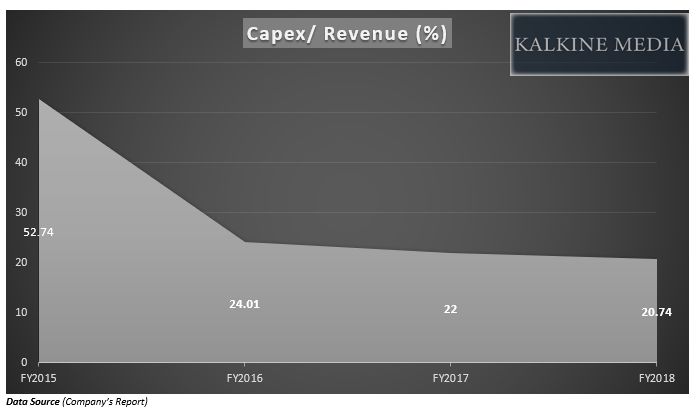

On the expenditure front, the company is significantly reducing its capital expenditure from FY2015 figures, when the capital expenditure of the company stood at USD 1,288 million. In FY2018, the capital expenditure of the company stood at USD 769 million, down by over 40 per cent against the FY2015.

The Capex by Revenue percentage of the company is also witnessing a continuous decline from FY2015, which further suggests, that the greater part of the capex is contributing to revenue.

Oil Production and Realised Average Price

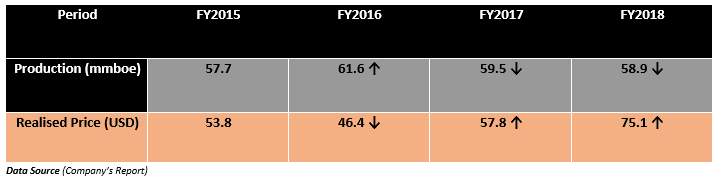

While the oil production of the company stood 100bps down in FY2018 against FY2017, Santos realised an average oil price of USD 75.1 in FY2018, which was almost 30 per cent higher as compared to the previous corresponding period.

STO Beating the Global Oil and Gas Explorers

STO and S&P Commodity Producers Oil & Gas Exploration & Production Index Total Returns (Source: Thomson Reuters)

On a YTD basis, the S&P Commodity Producers Oil & Gas Exploration & Production Index delivered a return of -3.78 per cent, while the stock of the company delivered a return of 47.70 per cent.

On the return counter, the stock delivered a return of 17.27 per cent over the last six months and a return of 8.93 per cent over the last three months. The yearly return of the company stands at 33.50 per cent.

On the price-performance counter, the stock of the company is currently surpassing the price performance of the industrial (ASX all ordinaries index) and sectoral (S&P/ASX 200 Energy) indices over the medium- to long-term.

STO Price Change Relative to Industrial and Sectoral Indices (Source: Thomson Reuters)

In a nutshell, the company anticipates the production and sales to decline slightly in FY2019; however, Santos mentioned in its report to the stakeholders that the production and sales would again surge in FY2020, and the historical figures of the company depict, that the company would ultimately deliver in its guidance and could provide shareholders with decent returns.

Another major factor going in favour of STO is the shortage of natural gas in the domestic market, and the company recently secured additional acreage from the local government to address the natural gas shortfall situation in Australia.

To know more about the additional acreage tendered to the company by the Queenslandâs government, Read: Domestic Supply Constraints in Queensland Opens More Acreage in Surat Basin for Senex and Santos.

Also, while the global oil & gas explorers are under pressure of the natural gas supply glut in the international market, the ASX-listed oil & gas explorers are under the league of benchmark outperformers.

To Know More, Do Read: ASX-Listed Oil & Gas Exploration Companies Beat Global Explorers with Superior Benchmark Adjusted Returns

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.