The S&P/ASX 200 Information Technology (Sector) was trading upward by 1.59% to 1,393.0 on 30 August 2019 (AEST 01:21 PM), while S&P/ASX 200 was trading at 6,595.9, up 1.34%. From 2 January 2019 till 29 August 2019, the S&P/ASX 200 Information Technology (Sector) provided a return of 22.83% and S&P/ASX 200 provided a return of 14.59%, highlighting that the IT index is outperforming its benchmark index. S&P/ASX 200 Information Technology (Sector) continued with an upward trend from 2 January 2019 till 30 July 2019 and then declined massively, reaching the level of 1248.10 on 16 August 2019. However, since then it has been trading upward.

Below discussed are four stocks catering to the technology sector. Two of the stocks, Link Administration Holdings Limited and NEXTDC Limited have updated the market with their performance during FY19, while Xero Limited has released its annual meeting 2019 presentation and PayGroup Limited entered an acquisition deal. Let us have a look at all these developments.

Link Administration Holdings Limited

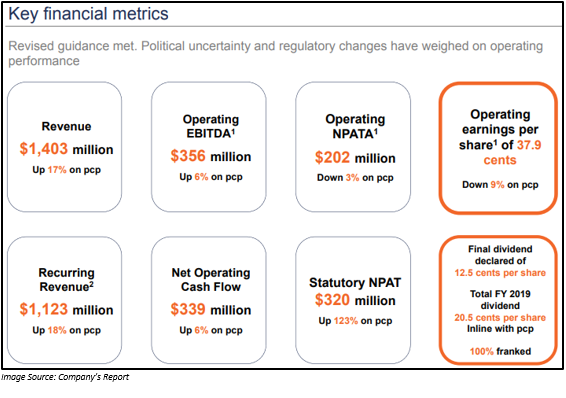

On 29 August 2019, Link Administration Holdings Limited (ASX:LNK), a market leading administrator of financial ownership data, released its FY2019 results for the year ended 30 June 2019.

FY2019 Highlights:

- Statutory NPAT of the company during the period was up by 123% to $320 million as compared to the previous corresponding period (pcp).

- Operating EBITDA increased by 6% to $356 million, while operating NPATA declined by 3% to $202 million.

- Revenue for the period increased by 17% to $1,403 million.

- Out of the total revenue, 80% was in the form of recurring revenue.

- Net operating cash flow increased by 6% to $339 million.

- The company boosted its stake in PEXA to 44.2%.

FY2019 Activities:

The company during FY2019 made significant progress towards the integration of Link Asset Services, resulting in the implementation of a global operating model and structure, which establishes a robust base for growth and efficiency gains. The company experienced several external headwinds during the years, which impacted its financial performance.

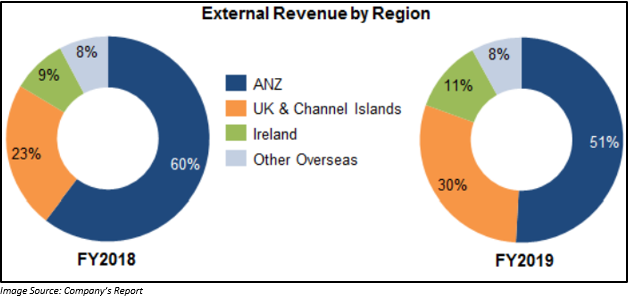

Its external revenue which was 60% from ANZ in FY2018 declined to 51% in FY2019.

Managing Director, John McMurtrie stated that even though the companyâs operational performance was impacted by several external factors, it was able to achieve a number of strategic objectives such as the renewal of its two of the largest clients AustralianSuper and Rest. The company also sold its business Corporate & Private Client Services (CPCS) in a deal worth £240 million, thereby providing flexibility to the balance sheet.

Outlook:

- In FY2020, operating EBITDA of the continuing business which excludes CPCS and LMS South Africa is expected to be stronger in the second half and would be in line with FY2019.

- RSS guidance for FY2020 - revenue would be in between $480 million and $500 million and operating EBITDA would be in the range of $60 million to $70 million

- Global transformation is expected to result in a $50 million annualised saving by FY2022 end.

- The company is expected on market share buyback of a maximum of 10%.

Stock Performance:

The shares of LNK have generated a negative YTD return of 19.85%. On 30 August 2019 (AEST 01:31 PM), the stock was trading at a price of A$5.410, up 0.745% from its previous close. LNK has a market cap of A$2.87 billion with ~ 533.95 million outstanding shares, PE ratio of 8.95x and an annual dividend yield of 3.82%.

NEXTDC Limited

NEXTDC Limited (ASX:NXT), an IT sector player engaged in the establishment, development and operation of data centre facilities, has released its FY2019 results for the period ended 30 June 2019.

FY2019 Highlights:

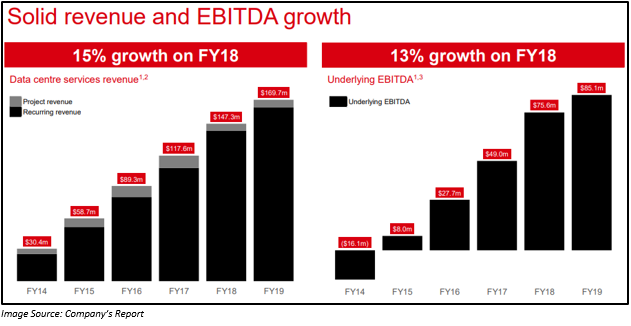

- Revenue increased by 15% to $179.3 million.

- The company made record new sales with an increased contracted utilisation of 31% to 52.5MW.

- Interconnections increased by 27% to 10,972, which resulted in 7.7% of the recurring revenue.

- Underlying EBITDA increased by 13% to $85.1 million

- Operating cash flow grew by 18% to $39.4 million

- Statutory loss after tax for FY2019 was $9.8 million, which was due to increased depreciation and interest costs after a record year of investment.

- The net cash position of the company by the FY2019 end was $399 million.

- The position of balance majorly supported by its $1.8 billion + total assets.

- Underlying capital expenses increased from $285 million in FY2018 to $378 million in FY2019.

- During the period, the company opened S2 to early customer access in the first half of FY2019 and the billing started in the second half.

- The stage 1 development of P2 is under progress.

- The expansion of B2 and M2âs additional capacity completed.

Outlook:

- Revenue is expected to be in the range of $200 million to $206 million.

- Underlying EBITDA is anticipated to lie between $100 million and $105 million.

- The capital expenditure in FY2020 is expected to be in between $280 million to $300 million

Stock Performance:

The shares of NXT have generated a YTD return 0.66%. On 30 August 2019 (AEST 01:32 PM), the stock was trading at a price of A$6.150, up 0.49% as compared to its previous closing price. NXT has a market cap of A$2.11 billion and ~ 344.52 million outstanding shares.

Xero Limited

Xero Limited (ASX:XRO), a provider of online accounting software for small-size enterprises, has released its Annual Meeting 2019 presentation. The agenda of the presentation was FY2019 overview and update.

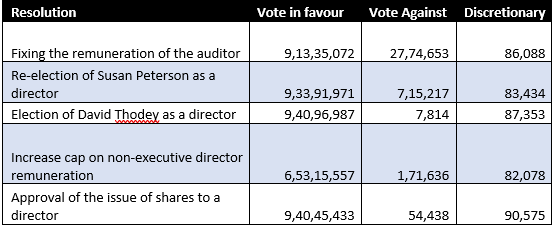

The presentation covered resolutions including fixing of remuneration of the auditor, with 96.96% of the members being in the favour of fixing the auditor remuneration, 2.95% against and the remaining 0.09% at discretionary.

Second resolution was related to the re-election of Susan Peterson as a director, with 99.15% casting their vote in the favour. Third resolution was for the election of David Thodey as a director, with 99.90% of the shareholders voted in the favour. Meanwhile, 99.61% of the shareholders voted in favour of increasing the cap on non-executive director remuneration, while 0.26% were against it. Lastly, 99.85% of the shareholders voted in favour of approval of the issue of shares to a director, Lee Hatton.

The company also highlighted that strong annual monthly recurring revenue of XRO in FY2019 of $154 million, increase in subscribers from 1,818,000 to 432,000 within 12 months, free cash flow of $6.5 million and 33% growth in the operating revenue to $552.8 million in constant currency unveil a strong business model of XRO.

The beauty of XROâs SaaS model is that it can generate long-term value. Moreover, it can acquire subscribers economically at scale, increase revenue per subscriber, boost gross margins as well as retention.

Outlook:

XRO would focus on enhancing its small business platform for the global level. Moreover, the company would continue to make reinvestments in the cash generated based on the investment criteria as well as market conditions, aimed at driving long-term shareholder value.

Stock Performance:

The shares of XRO have generated a decent YTD return of 48.15%. On 30 August 2019 (AEST 01:33 PM), the stock was trading at a price of A$63.000, up 1.368% from its previous close. XRO has a market cap of A$8.78 billion and ~ 141.34 million outstanding shares.

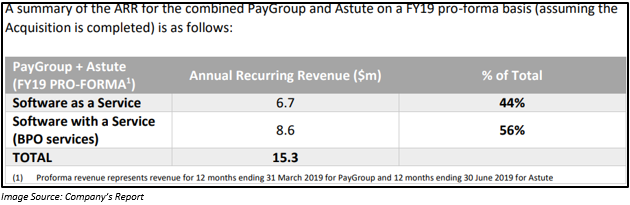

PayGroup Limited

PayGroup Limited (ASX: PYG), a provider of Human Resources SaaS and Software with a Service, on 28 August 2019 announced that it signed a term sheet in order to acquire Astute One Limited, which is an Australian-based Human Capital Management (HCM) business, along with its fully owned subsidiaries.

Astute was founded in the year 2006 and it has maintained a track record of profitable growth. It is the leading SaaS platform provider to workforce management companies as well as the corporate sector and has more than 330 clients across Australia and New Zealand. It works on the same ARR model as PYG.

The platform of Astute is capable of automating and simplifying highly complex compliance, employment as well as payment methods. Astute allows workforce management companies to improve their performance and effectiveness.

The proposed acquisition is consistent as per the strategic plan of the company to increase in annual recurring revenue along with the client base.

Acquisition Terms and Conditions:

The total consideration amount for the proposed acquisition is $11 million, which depends on the certain purchase price adjustments at completion like net debt along with the working capital.

There would be an additional earn-out consideration to a maximum of $1.5 million in PayGroup shares which would be payable depending on revenue and earnings performance of Astute by 30 September 2020. Also, there would be a claw-back mechanism which would be included in case Astute could not attain its revenue and earnings targets.

Stock Performance:

The shares of PYG have generated a negative YTD return of 25.47%. On 30 August 2019 (AEST 01:34 PM), the stock was trading at a price of A$0.700, up 2.19% from its previous close. PYG has a market cap of A$35.39 million and ~ 51.67 million outstanding shares.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.