The financial results posted by the ASX listed companies depicted a mixed scenario- with some signalling dip in operational and financial performance, while others riding high on the growth trajectory.

Talking about growth, dairy stocks - (ASX: A2M) and (ASX: SM1) posted decent numbers in the disclosure of the final results in August and September this year, respectively. However, the markets didnât react optimistically to those results. Consequently, the respective stocks were under pressure during the trading hours, following the results releases, shedding substantial gains as well.

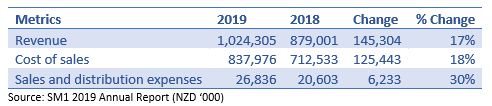

Small-Cap company â Synlait Milk Limited (ASX: SM1) posted revenue growth of 17%, reaching a billion-dollar (NZD) mark for the first time, which was indeed an accomplishment for the year ended 31 July 2019 (FY 2019).

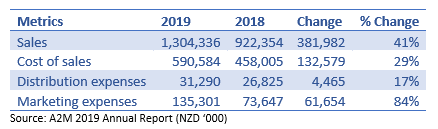

Mid-Cap company â The a2 Milk Company Limited (ASX: A2M) delivered revenue growth of a whopping 41.4% to NZD 1.3 billion for the year ended 30 June 2019 (FY 2019).

Sustainable Growth

A2Mâs Approach

In its 2019 Annual Report, A2M stated that a strategic approach to ensure sustainability is an integrated part of its business strategy. Macroeconomically, the dairy producerâs business is in a favourable position to reap rewards of its presence in growing markets â China & USA.

Chinese Market (Source: A2Mâs Investor Presentation)

Chinese Market (Source: A2Mâs Investor Presentation)

The company would be purchasing verified carbon offsets sourced from the projects in the key local markets where the company operates â ANZ, China & USA. In 2019, one of the companyâs key farms â Moxey Farms in New South Wales produced electricity and natural fertiliser from cow manure.

A2M is investing in developing new programmes to improve soil health, GHG emissions, biodiversity, water quality, animal welfare, and collaborating with farmers to innovate on-farm.

The company mentions that its global product packaging is 95% recyclable, and it is expanding the use of recyclable content in packaging, replacing single-use plastic. In the UK, the companyâs new fresh milk cartons are carbon neutral and use over 80% less plastic than the previous design.

The company is implementing a circular economy approach at its fresh milk processing facility in NSW, achieving over 95% of waste diversion from its production process. Further, the liquid waste is sent back to the farms for beneficial use as organic fertiliser after treatment at the on-site 80kL waste-water treatment system.

A2M is also working with its strategic partners to deliver on sustainable growth. The companyâs infant formula producer in New Zealand â Synlait Milk has installed the first large-scale electric boiler in the country as part of its commitment to reduce off-farm greenhouse gas emissions by 50% by 2028.

SM1âs Approach

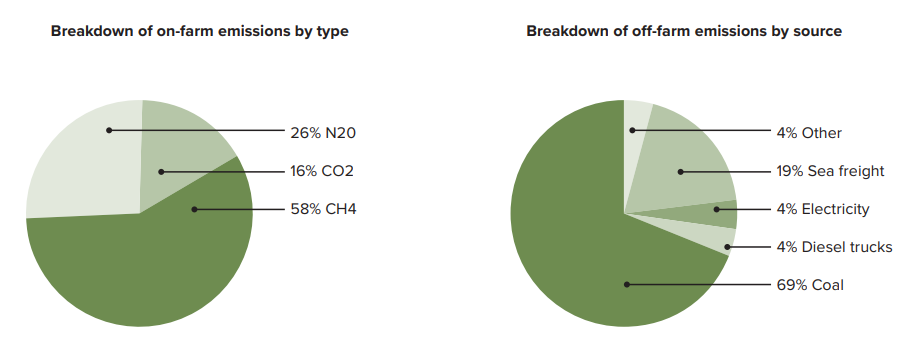

The company undertook its first Greenhouse Gas (GHG) inventory. The externally audited report showed that in the period from 1 August 2017 to 31 July 2018, the company GHGâs emissions were 912,731 tCO2e.

GHG Breakdown (Source: SM1âs 2019 Annual Report)

It was highlighted that the use of coal (108,301 tCO2e) and sea freight (30,162 tCO2e) were the two largest sources of off-farm GHG emissions, with electricity third (6,923 tCO2e). In addition, the non-farm emissions totalled 755,583 tCO2e that included quantum of carbon dioxide, methane, and nitrous oxide.

The company has introduced a GHG reduction incentive payment with âLead With PrideTMâ â an internationally accredited ISO 17065 dairy farm assurance system. Farms have to develop farm-specific GHG management plans, demonstrating a clear knowledge of GHG sources with mitigation strategies to receive the incentive payment.

Synlait Dunsandel commissioned New Zealandâs first large-scale electrode boiler to provide process heat to the advanced liquid dairy packaging facility. Traditional techniques were relying on coal as a cost effective source to create large volumes of process heat that are required to turn milk into powder, pasteurise and sterilise milk, clean production lines, and help form product packaging.

Profitability

At sales of NZD 1.3 billion, A2M generated a profit after tax of NZD 287.7 million for FY 2019 with a basic EPS of NZ 39.25 cents. Meanwhile, in FY 2019, SM1 reported revenue of NZD 1.02 billion and delivered net profit after tax of NZD 82.24 million with a basic EPS of NZ 45.89 cents.

Considering the vast investment opportunities designed to support growth aspirations, the Board of A2M does not anticipate paying any dividends in the near-term.

Synlait says that given the prolonged growth agenda and strategies to enter new categories, it would invest at a rate to match the investment pattern depicted during the initial eleven years. Further, the company do not anticipate paying dividends in the foreseeable future.

In a growth company, investors must expect that the profitability could be lower due to reasons, including investments, customer-retention techniques, discounts, promotional activities, new product launches, market share penetration, new sites etc. Moreover, the capital expenditure, as well as revenue expenditure, is likely to depict higher levels, possibly suppressing profitability metrics of a growing company.

Select Expense Analysis

In FY 2019 for A2M, let us look at some core expenses to deliver robust sales growth. The metrics depict that the company had to increase marketing expenses by 84%, distribution expense by 17% in order to achieve a sales growth of 41%.

In FY 2019 for SM1, the company increased its sales and distribution expense by 30% to achieve revenue growth of 17%. In contrast to A2M, it is evident that more expenses on sale & distribution capabilities could help to deliver better growth in sales or revenue.

On 1 November 2019, A2M traded at $12.05, up by 0.08% relative to the previous close (as at 2:49 PM AEST).

On 1 November 2019, SM1 raded at $8.70, down by 0.23% relative to the previous close (as at 2:49 PM AEST).

Bellamyâs Acquisition

On a related, let us aquaint you about whats panning out for a similar company in the related space.In September, it was announced that Bellamyâs Australia Limited (ASX:BAL) would by wholly acquired by China Mengniu Dairy Company Limited. The offer was $12.65 per share in cash and a fully franked special dividend of $0.60 per share.

Recently, the Court had approved the despatch of scheme booklet and schedule of scheme meeting to consider voting on the offer for the companyâs acquisition. Further, the scheme meeting has been scheduled on 5 December 2019. In addition, the scheme and special dividend record date is 17 December 2019 with special dividend pay-date on 23 December 2019.

Disclaimer

This website is a service of Kalkine Media Pty. Ltd. A.C.N. 629 651 672. The website has been prepared for informational purposes only and is not intended to be used as a complete source of information on any particular company. Kalkine Media does not in any way endorse or recommend individuals, products or services that may be discussed on this site. Our publications are NOT a solicitation or recommendation to buy, sell or hold. We are neither licensed nor qualified to provide investment advice.